Medicare in California

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in California

Medicare enrollment in California

Nationwide, nearly 70 million people are covered by Medicare1 – and more than 10% of them are in California.2 As of January 2026, nearly 7.2 million California residents had Medicare coverage.3

For most people, Medicare coverage enrollment goes along with turning 65. But Medicare eligibility is also triggered when a person has been receiving disability benefits for 24 months (people with amyotrophic lateral sclerosis (ALS) or end-stage renal disease (ESRD) do not have to wait 24 months for their Medicare enrollment). Nationwide, more than 90% of Medicare beneficiaries are eligible due to their age, while about 9% are eligible due to a disability.4 It’s lower in California, though, with only a little more than 6% of Medicare beneficiaries enrolled due to a disability.5

Note that under legislation California enacted in 2023, the state will pay Medicare Part A premiums for residents who are eligible for both Medicare and Medicaid (including some Medicare Savings Programs) and/or SSI benefits, if the person would otherwise have to pay a premium for Medicare Part A.6 (Most Medicare beneficiaries do not pay a premium for Part A, due to their work history.)

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how California’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

Medicare Advantage plan availability and enrollment in California

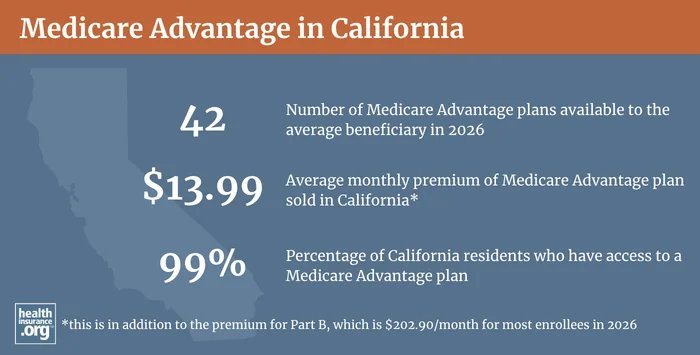

There are two counties in California where Medicare Advantage plans are not available in 2026,7 but 99.9% of California’s Medicare beneficiaries have access to a Medicare Advantage plan in 2026.8

About 51% of California Medicare beneficiaries had Medicare Advantage coverage as of January 20265 this is about the same as the nationwide average.9 As of January 2026, there were 3,682,589 California residents with private Medicare Advantage coverage, while the other 3,489,060 beneficiaries had coverage under Original Medicare.10

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in California by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in California

There are 22 insurers in California that offer Medigap plans.11 And as of 2023, about 598,000 Original Medicare beneficiaries in California had Medigap coverage.12

Learn more about how Medigap plans are standardized and what they cover.

Unlike other private Medicare coverage (Medicare Advantage plans and Medicare Part D plans), federal rules do not provide an annual open enrollment window for Medigap plans. Instead, federal rules provide a one-time six-month window when Medigap coverage is guaranteed-issue. This window starts when a person is at least 65 and enrolled in Medicare Part B (you must be enrolled in both Part A and Part B to buy a Medigap plan).

However, California law has long given Medigap enrollees an annual window, following their birthday, when they can switch to any other Medigap plan with equal or lesser benefits, without medical underwriting. This window used to be 30 days long, but legislation enacted in 2019 extended it to 60 days, as of 2020. California is one of several states that have this type of “birthday rule” that allows Medigap enrollees an opportunity to make limited plan changes without underwriting.

People who aren’t yet 65 can enroll in Medicare if they have amyotrophic lateral sclerosis (ALS) or end-stage renal disease (ESRD), or if they’re disabled and have been receiving disability benefits for at least two years, and almost 464,000 Medicare beneficiaries in California are under 65.13 Federal rules do not guarantee access to Medigap plans for people who are under 65, but the majority of the states, including California, have stepped in to ensure at least some access to private Medigap plans for disabled enrollees under the age of 65.

For Medicare beneficiaries in California who are under age 65, Article 6 (Section 10192.11) of California’s insurance statute requires Medigap insurers in the state to offer at least plans A, B, D, and G (if offered by the company to any applicants; note that this used to be plans A, B, C, and F, but S.B.784 was enacted in 2019 to swap Plans C and F for Plans D and G, since Plans C and F are no longer available – nationwide – to newly-eligible Medicare beneficiaries as of 2020; the requirement to make plans C and F – if offered by the insurer – available is still applicable for disabled Medicare beneficiaries who became eligible for Medicare prior to 2020). The insurers must also offer either plan K or Plan L, if offered by the company, or Plan M or Plan N, if offered by the company. But none of these provisions apply to Medicare beneficiaries under age 65 who are eligible for Medicare due to having end-stage renal disease (kidney failure).

