Short-term health insurance

Key takeaways

- Short-term health insurance offers a temporary safety net for some who can’t afford ACA-compliant plans.

- Short-term health insurance availability varies by state. Check your state here.

- Find answers to readers’ frequently asked questions about short-term health insurance.

- Read more articles about short-term coverage.

An affordable short-term safety net

The Affordable Care Act delivered affordable comprehensive health insurance to millions of Americans.

But while provisions of the law have indeed lowered coverage costs for most people who need to buy their own health insurance, some people cannot obtain affordable coverage. This can be due to an undocumented immigration status, failure to apply for coverage during an open enrollment or special enrollment period, or an inability to pay even subsidized premiums.

If you’re among these consumers – and you’ve looked at all the on- and off-exchange options for regular health insurance and simply cannot afford them or are not eligible to enroll – it’s worth at least weighing the pros and cons of short-term coverage.

The Trump administration expanded the rules for short-term plans, allowing them to continue for longer durations than previously allowed. The Biden administration has proposed rule changes that would sharply limit short-term health plans, allowing them to have initial terms of no more than three months and total duration, including renewals, of no more than four months. But for the time being, the longer duration rules are still in effect unless a state has taken action to further restrict short-term health plans.

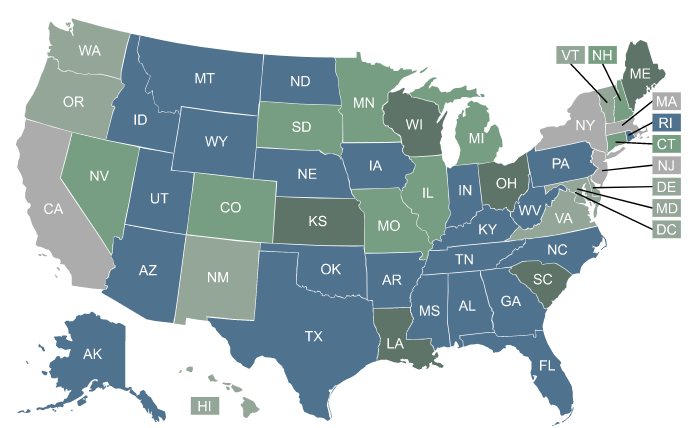

Short-term health insurance availability in your state

| Short-term plans available for purchase |

|

| No short-term plans currently for sale |

Explore your short-term health insurance options.

Get a free quote from our third-party insurance agency partners!

Frequently asked questions about short-term health insurance

What is short-term health insurance?

Short-term health insurance offers temporary coverage to fill a gap between other health plans. Short-term health insurance is not comprehensive coverage and is not regulated by the Affordable Care Act, mental health parity rules, No Surprises Act, or other federal health insurance rules.

Short-term health insurance is not an excepted benefit under the ACA. But it is exempt from federal insurance rules and regulations specifically because it is not considered individual health insurance (see Section II(A)).

Who might consider short-term coverage?

These plans are attractive to people who don’t qualify for premium subsidies in the health insurance marketplace/exchange, or who missed open enrollment and are otherwise facing a gap in coverage. This includes people who are between jobs, retiring prior to Medicare eligibility, or those who have already enrolled in other insurance coverage (an employer’s plan or an ACA-compliant individual market plan, for example) and are waiting for it to take effect.

A short-term health plan can also be used to bridge a gap in coverage if you’re newly employed and have a waiting period of up to three months before you’re eligible to enroll in your employer’s health benefits plan.

Why would I buy a short-term plan – and not an ACA-compliant plan?

There are currently about 2.2 million people caught in the coverage gap in 11 states that have refused to expand Medicaid. Their household incomes are under the federal poverty level, so paying full price for health insurance is probably a non-starter. (The coverage gap is expected to shrink to nine states by 2024, with South Dakota expanding Medicaid in mid-2023 and North Carolina expected to do so in 2024).

The American Rescue Plan and Inflation Reduction Act have temporarily eliminated the subsidy cliff through 2025, meaning that households with income over 400% of the poverty level can qualify for a premium subsidy if the cost of the benchmark plan would otherwise be more than 8.5% of the household’s income.

And the IRS partially fixed the family glitch as of 2023, so some families are newly eligible for subsidies in the marketplace when their offer of employer-sponsored coverage is not affordable (although the employee is still ineligible for marketplace subsidies, meaning that the family’s total premiums could still be outside their budget).

