Find Maine Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Maine Health Insurance Marketplace Guide

This guide, including the FAQs below, is designed to help you understand your health insurance options in Maine, and we’ve included answers to numerous frequently asked questions below.

Maine’s ACA Marketplace health insurance plans are available on CoverME, a state-run website where four private health insurance companies offer plans.1 Most of the plans available through CoverME are Clear Choice plans, which means their cost-sharing is standardized to make plan comparisons easier.2

For 2026, the insurers that offer plans through CoverME implemented a weighted average rate increase of 23.9%3 (see details below for each insurer), but that’s only applicable to full-price premiums. Most enrollees get subsidies (premium tax credits), and after-subsidy rate increases were much larger because Congress allowed federal subsidy enhancements to expire at the end of 2025.

For 2027, one insurer is leaving the individual market in Maine. The remaining three insurers have proposed a weighted average rate increase of 16.8%, before subsidies are applied (details below).

Maine implemented a reinsurance program (MGARA) in 2019, which has been instrumental in keeping full-price (unsubsidized) premiums lower than they would have been without the reinsurance program. As of 2023, Maine merged its individual and small group health insurance markets, with MGARA reinsurance now covering both markets.4

The Maine Bureau of Insurance noted that the state received more federal MGARA funding than expected in 2024. This allowed them to reset the reinsurance parameters for 2024 and 2025, so that MGARA would pay 75% of eligible claims, instead of 55%.5 For 2026, however, the reinsurance program pays 60% of eligible claims, meaning the rate reduction due to reinsurance is slightly smaller than it was in 2025.6 (To be clear, overall premiums still increased for 2026, but overall rates would be higher still if the reinsurance program didn’t exist.)

Frequently asked questions about health insurance in Maine

Who can buy Marketplace health insurance in Maine?

To qualify for health coverage through the Marketplace in Maine, you must:9

- Be a Maine resident

- Be either a United States citizen or national, or be lawfully present

- Not be incarcerated

- Not have Medicare coverage

Eligibility for financial assistance (premium subsidies and cost-sharing reductions) will depend on your household income. In addition, to qualify for financial assistance with your Marketplace plan you must:

- Not have access to affordable employer-sponsored health insurance. If your employer offers coverage but you feel it’s too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies in the Marketplace.

- Not be eligible for MaineCare (Medicaid/CHIP).

- Not be eligible for premium-free Medicare Part A.10

- File a joint tax return with your spouse if you’re married.11 (with very limited exceptions)12

- Not be able to be claimed by someone else as a tax dependent.11

When can I enroll in an ACA-compliant plan in Maine?

In Maine, the open enrollment period for 2026 individual/family health coverage ended on January 15, 2026.

A federal rule change will shorten the open enrollment period, starting in the fall of 2026. At that point, open enrollment will no longer be allowed to continue past December 31, and all plans selected during open enrollment will take effect January 1.13

Outside of open enrollment, a special enrollment period is necessary to enroll or make changes to your coverage. In most cases, a qualifying life event is required to trigger a special enrollment period, but Native Americans can enroll in coverage at any time. Learn more in our comprehensive guide to special enrollment periods.

Maine is one of several states where pregnancy is considered a qualifying event. In most states, birth is the qualifying event and the special enrollment period begins the day the baby is born. But in Maine, the expectant mother can enroll in coverage, as the confirmation of the pregnancy is considered a qualifying life event in Maine.14

Maine also enacted legislation in 2022 that created an “easy enrollment program,” allowing uninsured residents to check a box on their state tax return if they want to be contacted by the state about enrolling in health coverage. A special enrollment period is available if the person is not eligible for Medicaid and would thus need a special enrollment period to sign up for coverage.15 Several other states also have easy enrollment programs.

How do I enroll in a Marketplace plan in Maine?

To enroll in an ACA Marketplace plan in Maine, you can:

- Visit CoverME.gov – Maine’s health insurance marketplace to enroll in individual and family health plans. You can contact CoverME by phone at (866) 636-0355 if you need assistance.

- Purchase Marketplace coverage with the help of an insurance agent or broker, or a Maine Enrollment Assister.16

How can I find affordable health insurance in Maine?

To locate affordable health insurance options in Maine, consumers can enroll through the state’s ACA Marketplace (CoverME.gov).

