Find Arkansas Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Arkansas Health Insurance Marketplace Guide

We designed this guide, including the FAQs below, to help you understand your health insurance coverage options in Arkansas. For many people, an Affordable Care Act (ACA) Marketplace plan – also called Obamacare – is a cost-effective choice.

Arkansas residents enroll in ACA-compliant plans through a state-based exchange/Marketplace that utilizes the federal enrollment platform (SBE-FP). This means people enroll through HealthCare.gov, but the state (via the Arkansas Insurance Department) oversees the exchange plans and runs its own outreach and assistance programs.1 Arkansas has used this approach since 2016.

Six private insurers offer plans through the Arkansas Marketplace in 2026.

Arkansas began requiring Marketplace insurers to use “premium alignment” (Silver loading) for 2026, adding a 46% load2 to the cost of Silver plans to account for the fact that the federal government stopped funding cost-sharing reductions back in 2017 (insurers were already adding a load factor for this, but Arkansas standardized it for 2026).

Premium alignment helps to ensure that premium subsidies are larger and that Bronze and Gold plans become more affordable starting in 2026 than they were in previous years.3 (See below for more details about premium changes for 2026.) For 2027, Arkansas reduced the CSR load to 40%.4 So Bronze and Gold plans will still be relatively more affordable than they were prior to 2026, but not quite to the same extent that they were in 2026.

Arkansas also purchases Marketplace health plans for people who are eligible for expanded Medicaid.

*Values displayed by this tool are from data generated by CMS and reflect 2026 Marketplace health plans purchased in each state. The values returned are averages based on the plans purchased by consumers of each selected state: subsidy and premium values vary based on factors such as zip code, age, household size, and income.

Arkansas Marketplace quick facts

Frequently asked questions about health insurance in Arkansas

Who can buy Marketplace health insurance in Arkansas?

To be eligible for health coverage through the Arkansas Marketplace, you must meet certain criteria. Typically, you can apply if you:7

- Reside in Arkansas

- Are either a U.S. citizen, U.S. national, or lawfully present in the U.S.

- Are not incarcerated

- Are not enrolled in Medicare

So most Arkansas residents are eligible to enroll in a Marketplace plan. However, a more important question for most people is whether they’re eligible for financial assistance (premium subsidies and cost-sharing reductions) in the Marketplace.

Eligibility for financial assistance depends on your income. In addition, to qualify for financial assistance with your Marketplace plan you must:

- Not have access to affordable employer-sponsored health insurance. If your employer offers coverage but you feel it’s too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies in the Marketplace.

- Not be eligible for Medicaid or CHIP.

- Not be eligible for premium-free Medicare Part A 8

- File a joint tax return with your spouse, if you’re married.9 (with very limited exceptions)10

- Not be able to be claimed by someone else as a tax dependent.9

When can I enroll in an ACA-compliant plan in Arkansas?

The open enrollment period for 2027 coverage is scheduled to run from November 1, 2026 to December 15, 2026, under a federal rule change that was finalized in 2025. However, that rule change was vacated by a judge in June 2026.11

So open enrollment might continue to have a January 15 deadline (as was the case for the last few years),12 but HHS could also appeal the vacatur.

Outside of open enrollment, you can only change plans or enroll in coverage if you qualify for a special enrollment period (SEP).

An SEP allows you to make plan changes outside open enrollment if you’ve had a qualifying life event, like getting married, having a baby, or losing other health coverage.13

Native Americans can enroll in Marketplace plans year-round, without needing a qualifying life event.

How do I enroll in a Marketplace plan in Arkansas?

If you’re eligible for an ACA Marketplace plan in Arkansas, you can enroll:

- Online through HealthCare.gov

- By phone at (800) 318-2596

- With the help of a local insurance agent/broker, Navigator, or certified application counselor

- Via an approved enhanced direct enrollment entity.14

How can I find affordable health insurance in Arkansas?

You can find affordable health plans in Arkansas on the ACA Marketplace (HealthCare.gov).

