Medicare in Connecticut

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Connecticut

Medicare enrollment in Connecticut

As of February 2026, Medicare enrollment in Connecticut stood at 776,948 people.1 As is the case nationwide, Medicare enrollment in Connecticut is comprised mostly of people who are eligible due to their age (being at least 65).

But younger people can gain Medicare eligibility if they have end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS), or after they’ve been receiving disability benefits for 24 months. In Connecticut, about 8% of beneficiaries are eligible due to disability rather than age.1

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Connecticut’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

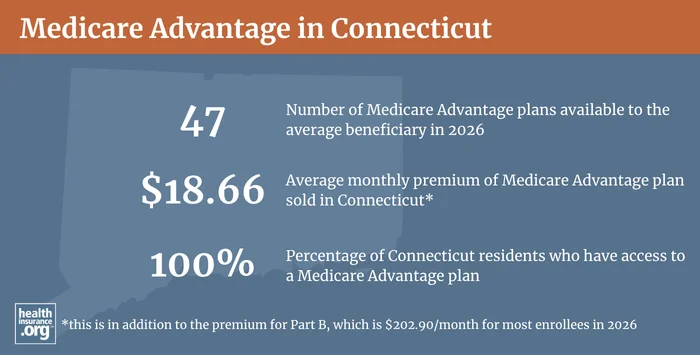

Medicare Advantage plan availability and enrollment in Connecticut

Nationwide, 51% of all Medicare beneficiaries were enrolled in Medicare Advantage plans as of February 2026.2

Medicare Advantage enrollment in Connecticut is slightly higher than the national average at 57%.1

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Connecticut by contacting a licensed agent.

Medicare supplement (Medigap) plan availability in Connecticut

Eight insurers offered Medigap plans in Connecticut in 2026.3

Although Medigap plans are sold by private insurers, the plans are standardized under federal rules, with ten different plan designs (differentiated by letters, A through N). The benefits offered by a particular plan (Plan G, Plan K, etc.) are the same regardless of which insurer sells the plan.

Prices vary from one insurer to another,3 but Connecticut law (Chapter 700c, Section 38a-473) requires insurers to use community rating: rates cannot vary based on age, gender, or health status. Connecticut is one of nine states where Medigap plans must be community rated.4

Unlike other private Medicare coverage (Medicare Advantage and Medicare Part D plans, which cover prescription drugs), federal rules do not grant an annual open enrollment window for Medigap plans. Instead, federal rules provide a one-time six-month window when Medigap coverage is guaranteed issue, starting when a person is at least 65 and enrolled in Medicare Part B. But consumer protections are much stronger in Connecticut: All Medigap plans in Connecticut are sold on a guaranteed-issue basis at all times, and with community rating. So Connecticut residents can switch from one Medigap plan to another, regardless of their health.5

Connecticut is one of only four states that require continuous or annual guaranteed issue access to all Medigap plans for all Medicare beneficiaries who are at least 65 years old.6 But the tradeoff is that Medigap is also more expensive in Connecticut than in most other states.4

People who aren’t yet 65 can enroll in Medicare if they’re disabled and have been receiving disability benefits for at least two years (the 24-month wait does not apply if they have ALS or end-stage renal disease), and about 8% of Connecticut Medicare beneficiaries are under age 65.7 Federal rules do not guarantee access to Medigap plans for people who are under 65, but the majority of the states – including Connecticut – have implemented rules to ensure that disabled Medicare beneficiaries have at least some access to Medigap plans.

Under Connecticut law (Chapter 700c, Section 38a-495c) Medigap insurers must offer Plan A to disabled beneficiaries who are under age 65. And if the company offers Plans B or D (or C if the beneficiary became eligible for Medicare prior to 2020) it must also offer those plans to disabled beneficiaries under age 65.8 This page shows which plans each insurer offers; note that many of them do not offer plans B, D, or C, meaning that the only plan they would offer to beneficiaries under 65 would be Plan A.

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

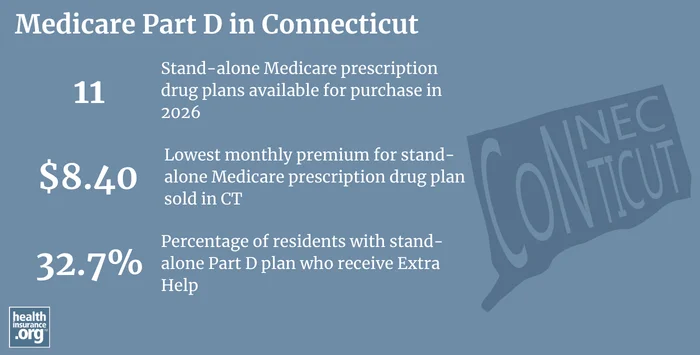

Medicare Part D plan availability and enrollment in Connecticut

There are 11 stand-alone Medicare Part D plans available in Connecticut for 2026 coverage, with premiums that start at $8.40/month.9

More than 660,000 Medicare beneficiaries in Connecticut had Part D coverage as of February 2026.1 At that point, 348,250 Connecticut Medicare beneficiaries had Part D coverage via Medicare Advantage plans with integrated Part D coverage, while 311,992 had stand-alone PDP coverage.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Connecticut

These resources provide free assistance and information about Medicare programs and availability in Connecticut.

- CHOICES (Connecticut’s program for Health insurance assistance, Outreach, Information and referral, Counseling, Eligibility Screening) answers questions about Medicare coverage in Connecticut.

- Our guide to Medicare’s annual open enrollment period is a summary of what you need to know about the fall enrollment window for Medicare Part D plans and Medicare Advantage plans.

- Connecticut’s overview of Medicare includes a summary of important dates and links to various resources for Medicare beneficiaries in Connecticut.

- Connecticut’s overview of Medicare Savings Programs is helpful for Connecticut Medicare beneficiaries with modest incomes and assets.

- The Medicare Rights Center website provides information geared to Medicare beneficiaries, caregivers, and professionals.

Looking for more information about other options in your state?

Need help navigating health insurance options in Connecticut?

Explore more resources for options in CT including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Connecticut” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – National” Centers for Medicare & Medicaid Services Data. Accessed May 2026 ⤶

- “Monthly Medicare Supplement rates for Standardized Plans” Connecticut Insurance Department. Updated May 27, 2026 ⤶ ⤶

- “Key Facts About Medigap Enrollment and Premiums for Medicare Beneficiaries” KFF.org. Oct. 18, 2024 ⤶ ⤶

- “Medigap Fact Sheet” Connecticut Insurance Department. Accessed May 29, 2026 ⤶

- “Access to Medicare Supplemental Insurance Policies (Medigaps)” Medicare Rights Center. Accessed May 29, 2026 ⤶

- “Medicare Monthly Enrollment – Connecticut” Centers for Medicare & Medicaid Services Data. Accessed May 29, 2026 ⤶

- “Monthly Medicare Supplement rates for Standardized Plans” Connecticut Insurance Department. Updated May 27, 2026 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