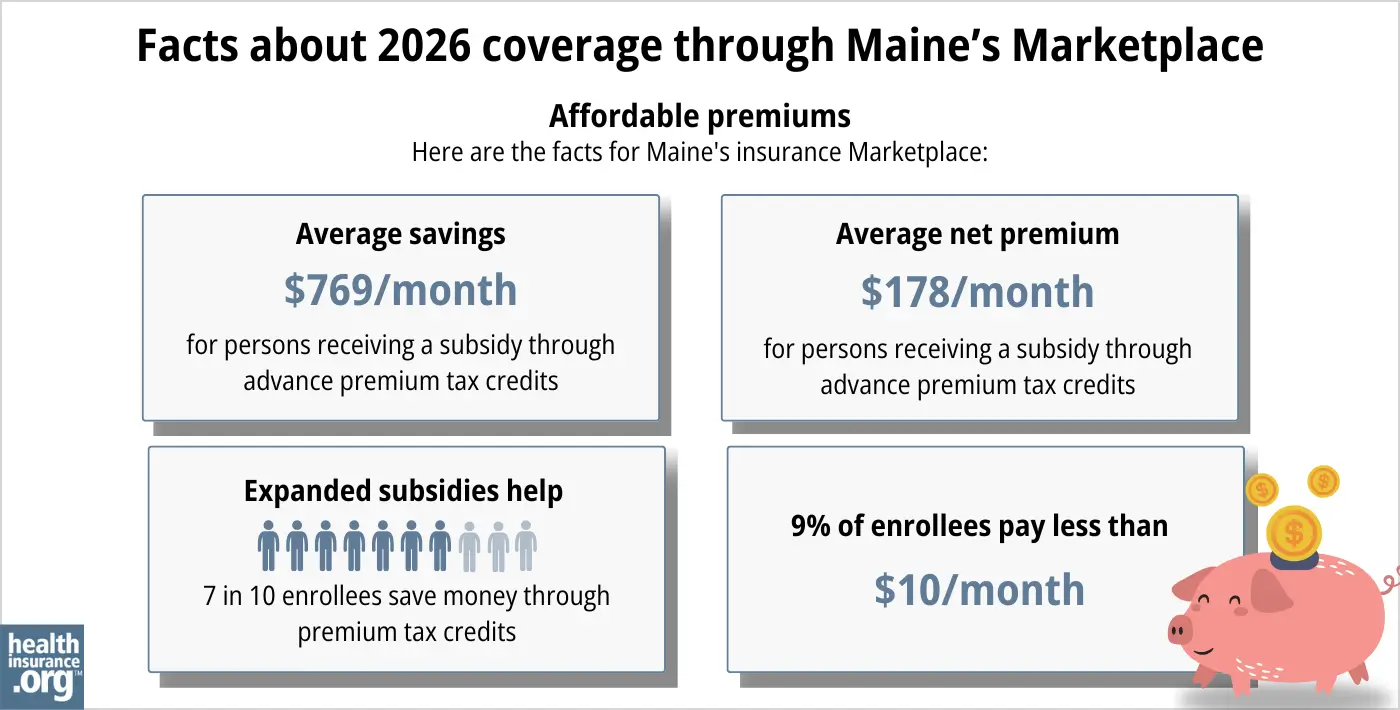

During the open enrollment period for 2025 coverage, nearly 85% of CoverME enrollees qualified for income-based premium subsidies.17

But for 2026, that dropped to 74%, due to the expiration of federal subsidy enhancements at the end of 2025. And although average after-subsidy premiums remained unchanged for 2026, CoverME noted that 58% of enrollees selected Bronze plans for 2026, up from 46% in 2025.18

(Bronze plans have lower premiums, but higher out-of-pocket costs; other state-run Marketplaces reported a similar uptick in Bronze plan enrollments for 2026.)

In addition to premium subsidies, the Affordable Care Act provides cost-sharing reductions (CSR) to Marketplace enrollees whose household income isn’t more than 250% of the poverty level, as long as they select a Silver-level plan. The CSR benefits result in lower out-of-pocket costs when you need medical care.19 During the open enrollment period for 2025 coverage, about 29% of CoverME enrollees selected plans with CSR benefits.17

Between the premium subsidies and cost-sharing reductions, you may find that an ACA-compliant plan obtained via Maine’s Health Insurance Marketplace plan will provide you with the best overall value.

