Medicare in Tennessee

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Tennessee

Medicare enrollment in Tennessee

As of January 2026, Tennessee Medicare enrollment stood at 1,517,648,1 including those with Original Medicare and those with Medicare Advantage plans.

Of Tennessee’s Medicare beneficiaries, 88% are eligible based on their age (i.e., being at least 65 years old), while the other 12% percent are eligible due to a disability1 (24+ months of receiving Social Security Disability Insurance, or a diagnosis of amiotrophic lateral sclerosis (ALS) or end-stage renal disease).

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Tennessee’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

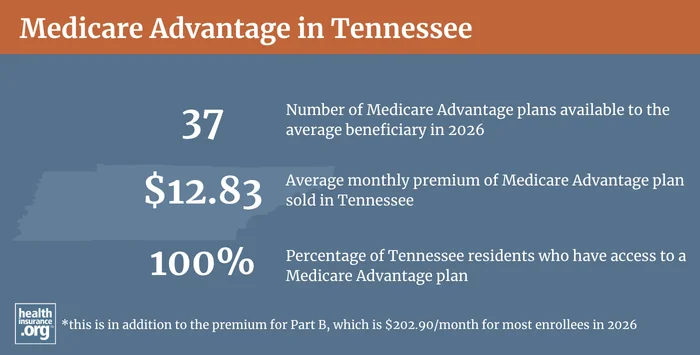

Medicare Advantage plan availability and enrollment in Tennessee

As of January 2026, 54% of the people enrolled in Medicare in Tennessee had Medicare Advantage plans.1 Nationwide, about 51% of Medicare beneficiaries have Medicare Advantage plans.2

The availability of Medicare Advantage plans in Tennessee varies from one county to another, but the market is quite robust throughout the state, and Medicare Advantage plans are available throughout the state. The average Medicare beneficiary in Tennessee can choose from among 37 Medicare Advantage plans in 2026.3

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Tennessee by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in Tennessee

There are 29 insurers offering Medigap plans in Tennessee in 2026.4 And according to an AHIP analysis, 308,365 people had Medigap coverage in Tennessee as of 2023.5

The Tennessee Department of Commerce and Insurance has a webpage where Medigap annual rate changes are displayed (including for plans that are no longer sold to new applicants), but it was most recently updated for 2024.

Medigap plans are standardized under federal rules,6 and people are granted a six-month enrollment window (which starts when they’re at least 65 years old and enrolled in Medicare Part A and Part B), during which Medigap coverage is guaranteed issue, and premiums cannot vary according to the applicant’s health. Federal rules do not, however, guarantee access to a Medigap plan if you’re under 65 and eligible for Medicare as a result of a disability.

But Tennessee is among the majority of the states that have adopted rules to ensure that people under age 65 have at least some access to Medigap plans. Since 2011, under state law, Tennessee Medigap insurers that offer plans to people age 65 and older are required to offer all of the same plans to people under 65 who become eligible for Medicare as a result of a disability. Disabled Tennessee residents have the same six-month open enrollment window for Medigap as those who gain eligibility for Medicare due to their age. The six-month window starts when the person is enrolled in Medicare Part B, and coverage is guaranteed issue during the enrollment window.

However, Tennessee residents under age 65 are charged much higher premiums for their Medigap coverage. These beneficiaries have access to a second Medigap open enrollment period when they turn 65. At that point, they have access to all of the available plans with the age-65 rates, which will lower their premiums significantly.

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

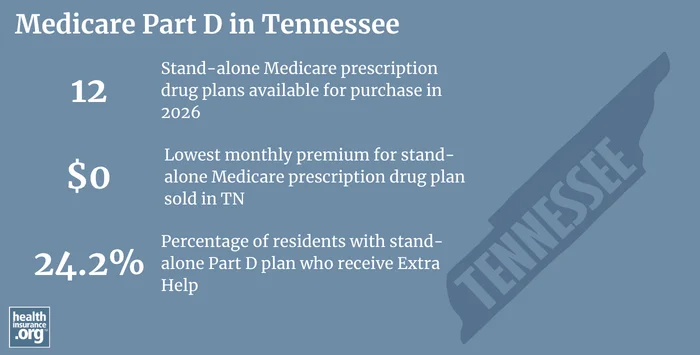

Medicare Part D plan availability and enrollment in Tennessee

Original Medicare does not cover outpatient prescription drugs. But Medicare beneficiaries can get prescription coverage via a Medicare Advantage plan, an employer-sponsored plan (offered by a current or former employer), or a stand-alone Part D prescription drug plan.

As of January 2026, there were 481,295 Medicare beneficiaries enrolled in stand-alone Part D prescription drug plans in Tennessee, and another 751,979 beneficiaries who had Part D coverage integrated with their Medicare Advantage plans.1 For 2026 coverage, there are 12 stand-alone Part D plans available in Tennessee, with premiums starting at $0 per month.7

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Tennessee

Questions about Medicare eligibility or enrollment in Tennessee?

- The Tennessee State Health Insurance Assistance Program for Medicare Participants can provide a variety of assistance and information, including answering your questions about Medicare eligibility in Tennessee and Medicare enrollment in Tennessee.

- The Tennessee Commission on Aging and Disability is also an excellent resource for Medicare beneficiaries in Tennessee, or people who will soon be eligible for Medicare in Tennessee.

- The Tennessee Department of Commerce and Insurance provides assistance and guidance for consumers with various insurance-related questions.

- The Medicare Rights Center provides assistance with and information about Medicare enrollment, eligibility, and benefits.

- This resource explains how Tennessee Medicaid can provide assistance to Medicare beneficiaries with limited income and assets.

Looking for more information about other options in your state?

Need help navigating health insurance options in Tennessee?

Explore more resources for options in TN including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Tennessee” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. May 2026. ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org. Dec. 9, 2025 ⤶

- “Supplement Insurance (Medigap) Plan A policies” Medicare.gov. Accessed May 14, 2026 ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Compare Medigap Plan Benefits” Medicare.gov. Accessed May 14, 2026 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