But the coverage gap continues to be a problem. And subsidies are also not available to undocumented immigrants, who aren’t allowed to purchase coverage through the exchange even if they’re willing to pay full price (some states are addressing this issue on their own).

And if you missed open enrollment (either for your employer’s plan or for a private individual/family plan) and aren’t eligible for a special enrollment period, you likely cannot enroll in real major medical coverage until the following year, unless you’re eligible for Medicaid.

If you’re among these consumers who don’t have access to affordable ACA-compliant coverage, it’s worth at least weighing the pros and cons of short-term coverage.

Do short-term plans cover ACA's essential benefits?

Under federal rules, short-term plans are not required to cover the ACA’s essential health benefits. So in most states where short-term health plans are available, the available plans tend to have more benefit limitations than ACA-compliant plans, and gaps in their coverage for at least some of the essential health benefit categories.

The most commonly excluded categories of coverage are maternity care, mental health care, preventive care, and prescription drugs, although short-term plans can be designed to include or exclude whatever services they choose, unless states require certain mandated benefits to be covered. (Click on your state on the map above to see plan availability and information about how short-term health insurance is regulated.)

Most short-term plans will provide at least some coverage for medically necessary inpatient and outpatient medical care, including emergency services. But there are generally blanket exclusions for any pre-existing condition that the enrollee may have, and the plans will often impose limits on the amount the plan will pay for certain services.

How long will a short-term health plan cover me?

Depending on where you live and the insurance company you select, it’s possible to get a short-term plan that can last for a total duration of up to three years, including renewals.

But the Biden administration is expected to propose new rules in April 2023 that would limit short-term health plans. It’s unclear what the administration will propose, but the Biden administration implemented a three-month cap on short-term plans, so something like that could be revisited by the Biden administration (note that the proposed rule was previously expected in 2022 and did not appear, so it’s not certain that new rules will be proposed in the spring of 2023).

But for now, federal rules allow short-term health plans to have initial terms of up to 364 days, and total duration, including renewals, of up to three years. The insurer may offer the option to lock in guaranteed renewability, without additional medical underwriting, when the policy is purchased, meaning that the applicant would only have to apply once and could be covered for up to three years. (Note that in most states, short-term health insurers are not required to offer renewability. Check the plan details carefully before purchasing coverage, to make sure you understand what you’re buying.)

About half the states have stricter rules, however, and do not allow plans to remain in effect for a full three years. And even in states where longer short-term plans are allowed, some insurers choose to only offer shorter terms and/or non-renewable plans.

Who is eligible to purchase short-term health insurance?

As long as you can pass the cursory medical underwriting involved in most short-term health plan applications (a very short series of yes/no questions about major medical events), you can purchase a short-term plan. But be aware that the plan will likely exclude any pre-existing medical condition, even if it’s not mentioned in the list of health questions asked on the application.

How do consumers buy short-term health insurance coverage?

Short-term health insurance is typically purchased online, although paper applications and in-person enrollments are available in some cases. Short-term health insurance can be obtained via a website that offers numerous plan options, or directly from an insurance company that sells short-term plans.

Short-term health plans are offered by several national companies that sell plans in numerous states, as well as regional companies that have more localized service areas, so short-term plan availability varies considerably depending on where you live.

Short-term health insurance plans are available in most states, but there are 13 states (including DC) where no short-term plans are available, due to either outright bans or state laws that are unattractive to the insurers that offer short-term health plans.

When can I enroll in a short-term health plan?

Enrollment in short-term health plans is available year-round, albeit with medical underwriting. So you can enroll or change plans anytime you like, without having to wait for an open enrollment period.

(Note that some states prohibit enrollment in short-term health plans during the open enrollment period for ACA-complaint coverage. Maine and Washington are examples of this, but no insurers offer short-term health plans in either of those states as of 2023.)

How long will it take me to get short-term coverage?

With short-term policies, healthy applicants can secure immediate individual and family coverage, with plans that can kick in as early as the next day. If you already know the number of days you will need to be covered, your insurer may allow you to make a single payment for the whole coverage period.

The application process for short-term health insurance is typically quite simple, with just a handful of yes/no questions about medical history. As long as your answer to all of the questions is “no,” you’ll generally be accepted for coverage with an effective date as soon as the following day.

