modified adjusted gross income (MAGI)

What is modified adjusted gross income (MAGI)?

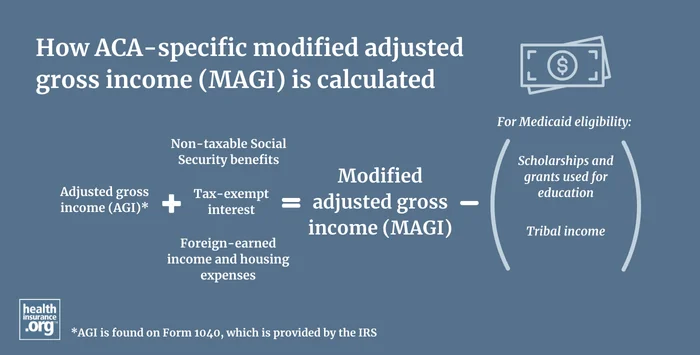

Under the Affordable Care Act (ACA), eligibility for Medicaid, premium tax credits1 (premium subsidies), and cost-sharing reductions2 is based on modified adjusted gross income (MAGI). But the ACA has its own calculation of MAGI, which differs from MAGI calculations used for other purposes.

MAGI starts with adjusted gross income (AGI) from Form 1040, but three things must be added to AGI to get MAGI under the ACA. If applicable, you must add in these amounts:

- Non-taxable Social Security benefits (this includes Social Security Disability Insurance benefits (SSDI), but Supplemental Security Income (SSI) does not get counted when the ACA-specific MAGI is determined)

- Tax-exempt interest (typically earned on municipal bonds)

- Foreign-earned income and housing expenses for Americans living abroad

Calculate Yearly Income

Use this to calculate your household’s estimated yearly income. Consider including your income, your spouse’s income, and that of any tax dependents, all of which are usually counted by the Marketplace. After that, provide information about expenses that may be deducted.This calculator is for educational and illustrative purposes only and should not be construed as financial or tax advice. It uses the income and other information you provide. We included categories of income and expenses that the Marketplace commonly (but not always) uses. You should contact a tax advisor or other professional about any specific requirements or concerns.

Click calculate to see updated yearly income

For Medicaid eligibility, some expenses can be subtracted, including scholarships and grants used for education, and certain American Indian/Native American income.3

Income received as a lump sum is counted as income only in the month it’s received when determining eligibility for Medicaid (whereas it would be counted as part of an enrollee’s annual income for determining eligibility for premium subsidies), although there’s an exception for lottery and gambling winnings of $80,000 or more – those amounts can be counted as income spread out across up to 120 months.45

If you receive advance premium subsidies (paid to your insurer on your behalf) based on your projected MAGI, the amount has to be reconciled on your tax return based on your actual MAGI for the year (and starting with the 2026 plan year, there’s no limit on how much excess premium subsidy you’ll have to repay). But there’s no after-the-fact reconciliation process for Medicaid or cost-sharing reductions.

In other words, Medicaid and CSR eligibility are determined at the time a person applies for coverage, and the benefits do not have to be repaid if the person’s actual MAGI ends up being different from what they projected.67

The details of the MAGI calculation are outlined in a CMS fact sheet.3 If you have questions or want guidance about your particular circumstances, consult a tax advisor or other professional.

Footnotes

- “Premium tax credit” HealthCare.gov. Accessed July 14, 2026 ⤶

- “Saving money on health insurance” HealthCare.gov. Accessed July 14, 2026 ⤶

- “Income Eligibility Using MAGI Rules” Centers for Medicare & Medicaid Services. Accessed July 14, 2026 ⤶ ⤶

- “Changes to Modified Adjusted Gross Income (MAGI)-based Income Methodologies” Centers for Medicare & Medicaid Services. Aug. 22, 2019 ⤶

- “State Plans for Medical Assistance - Treatment of certain lottery winnings and income received as a lump sum” Social Security Administration. Accessed July 14, 2026 ⤶

- “Cost-sharing reductions” Center on Budget and Policy Priorities. Updated Oct. 2025 ⤶

- “Questions and answers about health care information forms for individuals (Forms 1095-A, 1095-B and 1095-C)” Internal Revenue Service. Accessed July 14, 2026 ⤶