Medicare in Illinois

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Illinois

Key takeaways

- More than 2.4 million residents are enrolled in Medicare in Illinois.1

- About 43% of Illinois Medicare beneficiaries are enrolled in private plans.1

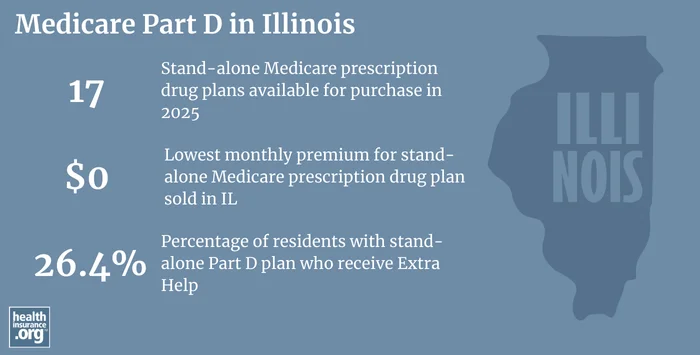

- Illinois residents can select from among 17 stand-alone Part D prescription plans in 2025, with premiums starting at $0 per month.2

Medicare enrollment in Illinois

There were 2,403,206 Medicare beneficiaries in Illinois as of August 2024, amounting to almost 18% of the state’s population.13

Most beneficiaries are eligible for Medicare coverage because they’re at least 65 years old. But Medicare eligibility is also triggered when a person has been receiving disability benefits for two years, or has ALS or end-stage renal disease. Nationwide, about 11% of people enrolled in Medicare are under 65;4 in Illinois, it’s about 10%; the state has about 232,000Medicare beneficiaries who are under 65.1

Medicare’s annual election period (October 15 to December 7 each year) allows Medicare beneficiaries the opportunity to switch between Medicare Advantage plans and Original Medicare and/or add or drop a Medicare Part D prescription plan.

Medicare Advantage enrollees also have the option to change to a different Medicare Advantage plan or to Original Medicare during the Medicare Advantage open enrollment period, which runs from January 1 to March 31.

Learn about Medicare plan options in Illinois by contacting a licensed agent.

Explore our other comprehensive guides to coverage in Illinois

The ACA Marketplace allows individuals and families to shop for and enroll in ACA-compliant health insurance plans. Subsidies may be available based on household income to help lower costs.

Hoping to improve your smile? Dental insurance may be a smart addition to your health coverage. Our guide explores dental coverage options in Illinois.

Learn about Illinois’ Medicaid expansion, the state’s Medicaid enrollment and Medicaid eligibility.

Short-term health plans provide temporary health insurance for consumers who may find themselves without comprehensive coverage. Learn more about short-term plan availability in Illinois.

Frequently asked questions about Medicare in Illinois

What is Medicare Advantage?

Although Medicare is funded and run by the federal government, enrollees can choose whether they want to receive their benefits directly from the federal government via Original Medicare or enroll in a Medicare Advantage plan offered by a private insurer, if such plans provide service in their area. There are pros and cons to Medicare Advantage and Original Medicare, and no single solution that works for everyone.

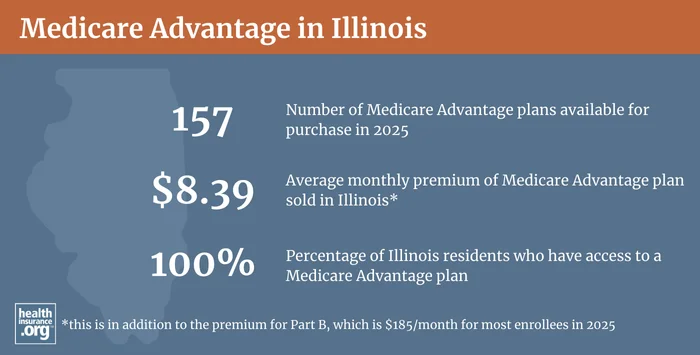

There are Medicare Advantage plans for sale throughout Illinois, with plan availability ranging from 1 plan to over 50 plans, depending on the county.5

43% of Medicare beneficiaries in Illinois were enrolled in Medicare Advantage plans as of August 2024.1

Medigap enrollment and regulations in Illinois

According to AHIP, 752,795 Illinois Medicare beneficiaries were enrolled in Medigap plans (also known as Medicare Supplement insurance) in 2023,6 to supplement their Original Medicare coverage.

Federal rules provide a six-month guaranteed-issue enrollment window for Medigap, starting when a person is at least 65 and enrolled in Medicare Part A and Part B. Federal rules do not provide annual guaranteed-issue enrollment or plan change opportunities, and federal rules also do not guarantee access to Medigap for Medicare beneficiaries under the age of 65.

