Find Maryland Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Maryland ACA Marketplace quick facts

Maryland health insurance Marketplace guide

This guide, including the FAQs below, is designed to help you understand the health coverage options and possible financial assistance available to you and your family in Maryland. For many, an Affordable Care Act (ACA) Marketplace (exchange) plan, also known as Obamacare, may be an affordable option.

Maryland operates its own state-based exchange called Maryland Health Connection. Maryland Marketplace plans are a good solution for self-employed people, early retirees needing coverage until Medicare, and people who work for small businesses that don’t offer health benefits.

For 2026, Maryland Health Connection offers plans from five insurers (including two CareFirst entities),4 down from six in 2025. See below for details about insurer and premium changes for 2026.

In addition to federal subsidies, Maryland also offers state-funded subsidies. This program had previously only been available to young adults, but it was expanded in 2026 to be available to Maryland Health Connection enrollees of all ages whose household income doesn’t exceed 400% of the federal poverty level.5 This was done to partially mitigate the impact of the expiration of federal subsidy enhancements at the end of 2025. See below for more details on how Maryland’s state subsidy program works, and how enrollment grew slightly in Maryland for 2026 (despite declining enrollment nationwide), likely in large part because of the state’s additional subsidies.

Maryland established a reinsurance program in 2019, which has kept full-price (unsubsidized) premiums lower than they would otherwise have been.6 Maryland also offers an easy enrollment program, which allows residents to connect with health coverage via their state tax return.

Frequently asked questions about health insurance in Maryland

Who can buy Marketplace health insurance in Maryland?

To qualify for Marketplace coverage in Maryland, you must:7

- Live in Maryland

- Be a U.S. citizen, national, or lawfully present in the U.S. (see note below)

- Not be incarcerated

- Not be enrolled in Medicare

Maryland has been working on the process of allowing undocumented immigrants to enroll via Maryland Health Connection, albeit without any subsidies unless state-funded subsidies were to eventually be allocated by the legislature.8 In early 2025, Maryland obtained federal permission to allow undocumented immigrants to begin enrolling in full-price Maryland Health Connection plans starting in November 2025.9

However, Maryland Health Connection has postponed this until 2028,10 because of the increased workload on the exchange due to H.R. 1 and the federal Marketplace Integrity rule.

(Washington was the first state to obtain federal permission to allow undocumented immigrants to use the exchange; Colorado operates a separate enrollment platform that undocumented immigrants can use. Both states provide state-funded subsidies for these enrollees.)

Whether or not you qualify for financial assistance with your premium, deductible, or out-of-pocket costs depends on your income and how it compares with the cost of the second-lowest-cost Silver plan in your zip code.

Additionally, to qualify for subsidies, you must:

- Not have access to affordable health coverage through an employer. If you think your employer-sponsored health plan is too expensive, use our Employer Health Plan Affordability Calculator to check if you might qualify for premium subsidies in the Marketplace.

- Not be eligible for Medicaid or CHIP.

- Not be eligible for premium-free Medicare Part A.[efn_note]Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Feb. 24, 2026[/efn_note]

- File a tax return (including Form 8962) and if married, you must file a joint tax return11 (with very limited exceptions)12

- Not be able to be claimed by someone else as a tax dependent.11

When can I enroll in an ACA-compliant plan in Maryland?

Open enrollment for 2026 coverage ended on January 15, 2026. However, the next open enrollment period, for 2027 coverage, will be shorter. Due to a federal rule change, it will have to end no later than December 31, 2026.

All plans selected during the open enrollment period in the fall of 2026 will take effect on January 1, and there will no longer be an open enrollment period option to enroll in January for a February 1 effective date.

Outside of open enrollment, you generally need a qualifying life event, such as losing coverage, getting married, or permanently moving, to enroll or make changes. The qualifying life event will trigger a special enrollment period (SEP).

Note that Maryland is one of several states where pregnancy is considered a qualifying life event, giving a person 90 days from the date of the pregnancy confirmation to enroll in a health plan.13

Some people can enroll outside of open enrollment without a specific qualifying life event. For example:

- American Indians and Alaska Natives can enroll year-round.