(It’s important to understand that short-term healthcare plans generally rely on post-claims underwriting, which means they’ll go back and take a closer look at your medical history if and when you experience an injury or illness that results in a medical claim, to ensure that the condition was not pre-existing.)

How much does short-term health insurance cost?

The monthly premiums for short-term health insurance vary considerably depending on where you live, your age, and the insurance company that’s offering the coverage. Depending on the circumstances, they can start at well under $100/month.

Although premium subsidies are not available for short-term policies, the plans do tend to be considerably less expensive than ACA-compliant major medical plans if you’re not eligible for a premium subsidy.

With that said, however, most people are eligible for premium subsidies to purchase coverage through the exchange, assuming they’re not eligible for Medicare, Medicaid, or an employer’s health plan. And opting for short-term coverage would mean that you’d forfeit your premium subsidy.

How do short-term health insurance premiums compare to ACA plan premiums?

A lower monthly premium is the primary draw for short-term plans. Consider a single 45-year-old, living in southwestern Wyoming and earning an income of $13,000/year in 2023 (there’s an ACA-specific calculation for household income). That’s under the 2022 poverty level, which is used to determine eligibility for 2023 subsidies. And Wyoming has not accepted federal funding to expand Medicaid. That means this person is ineligible for Medicaid, and they’re also ineligible for premium subsidies in the exchange/marketplace (ie, they’re in the coverage gap).

The least expensive ACA-compliant plan available to this person will cost $647/month. That’s obviously unrealistic with an income of only a little more than a thousand dollars a month.

But if we look at short-term plans, there are policies available with premiums starting at around $110/month, and numerous plans available with premiums below $200/month. That’s still a stretch for someone earning $13,000/year, but it’s much more feasible than $647/month.

The deductible for the lowest-priced short-term plans will be in the range of $10,000 (versus $7,500 for the least-expensive ACA-compliant plan), and the out-of-pocket maximum will be $20,000 (versus $8,150 for the cheapest ACA-compliant plan available to this person; the upper limit on out-of-pocket costs for any ACA-compliant plan is $9,100 in 2023).

Some of the available short-term plans have a maximum duration of six months, while others allow up to 364 days of coverage. There are several plan designs available, and although none of them are as comprehensive as ACA-compliant plans, the trade-off is that they have much lower premiums.

(It should be noted that if this person had an income of $14,000, instead of $13,000, they would be eligible for a premium subsidy of more than $900 per month, which would allow them to choose from numerous premium-free ACA-compliant plans in the Wyoming exchange. None of the available plans would cost more than about $140/month, even for the most comprehensive options. This is why it’s so important to understand the income thresholds for subsidy eligibility in the exchange.)

What does short-term health insurance cover?

Short-term health insurance policies are designed to cover at least some of the cost of unexpected medical events that are not linked to a pre-existing condition. The plans will generally provide coverage for inpatient and emergency care, surgeries, and various outpatient services, lab work, and imaging. Some short-term plans include inpatient prescription drugs, although it’s much less common for short-term plans to cover prescriptions that you’d pick up at the pharmacy.

Can I buy short-term insurance in my state?

Though short-term plans are available in most states, short-term plans aren’t available at all in 12 states and DC.

States where you can’t buy short-term health plans in 2023:

- California

- Colorado

- Connecticut

- District of Columbia

- Hawaii

- Maine

- Massachusetts

- New York

- New Jersey

- New Mexico

- Rhode Island

- Vermont

- Washington

In some cases, this is because state regulations ban them outright, while in other cases it’s because state regulations are strict enough that insurers have opted not to sell short-term plans. And the availability of short-term plans does sometimes fluctuate from one year to the next in a given state, due to insurer business practices and evolving state regulations. So this list has changed a bit over time.

Short-term plans are available in the remaining states, but regulations and availability vary considerably from state to state. (Choose your state from the map above to to see how short-term plans are regulated within your state.)

Will short-term plans cover my doctors?

Short-term health insurance plans cover a range of physician services, surgery, outpatient and inpatient care. In addition, policyholders can sometimes choose their own doctor and hospital without restrictions, though there may be financial incentives for using in-network providers.