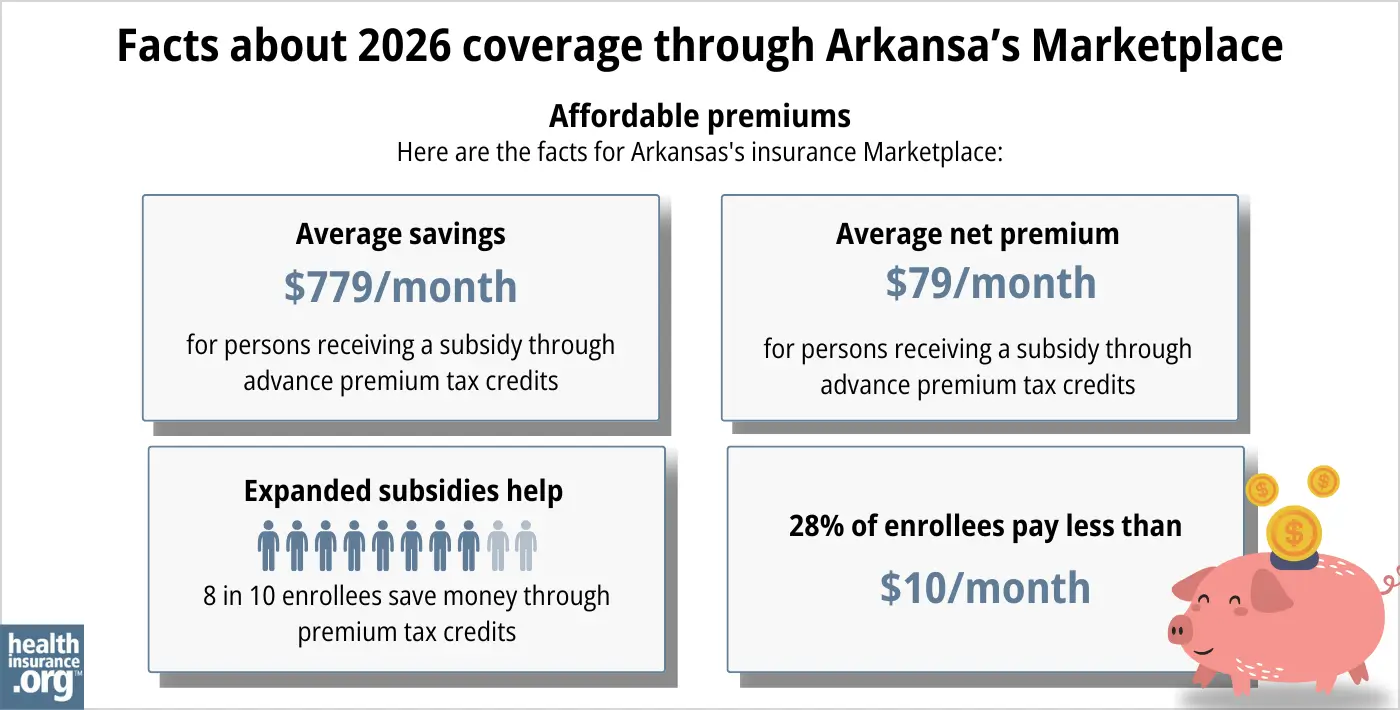

During the open enrollment period for 2026 coverage, 87% of Arkansas Marketplace enrollees were eligible for advance premium tax credits (APTC, or premium subsidies). The average subsidy amount was about $779/month, leaving the average subsidy-eligible enrollee paying only about $79/month for their coverage.15

Source: CMS.gov15

If your income isn’t more than 250% of the federal poverty level, you may also qualify for cost-sharing reductions (CSR) to lower your deductibles and out-of-pocket costs.16 During the open enrollment period for 2026 coverage, about 32% of Arkansas Marketplace enrollees selected a plan with CSR benefits.15

You may enroll in Medicaid coverage if eligible, and Medicaid enrollment continues year-round. Arkansas expanded Medicaid under the ACA, and the state purchases private Marketplace health plans (Blue Cross Blue Shield or Ambetter) for people who are eligible for expanded Medicaid. This program is called ARHOME.17

Short-term plans can be a lower-cost coverage option for people not eligible for Medicaid, Medicare, or subsidized Marketplace coverage. But it’s important to understand the drawbacks of short-term coverage before purchasing it, as these plans are not regulated by the ACA.

How many insurers offer Marketplace coverage in Arkansas?

The Arkansas health insurance Marketplace offers individual and family health plans from six insurers, although some are subsidiaries or licensees of a single parent entity:18

- Celtic Insurance Company (Ambetter)

- HMO Partners, Inc (Health Advantage)

- QCA Health Plan, Inc.

- QualChoice Life and Health Insurance Company, Inc.

- USAble Mutual Insurance Co. (AR Blue Cross & Blue Shield)

- USAble HMO, Inc. (Octave)

Each insurer sets its own coverage area, so different plans are available in each part of the state.

Are Marketplace health insurance premiums increasing in Arkansas?