- People who utilize Maryland’s easy enrollment period can begin the process of obtaining health insurance by checking a box on their tax return.14

People who qualify for Medicaid, the Maryland Children’s Health Program (MCHP), or MCHP Premium can enroll anytime.15

How do I enroll in a Marketplace plan in Maryland?

There are several ways to enroll in an ACA Marketplace plan in Maryland:16

- Online: Go to MarylandHealthConnection.gov to create an account and apply.

- Phone: Contact the Call Center at 855-645-8572. Those who are deaf and hard of hearing use the Relay service. Help is available in over 200 languages.

- Talk to a broker: Get help from an authorized insurance broker through Broker Connect.17

- Talk to a navigator: Get help from one of the local navigator organizations in Maryland.

- Mobile app: Apply from your phone by downloading the mobile app, Enroll MHC.

How can I find affordable health insurance in Maryland?

You can find affordable individual and family health plans in Maryland through MarylandHealthConnection.gov, the state’s ACA exchange.

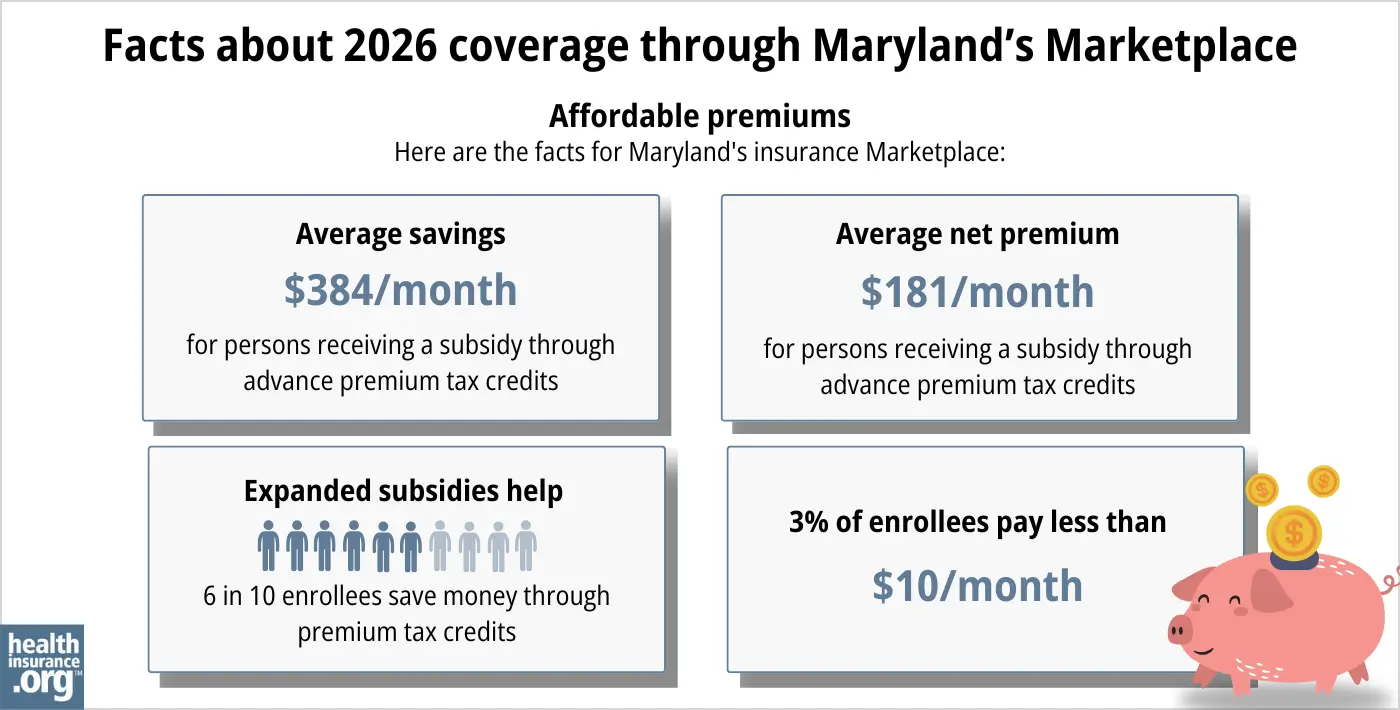

About 67% of Maryland’s exchange enrollees received premium subsidies in 2026, saving about $384 per month on their premiums. These subsidies are called Advance Premium Tax Credits (APTC). Subsidy-eligible Maryland residents pay about $181 monthly on average in premiums.1 But it’s important to understand that this only accounts for federal subsidies. Maryland’s state-funded subsidy program, described in more detail below, further reduces the premiums that many enrollees pay.

