Find the dental plan in Massachusetts that’s right for you.

Need dental coverage in Massachusetts? Shop and enroll in coverage that can start as early as tomorrow.

Massachusetts dental insurance guide

Massachusetts Health Connector has certified individual and family dental plans from two insurers

Massachusetts uses a state-based health insurance exchange called Massachusetts Health Connector for the sale of certified individual/family dental plans as well as small group dental options.

All insurers that offer medical plans through the Massachusetts exchange include pediatric dental coverage with their health plans, and a few offer limited adult coverage. Stand-alone dental plans are available for both children and adults through the Connector all year.

Massachusetts voters pass ballot measure to create medical loss ratio rules for dental plans

In the 2022 election, Massachusetts voters overwhelmingly supported Question 2, which will impose medical loss ratio rules on dental plans in the state as of 2024. Advocates in the state are hoping that the new rules will serve as a model for other states to create similar rules.

Under the terms of Question 2, dental plans in Massachusetts will have to spend at least 83% of premiums on members’ dental care and quality improvements, and will be allowed to spend no more than 17% of premiums on administrative costs. The ACA imposed medical loss ratio rules for health insurance, but did not address dental coverage (Massachusetts has medical loss ratio rules that are more strict than those imposed by the ACA).

Massachusetts Question 2 was supported by dentists and dental associations, including the American Dental Association, who noted that the passage of the measure will help to bring dental insurance regulations in line with medical insurance regulations, and help to eliminate administrative waste and excessive salaries for executives. It was opposed by major dental insurers in the state, who argued that it will result in higher premiums and less access to dental insurance.

It’s true that one of the criticisms of the ACA’s medical loss ratio (for health insurance) is that it doesn’t put a lid on overall premiums, since higher total premiums allow for higher administrative costs. But most of the state’s large dental carriers already spend close to 83% of premiums on dental care and quality improvements, and experts project that premiums are not likely to rise by excessive amounts.

Question 2 also authorizes the Massachusetts insurance commissioner to reject dental carriers’ proposed rates if they’re deemed excessive. (Many states have a similar provision for medical insurance rates, although some states’ rate review processes do not allow insurance commissioners to reject premium increase, even if they find them to be unjustified.)

Frequently asked questions about dental coverage in Massachusetts

How much does dental insurance cost in Massachusetts?

Premiums range from $47 to $252 per month for adults who purchase their own stand-alone or family dental coverage through the exchange.1

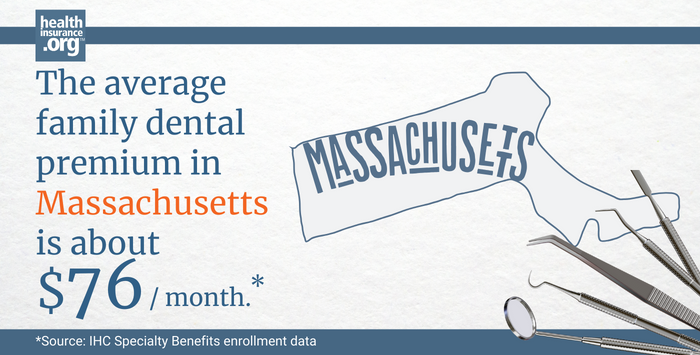

IHC Specialty Benefits reports that the average monthly premium for a stand-alone family dental plan sold in Massachusetts in 2023 was $75.77.

If a family is purchasing coverage through the health insurance exchange, the premiums associated with pediatric dental coverage may or may not be offset by premium tax credits (premium subsidies). Here’s more about how that works, depending on whether the health plan has integrated pediatric dental benefits.

Are stand-alone pediatric dental plans on the exchange ACA-compliant?

All insurers that offer medical plans through the Massachusetts exchange include pediatric dental coverage with their health plans. To purchase a stand-alone dental plan for someone under 19 years old without medical coverage, you must contact the exchange directly at 1-877-MA-ENROLL. Otherwise, family and adult plans are available through the website.

The exchange-certified pediatric stand-alone dental plans available in Massachusetts will comply with the ACA’s pediatric dental coverage rules. This means out-of-pocket costs for pediatric dental care will not exceed $375 per child in 2023 (or $750 for all the children on a family’s plan), and there is no cap on medically-necessary pediatric dental benefits.

As is the case for all essential health benefits, the specific coverage requirements for pediatric dental care are guided by the state’s essential health benefits benchmark plan.

You can see details here for Massachusetts’s benchmark plan, which does include coverage for both basic and major dental services for children.

Which insurers offer dental coverage through the Massachusetts marketplace?

Adult and family dental coverage is not automatically included with the medical plans from insurers who offer coverage through Massachusetts’s health insurance marketplace.

In 2023, two insurers offer stand-alone individual/family dental coverage through Massachusetts Health Connector. These are dental plans that are not included with a medical plan and must be purchased separately:

- Altus Dental

- Delta Dental

These dental plans can be purchased through the Massachusetts exchange at any time during the year, and not just during open enrollment (November 1 to January 23) or during a special enrollment period triggered by a qualifying life event. Exchange-certified stand-alone dental plans are compliant with the ACA’s rules for pediatric dental coverage. Massachusetts also offers non-standardized plans through the exchange that offer different features and out-of-pocket costs.

Can I buy dental insurance outside of Massachusetts's exchange?

There are also a variety of dental insurers that sell stand-alone dental plans directly to consumers in the Bay State. These plans are not subject to the ACA’s essential health benefit rules for pediatric dental coverage, but they are regulated by the Massachusetts Division of Insurance. If you would like to purchase a non-ACA qualified dental plan, ask a dentist for recommendations or search online.

In Massachusetts, there are also various dental discount plans available. Dental discount plans are not insurance, but they can offer discounted charges at participating dentists. Here’s what you need to know about the differences between dental insurance and dental discount plans.

To find plans in your area, search online for dental discount plans and the state you are looking to buy a plan in.

How does Massachusetts Medicaid and CHIP provide dental coverage?

Adults enrolled in Medicaid in Massachusetts are eligible for dental services. Children enrolled in MassHealth are eligible for various dental programs (based on their families’ benefit level) to ensure continuous coverage until the age of 21.

MassHealth, which is Massachusetts’s CHIP, provides coverage to uninsured children and pregnant women with income above the eligibility limits for Medicaid.

What dental resources are available in Massachusetts?

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written dozens of opinions and educational pieces about the Affordable Care Act for healthinsurance.org.

Footnotes

- ”IHC Specialty Benefits enrollment data” Accessed March 2024 ⤶