Source: CMS.gov 20

Individual/family health plans in Maine are required to fully pay for a member’s first primary care visit and behavioral health care visit each year. The 2nd and 3rd primary care and behavioral health visits have to be covered with only a copay (no deductible or coinsurance). There is an exception for HSA-qualified high-deductible health plans, to comply with IRS rules that prohibit those plans from covering anything other than preventive care before the minimum deductible is met.21 (Note that as of 2026, all Marketplace Bronze and Catastrophic plans are considered HSA-eligible, nationwide, regardless of their plan design.)

Maine has expanded Medicaid under the ACA, so MaineCare (Medicaid) coverage is available to adults under age 65 with household income up to 138% of the federal poverty level. Children and pregnant women are eligible for MaineCare with higher household incomes.22

How many insurers offer Marketplace coverage in Maine?

Three insurers will offer coverage through Maine’s health insurance exchange for 2027. This is down from four in 2026,23 as Mending will no longer offer coverage after the end of 2026.24

The following insurers will offer coverage through CoverME for 2027:25

- Anthem Health Plans of ME (Anthem BCBS)

- Harvard Pilgrim Health Care Inc.

- Maine Community Health Options

Maine has one of just two remaining ACA-created CO-OPs (Community Health Options, or CHO).

As of 2026, CoverME’s carriers had the following market share:18

- Anthem: 48% of enrollees

- CHO: 28% of enrollees

- Harvard Pilgrim: 22% of enrollees

- Mending (Taro): 2% of enrollees (plans will terminate at the end of 2026)

Are Marketplace health insurance premiums increasing in Maine?

For 2027 coverage, the following average rate increases have been proposed by the insurers that offer coverage through CoverME, amounting to a weighted average proposed rate increase of 16.8%, before subsidies are applied.26

Maine’s ACA Marketplace Plan 2027 PROPOSED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Anthem Health Plans of ME (Anthem BCBS) | 17.9% |

| Harvard Pilgrim Health Care Inc. | 9.2% |

| Maine Community Health Options | 20.9% |

| Mending | Exiting market |

Source: Maine SERFF25

Average rate changes are calculated for full-price plans, before any premium subsidies are applied. But the majority of CoverME enrollees qualify for subsidies, which change each year to keep pace with the cost of the second-lowest-cost Silver plan. However, subsidies cover a smaller share of total premiums, and aren’t as widely available in 2026 and future years, because Congress did not extend the premium subsidy enhancements that had been in place since 2021.

The change in net (after-subsidy) premium depends on the specific plan (each carrier’s approved rate change is an average, across all plans they offer), geographic rating area, your age, and federal premium tax credits. But overall, Marketplace enrollees saw a sharp increase in after-subsidy premiums for 2026. This resulted in declining enrollment as well as a shift toward more Bronze plan selections.18

Here are some examples of the net premium increases that people saw in Portland, Maine for 2026:27

- 40-year-old earning $40,000:

- Lowest-cost plan in 2025 was $77/month

- Lowest-cost plan in 2026 is $112/month

- 60-year-old earning $63,000:

- Lowest-cost plan in 2025 was $283/month

- Lowest-cost plan in 2026 is $1,059/month (due to the subsidy cliff)

If the cost of your current plan increases, you can explore other plans in the exchange that may be less expensive and offer similar benefits.

For perspective, here’s a summary of how full-price premiums have changed in Maine over the years:

- 2015: Average decrease of 1%28

- 2016: Average increase of 0.7%29

- 2017: Average increase of 23.5%30

- 2018: Average increase of 25%31

- 2019: Average increase of 1%32 (Reinsurance took effect)

- 2020: Average decrease of 1.6%33

- 2021: Average decrease of 13.1%34

- 2022: Average decrease of 2.1%35

- 2023: Average increase of 11.4%36

- 2024: Average increase of 14.6%37

- 2025: Average increase of 8.6%5

- 2026: Average increase of 23.9%23

How many people are insured through Maine’s Marketplace?