Source: CMS.gov1

If your income is no more than 250% of the federal poverty level, you may also qualify for cost-sharing reductions (CSR) to lower your deductibles and out-of-pocket costs.18

Thanks to the state-funded Maryland Premium Assistance program, Maryland Health Connection enrollees with household income up to 400% of the federal poverty level are eligible for additional premium subsidies, on top of the federal premium tax credit. And enrollees aged 18 to 37 qualify for additional state-funded subsidies, on top of both the federal subsidies and the Maryland Premium Assistance program.19

Maryland expanded its state subsidy program for 2026, to mitigate some of the impact of the expiration of federal subsidy enhancements at the end of 2025. As a result, about 177,000 enrollees were receiving Maryland’s state-funded subsidies in early 2026,5 up from about 65,000 the year before (when the program was limited to young adults aged 18-37).20

Maryland Health Connection clarified that the state-funded subsidy program would be able to fully cover the loss of the federal subsidy enhancements for enrollees with income up to 200% of the federal poverty level, and partially cover it for enrollees with income up to 400% of the federal poverty level.4

Although Maryland does not have plan standardization, the exchange does offer “Value Plans,” which have lower out-of-pocket costs for certain frequently-used services.21 And starting in 2024, changes were made to the Value Plans “to make the costs for common health care services clearer and more consistent across insurance companies.”22

How many insurers offer Marketplace coverage in Maryland?

Five insurers (including two CareFirst entities) offer coverage through Maryland Health Connection in 2026:4

- CareFirst BlueChoice, Inc.

- CareFirst GHMSI/CFMI

- Kaiser

- Optimum Choice, Inc.

- Wellpoint Maryland

There were six participating insurers in 2025,23 But Aetna exited the health insurance Marketplaces in all states where they offered coverage in 2025.

Aetna was new to Maryland’s Marketplace in 2024,24 and their plans were available for 2024 and 2025. But Aetna enrollees had to select replacement coverage for 2026. According to the Maryland Insurance Administration, almost 5,000 enrollees had Aetna coverage in 2025 and needed to pick a new plan for 2026.25

Are Marketplace health insurance premiums increasing in Maryland?

The following average rate increases (calculated before subsidies are applied) were approved for 2026, amounting to an overall average increase of 13.4%.4

Maryland’s ACA Marketplace Plan 2026 APPROVED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Change |

| Aetna Health, Inc. | Exited the market |

| CareFirst BlueChoice, Inc. | 13.6% |

| CareFirst GHMSI/CFMI | 13.1% |

| Kaiser | 9.8% |

| Optimum Choice, Inc. | 15.2% |

| Wellpoint Maryland | 10% |

Source: Maryland Insurance Administration4

Note that the average rate changes affect full-price premiums, and most enrollees are eligible for premium subsidies and thus don’t pay the full amount. These subsidy amounts are adjusted annually to match the cost of the second-lowest-cost Silver plan.

But because the federal subsidy enhancements were allowed to expire at the end of 2025, federal premium subsidies cover a smaller share of enrollees’ premiums and are available to fewer people in 2026, resulting in higher net premiums. However, Maryland’s state-funded subsidy program is fully covering the loss of the federal subsidy enhancements for enrollees with income up to 200% of the federal poverty level, and partially covering it for enrollees with income up to 400% of the federal poverty level.4

For the last few years, Maryland’s state-funded subsidy program was available to young adults ages 18-37, helping to make coverage even more affordable for this population (this program was previously available to adults up to age 34, but was extended to age 37).26 This program had been scheduled to sunset at the end of 2025, but Maryland enacted legislation in 2025 to make it permanent.[efn_note]”Maryland HB297” BillTrack50. Enacted May 20, 2025[/efn_note] And the program was enhanced to also provide state-funded subsidies to enrollees of all ages with household income up to 400% of the federal poverty level.19

Maryland established a reinsurance program in 2019, and federal approval was granted in 2023 to extend this program for another five years. The reinsurance program has kept Maryland’s individual market premiums much lower than they would otherwise have been.23

If your premiums are increasing from one year to the next, you might want to consider other Maryland Health Connection plans that better fit your budget and offer the benefits you need.

