Medicare in Colorado

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Colorado

Medicare enrollment in Colorado

Nationwide, almost 70 million people are enrolled in Medicare.1 As of January 2026, there were 1,076,907 residents with Medicare in Colorado.2

More than 93% of people with Medicare in Colorado are eligible due to their age (i.e., being at least 65), while less than 7% are eligible due to a disability, including a diagnosis of end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS).2 Nationwide, about 91% of Medicare beneficiaries are eligible due to age, and 9% are eligible due to disability.3

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Colorado’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

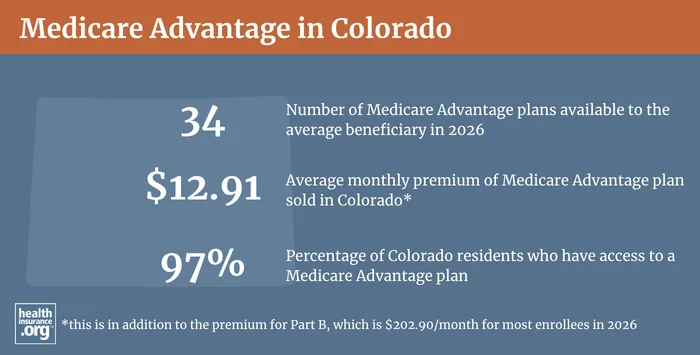

Medicare Advantage plan availability and enrollment in Colorado

Nationwide, 51% of all Medicare beneficiaries had Medicare Advantage plans as of January 2026.1 In Colorado, Medicare Advantage was a little more popular, with 52% of the state’s Medicare beneficiaries enrolled in Medicare Advantage plans.2 The other 48% of Colorado’s Medicare beneficiaries had opted instead for coverage under Original Medicare.

Medicare Advantage plans are provided by private insurers, which each have their own service area, so plan availability varies by area. There are Medicare Advantage plans available in most parts of Colorado in 2026, although there are eight counties where there are no individual Medicare Advantage plans available. But the average Medicare beneficiary in Colorado can choose from among 34 Medicare Advantage plans in 2026.4

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Colorado by contacting a licensed agent.

Medicare supplement (Medigap) plan availability in Colorado

For 2026, there are 30 insurers in Colorado offering Medicare supplement (Medigap) policies.5 And as of 2023, there were 233,787 Medicare beneficiaries in Colorado who had Medigap coverage, according to an AHIP analysis.6

Learn about how Medigap plans are standardized and what they cover.

Medigap policies can be priced using attained-age rating, issue-age rating, or community rating. Colorado does not require insurers to use a particular approach, so most Medigap insurers in Colorado use attained-age rating, which means that a person’s premiums increase as they get older. There are a handful of insurers in the state that use community rating (rates don’t vary with age) or issue-age rating (rates are based on the age the person was when they enrolled).7

Under federal rules, people are granted a six-month window during which they can enroll in a Medigap policy regardless of their medical history. This window starts when they’re at least 65 and enrolled in Medicare Part B. Federal rules do not, however, guarantee access to a Medigap policy if you’re under 65 and eligible for Medicare as a result of a disability.8

To address this, the majority of the states have implemented rules ensuring at least some access to Medigap policies for people who are under age 65.

Colorado statute (see 3 CCR 702-4 Series 4-3 Section 10) was changed in 2003 to ensure access to Medigap for people under age 65. Colorado requires Medigap insurers to offer all of their plans to people under age 65, with the same six-month enrollment window that applies to people who are aging onto Medicare. So a person under age 65 who becomes eligible for Medicare in Colorado has six months, starting when they’re enrolled in Medicare Part B, to sign up for a guaranteed-issue Medigap plan.

Although Medigap plans are guaranteed-issue for people under 65 during their six-month enrollment window, insurers can charge higher premiums for people under 65.9 Colorado publishes an annual rate comparison sheet for Medigap policies, making it easy to see how much more expensive the policies are for people under 65.7

However, the state does regulate the extent to which premiums can be higher for people under 65, with extensive rules governing what an insurer can charge as a “credibility-weighted average age premium rate” (see Section 10(E) of the statute).

Disabled Medicare beneficiaries have access to the normal Medigap open enrollment period when they turn 65. At that point, they have access to any of the available Medigap plans, at the standard age-65 rates.

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

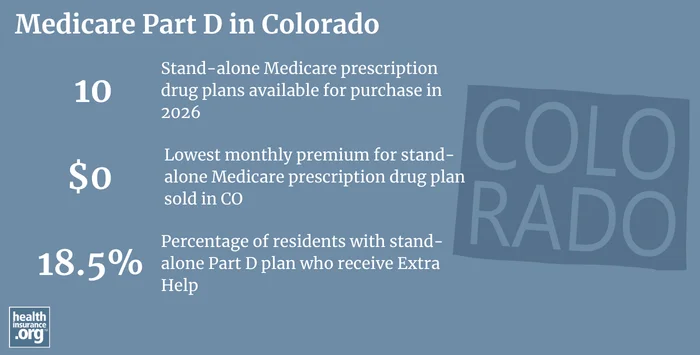

Medicare Part D plan availability and enrollment in Colorado

As of January 2026, there were 343,815 Colorado Medicare beneficiaries enrolled in stand-alone Medicare Part D prescription drug plans, and another 526,691 beneficiaries had Medicare Part D prescription drug coverage integrated with their Medicare Advantage plans. In total, 870,506 Colorado Medicare beneficiaries had Part D prescription drug coverage.2

For 2026 coverage, there are 10 stand-alone Medicare Part D prescription drug plans available in Colorado, with premiums starting at $0.10

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Colorado

If you have questions about Medicare eligibility in Colorado or Medicare enrollment in Colorado, you contact the Colorado State Health Insurance Assistance Program. (There are offices in each county.)

The Colorado Division of Insurance also maintains a useful Senior Publications page that includes a variety of helpful resources and information to address questions you might have about Medicare coverage in Colorado.

The Colorado Division of Insurance also regulates Medigap plans in the state, although those plans must also conform to the federal government’s standardization rules, as described above. (The governance of Medicare Advantage and Medicare Part D prescription drug plans mostly lies with the federal government, the state is only responsible for licensing the insurers that offer these plans and ensuring they remain financially solvent.)

This page is a comprehensive resource that details how Colorado Medicaid can provide financial assistance to Medicare beneficiaries in the state who have limited income and assets.

Looking for more information about other options in your state?

Need help navigating health insurance options in Colorado?

Explore more resources for options in CO including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – National” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶

- “Medicare Monthly Enrollment – Colorado” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – U.S” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org Dec. 9, 2025 ⤶

- “Colorado 2025-2026 Medigap Premium Charts” (link will download the chart). Colorado Division of Insurance. Accessed May 14, 2026 ⤶

- “The State of Medicare Supplement Coverage” AHIP, Page 11. May 2025 ⤶

- “Colorado 2025-2026 Medigap Premium Charts” (link will download the chart). Colorado Division of Insurance. Accessed May 14, 2026 ⤶ ⤶

- “Choosing a Medigap Policy” Page 10. Medicare.gov. Accessed May 14, 2026 ⤶

- ”Medicare Supplement Insurance Policies in Colorado” Colorado Division of Insurance. Sep. 2025 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