The insurers that offer coverage through the Arkansas Marketplace have implemented the following average rate changes for 2026, before any subsidies are applied.18

Arkansas’ ACA Marketplace Plan 2026 APPROVED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Celtic Insurance Company (Ambetter) | 26.1% |

| HMO Partners, Inc (Health Advantage) | 12.3% |

| QCA Health Plan, Inc. | 27.5% |

| QualChoice Life and Health Insurance Company, Inc. | 29.8% |

| USAble Mutual Insurance Co. (AR Blue Cross & Blue Shield) | 16.9% |

| USAble HMO, Inc. (Octave) | 20.6% |

Source: Arkansas Insurance Department19

This amounts to an overall weighted average increase of 22.2%, before any subsidies are applied.20

The average rate changes are for full-price premiums. But most people in Arkansas receive subsidies to lower their costs, and the expiration of the federal subsidy enhancements resulted in a significant increase in net premiums for 2026. The average Arkansas Marketplace enrollee’s net premium was:

- $124/month in 202521

- $162/month in 202615 (despite the fact that many enrollees downgraded to Bronze plans)

But it’s important to note that Arkansas implemented a standardized premium alignment (Silver loading) approach for 2026, requiring insurers to add a 46% load to the cost of Marketplace Silver plans2 to account for the fact that the federal government stopped funding cost-sharing reductions back in 2017 (insurers were already adding a load factor for this, but Arkansas standardized it for 2026).3

Since premium subsidy amounts are based on the cost of the second-lowest Silver plan, increasing the prices for Silver plans results in larger premium subsidies for everyone who qualifies for premium subsidies. This helps to ensure that Bronze and Gold plans become more affordable than they were in previous years.3 (For 2027, the CSR load factor has been reduced to 40% in Arkansas.)4

Several states have mandated premium alignment rules, including Texas (40% load),22 Washington (43.5% load),23 and Vermont (41.9%).24 But the 46% load that Arkansas used for 2026 was the highest we’ve seen (to clarify, this is beneficial for consumers, because it results in a more significant increase in Silver plan rates, and thus a larger increase in subsidy amounts).

Here are examples of how net premiums changed in Arkansas for 2026, including the impact of the expiration of federal subsidy enhancements and the state’s new approach to premium alignment:25

40-year-old earning $40,000

- Lowest-cost plan in 2025: $84/month

- Lowest-cost plan in 2026: $0.04/month (impact of the federal subsidy enhancement expiration is more than offset by the new premium alignment rules in Arkansas, which make Bronze and Gold plans more affordable for people who get premium subsidies)

- Lowest-cost Gold plan in 2025: $224/month

- Lowest-cost Gold plan in 2026: $160/month (also due to the new premium alignment rule)

60-year-old earning $63,000

- Lowest-cost plan in 2025: $299/month

- Lowest-cost plan in 2026: $756/month (premium alignment doesn’t help here, because this person loses access to premium subsidies altogether due to the failure of Congress to extend the federal subsidy enhancements)

For perspective, here’s an overview of how unsubsidized average premiums have changed in Arkansas over the years:

- 2015: Average decrease of 2%.26

- 2016: Average increase of 4.4%.27

- 2017: Average increase of 9.1%.28

- 2018: Average increase of 17.5%.29

- 2019: Average increase of 4.1%.30

- 2020: Average increase of 2.3%.31

- 2021: Average increase of 3.4%.32

- 2022: Average increase of 4.4%.33

- 2023: Average increase of 5.9%.34

- 2024: Average increase of 4.1%.35

- 2025: Avearge increase of 6.2%.36

How many people are insured through Arkansas’ Marketplace?