Here’s a look at how overall average premiums have changed each year in Maryland:

- 2015: 1% increase27

- 2016: 20% increase28

- 2017: 25.2% increase29

- 2018: 43.8% increase30 (after accounting for loss of federal CSR funding)

- 2019: 13% decrease31 (reinsurance took effect)

- 2020: 10.3% decrease32

- 2021: 11.9% decrease33

- 2022: 2.1% increase34

- 2023: 6.6% increase35

- 2024: 4.7% increase36

- 2025: 6.2% increase23

How many people are insured through Maryland’s Marketplace?

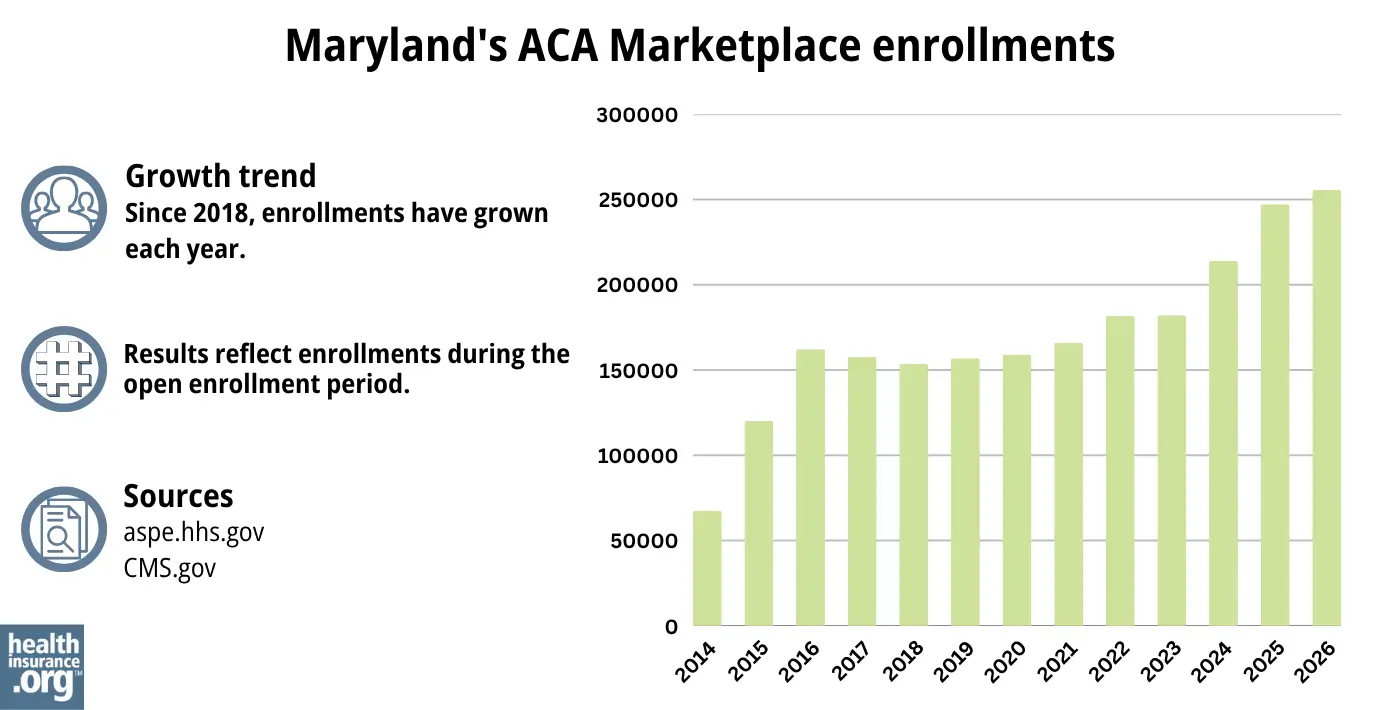

255,612 people enrolled in private plans through Maryland Health Connection during the open enrollment period for 2026 coverage, which was an increase of about 3% from the year before.5