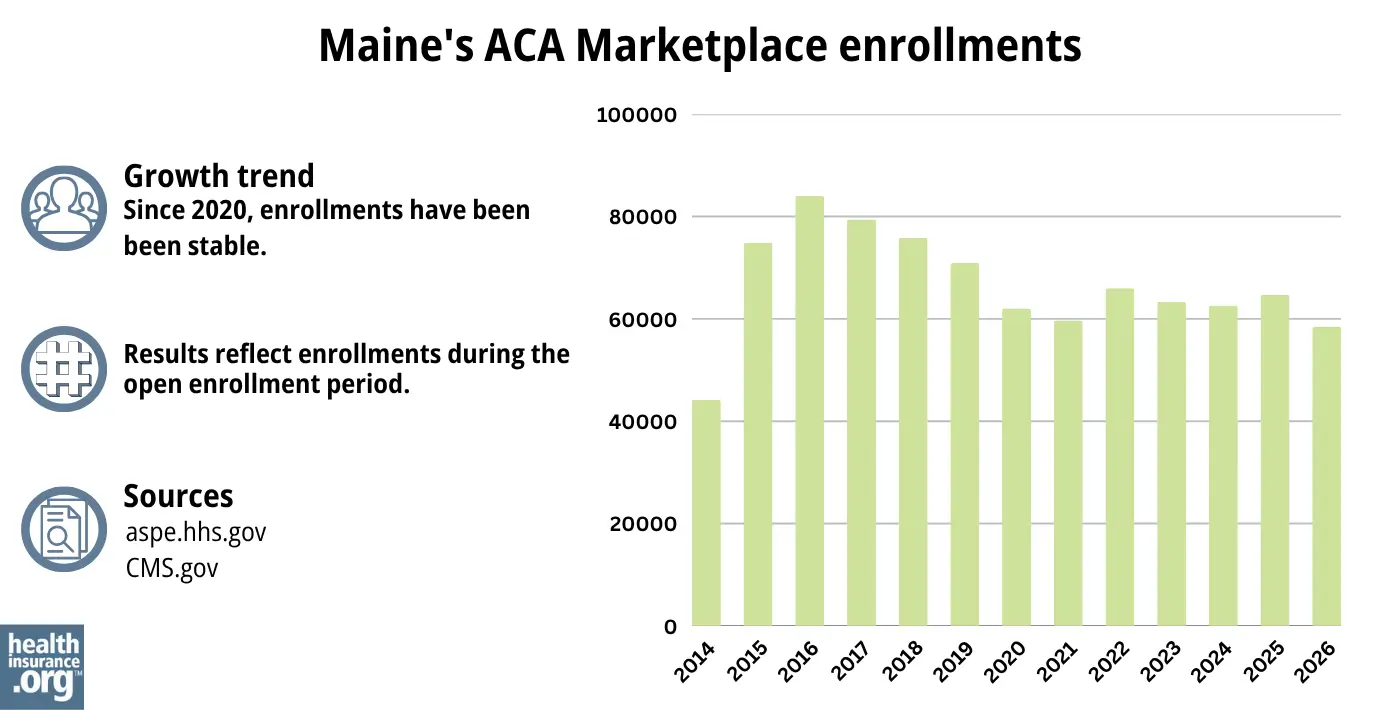

58,523 people enrolled in plans through CoverME during the open enrollment period for 2026 coverage.20

This was down almost 10% from the year before, when 64,678 people enrolled in plans through Maine’s exchange.17

Source: 2014,38 2015,39 2016,40 2017,41 2018,42 2019,43 2020,44 2021,45 2022,46 2023,47 2024,48 202549 202620

In most states, enrollment numbers had been steadily climbing in recent years, reaching significant record highs in 2025. But that wasn’t the case in Maine, where enrollment had hovered around the same level for several years (see chart below).

Maine was the only state where 2024 enrollment was lower than 2023 enrollment had been, with a 1.3% decrease.50 Maine officials noted51 that the enrollment decrease in 2024 was due to an increase in the income limits for children and young adults to qualify for Medicaid.52 As a result, some children and young adults were able to transition from CoverME plans to Medicaid starting in late 2023.

And CoverME enrollment did increase slightly in 2025, although certainly not to the sort of record-high levels it reached nationwide.53

But Maine did follow a similar pattern as most other states for 2026, where there was an overall enrollment decline nationwide, due to the expiration of the federal subsidy enhancements at the end of 2025.

What health insurance resources are available to Maine residents?

CoverME.gov Maine’s health insurance marketplace. Can also be reached at 1-866-636-0355.

State Exchange Profile: Maine The Henry J. Kaiser Family Foundation overview of Maine’s progress toward creating a state health insurance exchange.

Looking for more information about other options in your state?

Need help navigating health insurance options in Maine?