But Illinois has stronger consumer protections in this area than most other states.

Birthday rule

In 2021, Illinois enacted legislation that created a new Medicare Supplement Annual Open Enrollment Period (effective as of 2022)7 The annual enrollment opportunity is fairly limited, but it does still go beyond federal rules. Illinois Medigap enrollees between the ages of 65 and 75 have an annual window during which they can switch to a different Medigap plan, offered by their current Medigap insurer (or an affiliate of their current insurer),8 as long as the plan offers equal or lesser benefits (so a person could switch from Plan F to Plan G, but not from Plan A to Plan G, for example). The window starts on the beneficiary’s birthday, and lasts for 45 days.9 (Several other states have developed similar “birthday rule” Medigap plan change opportunities, but the Illinois version is among the more limited.)

Guaranteed issue coverage from BCBSIL

And Illinois residents who are 65 or older can enroll year-round into certain guaranteed-issue plans offered by Blue Cross and Blue Shield of Illinois (BCBSIL)9 (Plans A, G, and N are available, plus some additional variations of those plans).10

Guaranteed-issue coverage for beneficiaries under 65

Illinois Medicare beneficiaries who are under 65 have a six-month guaranteed-issue window during which they can enroll in any Medigap plan sold in their area. However, the premiums can be higher than they would be for a 65-year-old enrollee. So when the person turns 65, they can utilize the federally required Medigap enrollment window to switch plans and/or obtain the age-65 premiums.9

Annual enrollment opportunity with BCBSIL for beneficiaries under 65

Additionally, if an Illinois Medicare beneficiary is under 65 and didn’t enroll in Medigap during their intial enrollment window, they have an annual opportunity to enroll in guaranteed issue coverage offered by BCBSIL, between October 15 and December 7.9

What is Medicare Part D?

Original Medicare does not cover outpatient prescription drugs. More than half of Original Medicare beneficiaries have supplemental coverage via an employer-sponsored plan or Medicaid, and these plans often include prescription coverage. But Medicare enrollees without creditable drug coverage need to obtain Medicare Part D prescription coverage. Medicare Part D plans can be purchased as a stand-alone plan, or as part of a Medicare Advantage plan that includes Part D prescription drug coverage.

Insurers in Illinois are offering 17 stand-alone Medicare Part D plans for sale in 2025, with premiums that start at $0/month.2

As of August 2024, more than 1.9 million Illinois Medicare beneficiaries had Medicare Part D coverage.1 About 50% of them had stand-alone Medicare Part D plans, while the rest had Medicare Advantage plans that included Part D coverage.1

Medicare Part D enrollment follows the same basic schedule as Medicare Advantage enrollment: Beneficiaries can pick a Part D plan when they’re first eligible for Medicare (or when they lose creditable drug coverage they had under another plan), or during the annual open enrollment period in the fall, from October 15 to December 7.

What additional resources are available for Medicare beneficiaries and their caregivers in Illinois?

Need help with your Medicare application in Illinois, or Medicare eligibility in Illinois?

- You can contact the Illinois Senior Health Insurance Program with questions related to Medicare coverage in Illinois.

- The Illinois Department on Aging has an excellent resource for Illinois residents who are shopping for Medigap plans. Premiums varies by location, so there are three separate guides: Chicago Area, North-Central Area, and Southern Area.

- Illinois has a helpful handbook for state employees who are transitioning to Medicare.

- The Medicare Rights Center website provides helpful information geared to Medicare beneficiaries, caregivers, and professionals.

Looking for more information about other options in your state?

Need help navigating health insurance options in Illinois?

Explore more resources for options in IL including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Illinois.” Centers for Medicare & Medicaid Services Data. Accessed December, 2024. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- ”Fact Sheet: Medicare Open Enrollment for 2025” (41) Centers for Medicare & Medicaid Services. Sep. 27, 2024 ⤶ ⤶

- U.S. Census Bureau Quick Facts: United States & Illinois.” U.S. Census Bureau, July 2023. ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data, December 2024. ⤶

- ”Medicare Advantage 2024 Spotlight: First Look” KFF.org Nov. 15, 2023 ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025. Accessed Oct. 3, 2025 ⤶

- “Illinois SB147” BillTrack50. Enacted July 31, 2021 ⤶

- “Illinois SB56” BillTrack50. Enacted Aug. 2, 2024 ⤶

- “2025 Medicare Choices” Illinois Department of Aging. Accessed Oct. 3, 2025 ⤶ ⤶ ⤶ ⤶

- “Medicare Supplement Guaranteed Issue Plans” Blue Cross and Blue Shield of Illinois. Accessed Oct. 3, 2025 ⤶