But by February 2026, effectuated enrollment was essentially flat year-over-year, as a larger number of people had cancelled their coverage or not paid their initial premiums.37

Source: 2014,38 2015,39 2016,40 2017,41 2018,42 2019,43 2020,44 2021,45 2022,46 2023,47 2024,48 202549 20261

This surge in enrollment in recent years was due largely to the American Rescue Plan, which improved affordability starting in 2021. The Inflation Reduction Act extended these improvements until 2025, ensuring coverage remained more affordable than it was before the ARP became law.

As noted above, these subsidy enhancements expired at the end of 2025, driving full price premiums higher than they would otherwise have been.25

Maryland Health Connection noted that while enrollment did increase slightly for 2026 (as opposed to the nationwide average decline in enrollment), that was due in large part to the expansion of the state subsidy program that offset some of the higher premiums enrollees would otherwise have seen. The exchange also noted that they saw an increase in “buying down” for 2026, with people switching to plans at lower metal levels (going from a Gold plan to a Bronze plan, for example).5

But the trend of “buying down” was not as pronounced in Maryland as it was nationwide. Across the whole country, 40% of Marketplace enrollees picked Bronze plans for 2026, up from 30% in 2025. But In Maryland, the increase was much smaller: Just over 26% of enrollees picked Bronze plans for 2026, up from just under 24% in 2025.1

Another factor in the enrollment growth in 2024 and 2025 was the end of the pandemic-era Medicaid continuous coverage rule. Medicaid disenrollments resumed in 2023, after being paused for three years. By September 2024, more than 52,000 Maryland residents had transitioned from Medicaid to a private plan obtained via Maryland Health Connection, including more than 28,000 who were automatically enrolled50 (most states did not have an automatic enrollment process for people transitioning away from Medicaid, but Maryland implemented this to mitigate loss of coverage post-pandemic).

Maryland Health Connection reported that more than 14,000 of the people who enrolled during the open enrollment period for 2024 coverage had transitioned away from Medicaid,51 but the disenrollments and coverage transitions had begun in mid-2023, well before the start of open enrollment.

What health insurance resources are available to Maryland residents?

Maryland Health Connection

This is the state’s official health insurance Marketplace, where residents can shop for and enroll in health coverage plans.

Maryland Department of Health

This department oversees various health-related programs in the state, including providing information and managing enrollment for Medicaid.

Maryland Health Education and Advocacy Unit

This unit offers education and support to help individuals understand and navigate their health insurance options, making informed decisions about their coverage.

Health Care Access Maryland

This organization ensures that Maryland residents can access quality healthcare services, assisting with enrollment, navigation, and resources.

Maryland Senior Health Insurance Program

Designed for older adults, this program offers valuable information and assistance related to Medicare.

Looking for more information about other options in your state?

Need help navigating health insurance options in Maryland?

Explore more resources for options in MD including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶ ⤶

- ”Health Carriers Propose Affordable Care Act Premium Rates for 2026” Maryland Insurance Administration. June 3, 2025 *The above is based on the most current data available. ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” and “Marketplace 2025 Open Enrollment Period Report: National Snapshot” Centers for Medicare & Medicaid Services, April 2026 ⤶

- ”Maryland Insurance Administration Approves 2026 Affordable Care Act Premium Rates” Maryland Insurance Administration. Accessed Sep. 22, 2025 ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- ”Open Enrollment Data Show as Families Contend with Rising Health Insurance Costs, Maryland Premium Assistance Program Helps Ensure Access to Coverage” Maryland.gov, Office of the Governor. Jan. 23, 2026 ⤶ ⤶ ⤶ ⤶

- Reinsurance Program. Maryland Health Benefit Exchange. Accessed December 2023. ⤶