Explore more resources for options in ME including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”Health Insurance for Individuals and Families” Maine Bureau of Insurance. Accessed Dec. 9, 2025 ⤶

- Clear Choice Plans. CoverME. Accessed Mar. 22, 2026 ⤶

- ”2026 Individual (On/Off Exchange) Health Insurance Rate Filings” Maine Bureau of Insurance. Accessed Nov. 7, 2025 ⤶

- Federal Government Approves Maine’s Plan to Improve Health Insurance for Small Businesses. State of Maine, Office of Governor Mills. July 2022. ⤶

- ”Maine Bureau of Insurance Approves 2025 Health Insurance Rates for Individuals and Small Groups” Maine Bureau of Insurance. Aug. 26, 2024 ⤶ ⤶

- ”Maine Bureau of Insurance Section 1332 Waiver Annual Public Forum” Maine Bureau of Insurance. June 30, 2025 ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”2026 Individual (On/Off Exchange) Health Insurance Rate Filings” Maine Bureau of Insurance. July 23, 2025 *The above is based on the most current data available. ⤶

- “Frequently Asked Questions” CoverME.gov, ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Nov. 7, 2025 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Nov. 7, 2025 ⤶ ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- ”Partner Talking Points: Impact to Maine’s Health Insurance Marketplace, CoverME.gov Upcoming Changes as a Result of Federal Actions” CoverME. Accessed Mar. 22, 2026 ⤶

- Special Enrollment Periods. CoverME. Accessed Nov. 7, 2025 ⤶

- Maine LD1390. BillTrack50. Enacted April 2022. ⤶

- Free, local help is available to understand your options and apply for coverage. CoverME. Accessed Nov. 7, 2025 ⤶

- ”2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 12, 2025 ⤶ ⤶ ⤶

- ”2026 Open Enrollment Overview” CoverME. Mar. 2026 ⤶ ⤶ ⤶

- “APTC and CSR Basics” CMS.gov, June 2024 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶

- Consumer’s Guide to Individual Major Medical Insurance in Maine. Maine Department of Professional and Financial Regulation. Accessed December 2023. ⤶

- ”Medicaid, Children’s Health Insurance Program, & Basic Health Program Eligibility Levels” Centers for Medicare & Medicaid Services. December 2023. Accessed Nov. 7, 2025 ⤶

- ”2026 Individual (On/Off Exchange) Health Insurance Rate Filings” Maine Bureau of Insurance. Accessed Nov. 7, 2025 ⤶ ⤶

- ”Mending Health Notifies Maine Bureau of Insurance that it Will Cease Offering Health Insurance Plans” Maine Bureau of Insurance. June 8, 2026 ⤶

- ”SERFF Filings: MECH-134922366; HPHC-134972423; ATEM-134962217″ Maine SERFF. Accessed June 9, 2026 ⤶ ⤶

- ”SERFF Filings: MECH-134922366; HPHC-134972423; ATEM-134962217″ Maine SERFF. Weighted average rate increase based on enrollment numbers in SERFF filings: Maine CHO had 17,313 enrollees, Harvard Pilgrim had 13,374, and Anthem had 31,134. Accessed June 9, 2026 ⤶

- ”Compare Plans & Find Providers” (zip 04019) CoverME.gov Accessed Nov. 7, 2025 ⤶

- Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums. The Commonwealth Fund. December 2014. ⤶

- FINAL PROJECTION: 2016 Weighted Avg. Rate Increases: 12-13% Nationally* ACA Signups. October 2015. ⤶

- Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC). ACA Signups. October 2016. ⤶

- 2018 Rate Hikes. ACA Signups. October 2017. ⤶

- UPDATED: Maine: Thanks To Reinsurance, 2019 Rates Only Increasing 1.0%…But They WOULD Likely Be DROPPING By ~9.0% W/Out Sabotage. ACA Signups. July 2018. ⤶

- 2020 Rate Changes. ACA Signups. October 2019. ⤶

- 2021 Rate Changes. ACA Signups. October 2020. ⤶

- 2022 Rate Changes. ACA Signups. October 2021. ⤶

- Individual and Small Group Health Insurance Approved Rate Filings for 2023. Maine Bureau of Insurance. Accessed December 2023. ⤶

- 2024 Individual Health Insurance Rate Filings. Maine.gov. Accessed December 2023. ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶

- “Health Insurance Marketplaces 2024 Open Enrollment Report CMS.gov, March 22, 2024 ⤶

- “2024 Open Enrollment Overview” Coverme.gov. Feb. 1, 2024 ⤶

- “Help Spread the News to Families – MaineCare Eligibility Expanded for Children and Young Adults” Maine Department of Education. Dec. 18, 2023 ⤶

- ”Enrollment Growth in the ACA Marketplaces” KFF.org. Apr. 2, 2025 ⤶