If the short-term plan has a provider network, the provider’s total payment will be adjusted to match the insurer’s approved reimbursement rate, with the cost split between the health plan and the policyholder according to the terms of the plan. But if the health plan does not have a provider network — often touted as a benefit that provides freedom to see any doctor — enrollees should be aware of how balance billing works. This is described in more detail below.

Does short-term health insurance cover pre-existing conditions?

Even if you’re eligible for coverage based on the short list of questions asked on the application, you will generally not have coverage for any pre-existing medical conditions while you’re enrolled in the plan. Short-term plans exist solely to provide coverage for medical conditions that have not yet arisen – and will generally not be any help at all in terms of medical conditions you already have.

Be sure to check the list of exclusions on any policy. Short-term plans also tend to use post-claims underwriting, which means they will typically take your word for your health status when you enroll, but can then go back through your medical history if and when you have a claim, making sure that you were truthful on your application and verifying any pre-existing conditions.

What are possible drawbacks of short-term health plans?

What are some of the factors that might make consumers reluctant to buy short-term coverage?

You may be subject to balance billing

Some short-term plans tout the fact that you can see any doctor or go to any hospital you want. While that might sound good, it’s also a red flag for potential balance billing. If the plan doesn’t have a provider network, that means the doctors and hospitals that members end up using have not agreed to accept the insurer’s reimbursement rates as payment in full.

In that case, whatever amount the insurer pays them (a “reasonable and customary” amount, a percentage of Medicare rates, etc.) is likely to be less than what they billed. And since they do not have a contract with the short-term insurer, they are free to send a bill to the patient for whatever amount the insurance plan doesn’t pay.

So even if the plan has a maximum out-of-pocket limit, enrollees should keep in mind that balance billing could potentially result in much higher out-of-pocket costs if the plan doesn’t limit care to a specific network of providers.

You could still end up facing a gap in coverage.

When your short-term plan ends, you will not be eligible to purchase a regular plan in the individual market if it’s outside of open enrollment. Loss of minimum essential coverage is a qualifying event that triggers a special enrollment period, but a short-term plan is not considered minimum essential coverage.

But if you’re buying short-term coverage to get you through to the end of the year, you’ll be able to purchase an ACA-compliant plan during open enrollment that will take effect the first of the coming year. And if you’re going to be starting a new job that offers health insurance, you’ll be able to enroll in your new employer’s plan as soon as you’re eligible.

(It’s worth noting that the termination of a short-term plan does trigger a special enrollment period for group health coverage. (See page 51 of the 2018 rule for short-term plans). So if you have access to your employer’s plan but hadn’t enrolled — and had enrolled in a short-term plan instead — the termination of your short-term plan would allow you a special enrollment period during which you could enroll in your employer’s plan.)

That last point is important to keep in mind. If you purchase a 364-day plan in July and then suffer a serious illness or injury the following April, you could find yourself in a predicament if the plan you purchased was not guaranteed renewable. (Under the federal rules, insurers have the option to offer guaranteed renewability, but are not required to do so; some states do require renewability, but they’re the exception).

Depending on your medical situation, you may not be able to purchase another short-term plan when yours expires in June. And you wouldn’t be eligible for a special enrollment period to buy an ACA-compliant plan, since the termination of a short-term plan is not a qualifying event. More than likely, you’d have to wait for open enrollment in order to sign up for a new plan, which would take effect January 1.

So you could find yourself uninsured for several months (in this case, July through December), and it might be at a time when you have ongoing medical needs related to the illness or injury that made you uninsurable for a second short-term plan. This is complicated, and certainly requires more than a passing glance when you’re considering what coverage option to purchase.

Are temporary health plans regulated by the ACA?

Although the ACA has largely done away with medical underwriting for health insurance, short-term plans are not regulated by the ACA and they still ask some basic medical history questions in order to determine an applicant’s eligibility for coverage.

And post-claims underwriting is widely used for short-term health plans. But that also means that short-term policies are available year-round, which is not the case for ACA-compliant individual major medical plans.

Do short-term plans have benefit maximums?

Yes. Since short-term plans are not regulated by the ACA, they can still have annual and lifetime benefit maximums.

Is loss of my short-term coverage a qualifying event?

These policies are not considered minimum essential coverage under the ACA, which means that the termination of a short-term policy is not a qualifying event that triggers a special enrollment period for an ACA-compliant individual market plan.