This is important, because prior to 2021, federal rules also allowed Medicare Advantage plans to reject new applicants with end-stage renal disease, unless the plan was a special needs plan specifically designed for ESRD patients (such plans were not available in most of the state, meaning that ESRD patients had no option to cap their out-of-pocket costs unless they had access to a supplemental employer-sponsored or retiree plan). But this changed as of 2021, under the 21st Century Cures Act. Starting with 2021 coverage, Medicare Advantage plans are guaranteed-issue for all Medicare beneficiaries, including those with ESRD.14

California’s statute allows Medigap insurers to charge higher premiums for people under age 65. But coverage must be guaranteed-issue during the six months after a person enrolls in Medicare Part B (regardless of age) or the six months after a person is determined to be retroactively eligible for Medicare Part B. And insurers cannot pay differing broker commissions based on the age of the Medigap enrollee (ie, insurers are not allowed to use lower commissions to dissuade brokers from selling Medigap plans to people under age 65).15

Although the Affordable Care Act eliminated pre-existing condition exclusions in most of the private health insurance market, those regulations don’t apply to Medigap plans. Medigap insurers can impose a pre-existing condition waiting period of up to six months, if you didn’t have at least six months of continuous coverage prior to your enrollment. And if you apply for a Medigap plan after your initial enrollment window closes (assuming you aren’t using California’s “birthday rule” or eligible for one of the limited federal guaranteed issue rights),16 the insurer can look back at your medical history in determining whether to accept your application, and at what premium.

Medicare Part D plan availability and enrollment in California

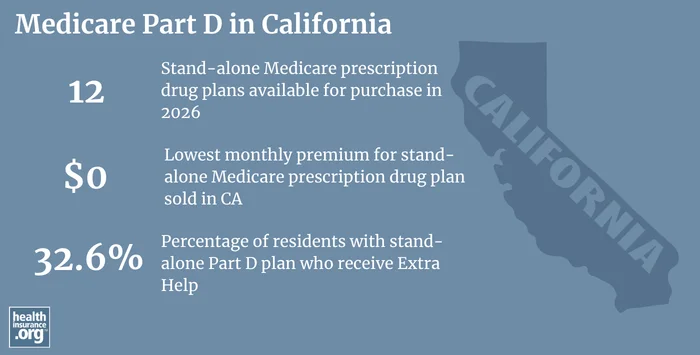

Insurers in California are offering 12 stand-alone Part D plans for sale in 2026.17 With the lowest monthly premiums starting at $0/month.18

As of January 2026, there were more than 2,494,219 Medicare beneficiaries in California with Part D prescription coverage, and another 3,546,493 had Part D coverage as part of their Medicare Advantage plans.5

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in California

Need help with Medicare enrollment in California, or have questions about Medicare eligibility in California?

- HICAP, California’s Health Insurance Counseling and Advocacy Program, is a helpful resource. Access their website or call 1-800-434-0222.

- California’s Department of Insurance, which oversees Medigap plans in California, has a helpful summary of state rules and regulations related to Medigap plans, and a general guide to Medigap plans in California.

- HICAP and the California Department of Aging also have a helpful toolkit for avoiding Medicare fraud and abuse.

- The Medicare Rights Center website provides information geared to Medicare beneficiaries, caregivers, and professionals.

Looking for more information about other options in your state?

Need help navigating health insurance options in California?

Explore more resources for options in CA including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data, Accessed Apr. 23, 2026. ⤶

- “Medicare Monthly Enrollment, January 2026 – California” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶

- “Medicare Monthly Enrollment, January 2026 – California” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶

- “Medicare Monthly Enrollment” Centers for Medicare & Medicaid Services. Accessed April 2026. ⤶

- “Medicare Monthly Enrollment” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶ ⤶ ⤶

- “Medicare Part A buy-in and automatic enrollment of Supplemental Security Income recipients into Qualified Medicare Beneficiary Program” California Department of Health Care Services. December, 2024. ⤶

- “Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings” KFF.org. Dec. 9, 2025 ⤶

- “Fact Sheet: Medicare Open Enrollment, 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶

- “Medicare Monthly Enrollment” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶

- “Medicare Monthly Enrollment” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶

- “List of Medicare Supplement Insurance Companies” California Department of Insurance. Accessed Apr. 23, 2026 ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Medicare Monthly Enrollment, January 2026 – California” Centers for Medicare & Medicaid Services Data, Accessed Apr. 23, 2026 ⤶

- “I have end-stage renal disease (ESRD). What are my coverage options under Medicare and how long does my Medicare coverage last?” KFF.org. Sep. 1, 2025 ⤶

- “ARTICLE 6. Medicare Supplement Policies” (Subsection d). California Legislative Information. Accessed Apr. 23, 2026 ⤶

- “Get ready to buy, Your Medigap Open Enrollment Period” Medicare.gov. Accessed Apr. 23, 2026 ⤶

- “Fact Sheet: Medicare Open Enrollment, 2026” KFF.org September 26, 2025 ⤶

- “Fact Sheet: Medicare Open Enrollment, 2026” Centers for Medicare & Medicaid Services. September 26, 2025 ⤶