- “Are you eligible to use the Marketplace?” HealthCare.gov, 2023 ⤶

- “Maryland HB728” and “Maryland SB705” BillTrack50. Accessed Feb. 16, 2024. ⤶

- ”Letter from CMS to Maryland” Centers for Medicare & Medicaid Services. Jan. 15, 2025 ⤶

- ”Undocumented residents’ access to state health insurance marketplace delayed from 2026 to 2028” Maryland Matters. Oct. 17, 2025 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Feb. 24, 2026 ⤶ ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- ”Special Enrollment” Marylandhealthconnection.gov, Accessed Feb. 24, 2026 ⤶

- ”Easy Enrollment Program” Maryland Health Connection. Accessed Feb. 24, 2026 ⤶

- “Maryland Health Connection Frequently Asked Questions” Marylandhealthconnection.gov, Accessed September 18, 2023 ⤶

- “Maryland Health Connection Frequently Asked Questions” Marylandhealthconnection.gov, Accessed Feb. 24, 2026 ⤶

- “Maryland Health Connection Find Help” Marylandhealthconnection.gov, Accessed Feb. 24, 2026 ⤶

- ”APTC and CSR Basics” Centers for Medicare & Medicaid Services. Oct. 2025 ⤶

- ”Maryland Premium Assistance” Maryland Health Connection. Accessed Feb. 24, 2026 ⤶ ⤶

- ”More Black, Hispanic and young Marylanders enrolled in state insurance marketplace” Maryland Matters. Jan. 18, 2025 ⤶

- ”All About Value Plans” Maryland Health Connection. Accessed Feb. 24, 2026 ⤶

- ”Maryland Health Connection’s Open Enrollment For 2024 Health Plans” The BayNet. Nov. 1, 2023. ⤶

- ”Maryland Insurance Administration Approves 2025 Affordable Care Act Premium Rates” Maryland Insurance Administration. Sep. 5, 2024 ⤶ ⤶ ⤶

- ”Maryland Insurance Administration Approves 2024 Affordable Care Act Premium Rates” Maryland Insurance Administration, September 18, 2023. ⤶

- ”Health Carriers Propose Affordable Care Act Premium Rates for 2026” Maryland Insurance Administration. June 3, 2025 ⤶ ⤶

- Young Adult Subsidy Program Expands Age Range. Maryland Health Connection. Accessed November 2023. ⤶

- “Modest Premium Changes Ahead in Health Insurance Marketplaces in Washington State and Maryland“ The Commonwealth Fund, October 20, 2014. ⤶

- “Maryland: *Approved* 2016 Weighted Avg. Hikes: 20.0% Overall (Updated)“ ACA Signups. September 4, 2015. ⤶

- “Maryland: *Approved* 2017 Avg. Rate Hikes Revised: 25.2% Vs. 27.9% Requested“ ACA Signups. September 24, 2016. ⤶

- “2018 Rate Hikes“ ACA Signups. ⤶

- “Marylanders to see premiums drop 13% on average for 2019 ACA plans” Baltimore Business Journal. September 21, 2018. ⤶

- “Maryland: *Approved* 2020 ACA Exchange Premium Rate Changes: 10.3% Reduction“ ACA Signups. September 19, 2019. ⤶

- “2021 Rate Changes“ ACA Signups. Accessed May 13, 2025 ⤶

- “Maryland Insurance Administration Approves 2022 Affordable Care Act Premium Rates“ Maryland Insurance Administration. September 3, 2021. ⤶

- “Maryland Insurance Administration Approves 2023 Affordable Care Act Premium Rates“ Maryland Insurance Administration. September 16, 2022. ⤶

- “Exhibit 1: 2024 Maryland ACA Individual Market Rate Filing Summary“ Maryland Insurance Administration, insurance.maryland.gov, September 2023. ⤶

- ”Data Report” Maryland Health Connection. Feb. 28, 2026 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- ”Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “2023 Marketplace Open Enrollment Period Public Use Files” CMS.gov, March 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶

- ”State-based Marketplace (SBM) Medicaid Unwinding Report” Centers for Medicare & Medicaid Services. Data through September 2024. ⤶

- ”Nearly 215,000 Enroll in 2024 Coverage, Most Ever for Maryland Health Connection” Maryland Health Connection. January 18, 2024. ⤶