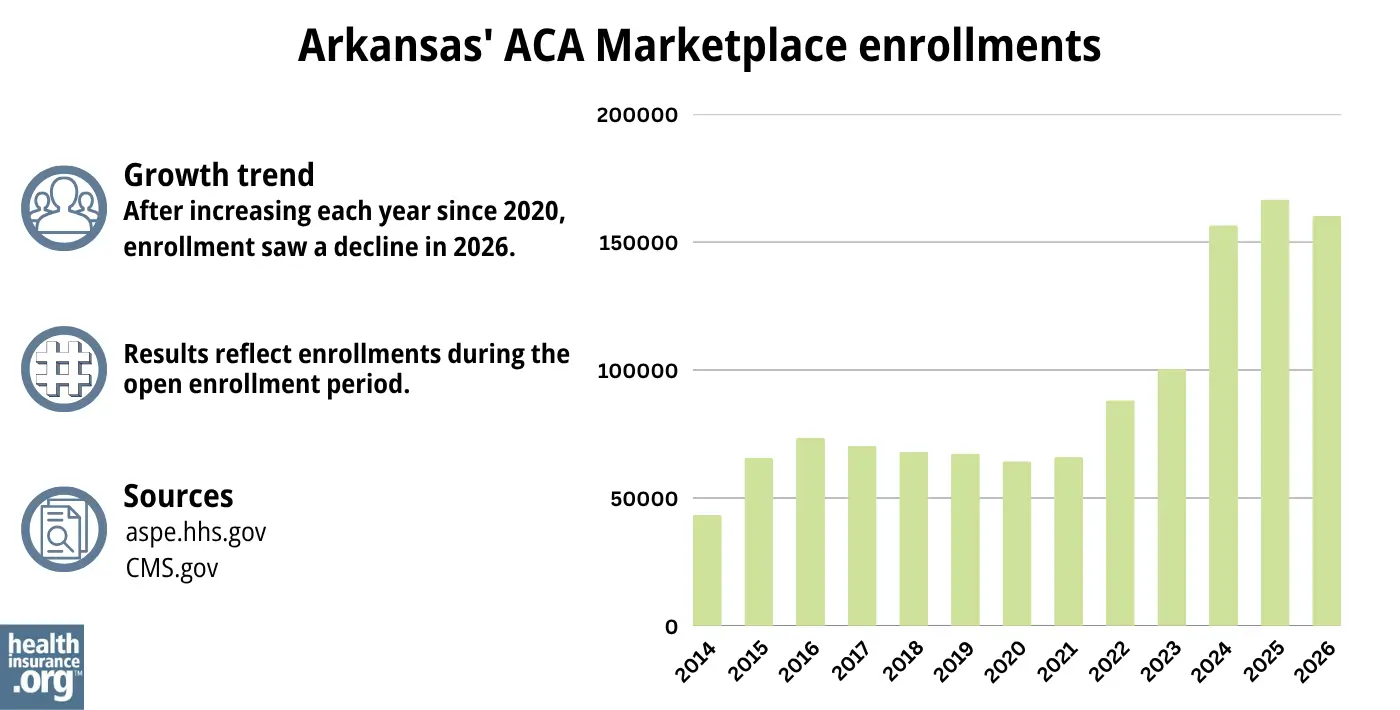

During the open enrollment period for 2026 coverage, 160,307 people enrolled in private plans through the Arkansas Marketplace.15

This was lower than 2025 enrollment, which had been a record high. (See chart below with historical enrollment data.)

The enrollment growth in recent years was driven in large part by the American Rescue Plan’s subsidy enhancements, which were extended through 2025 by the Inflation Reduction Act. These subsidy enhancements made coverage more affordable from 2021 through 2025. But their expiration at the end of 2025 resulted in higher net premiums for 2026, and fewer people signed up for coverage.

The enrollment spike in 2024 and 2025 was also partially due to the “unwinding” of the pandemic-era Medicaid continuous coverage rule. Medicaid disenrollments resumed in the spring of 2023, and Arkansas had completed the unwinding process by October 2023, with more than 427,000 people disenrolled from Medicaid.37

By April 2024, nearly 65,000 people had transitioned from Arkansas Medicaid to a private plan offered in the Arkansas Marketplace,38 helping to drive 2024 enrollment higher than it had been in recent years.

Source: 2014,39 2015,40 2016,41 2017,42 2018,43 2019,44 2020,45 2021,46 2022,47 2023,48 2024,49 202550 202615

What health insurance resources are available to Arkansas residents?

HealthCare.gov

This is the ACA Marketplace where you can enroll in a health insurance plan online. You may also get help by calling (800) 318-2596.

Arkansas Center for Health Improvement

Nonprofit focused on improving healthcare access and public health in Arkansas.

Arkansas Insurance Department Consumer Services Division

Regulates insurance companies and assists consumers. Can help with health insurance questions, complaints, and more.

ARKids First

Arkansas’ Children’s Health Insurance Program. Provides low-cost health coverage for children in families who earn too much for Medicaid but can’t afford other insurance.

Arkansas Senior Health Insurance Information Program

Provides local Medicare counseling and assistance. Can help answer questions, resolve issues, and enroll in Medicare plans.

Looking for more information about other options in your state?

Need help navigating health insurance options in Arkansas?

Explore more resources for options in AR including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- My Arkansas Insurance. Arkansas Insurance Department. Accessed June 16, 2026 ⤶

- ”Plan Year 2026 Individual, On-Marketplace Rate Filings” Arkansas Insurance Department. Mar. 7, 2025 ⤶ ⤶

- ”EXCLUSIVE: Arkansas Insurance Dept. going all in on Premium Alignment…but are they overplaying their hand?” ACA Signups. Sep. 15, 2025 ⤶ ⤶ ⤶

- ”Bulletin 6-2026, Plan Year 2027 Guidance for Applying Cost Sharing Reduction Load to Individual, On-Marketplace Silver Plans” Arkansas Insurance Department. Apr. 23, 2026 ⤶ ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Health Insurance Rate Changes for 2026” acasignups.net, October, 2025 *The above is based on the most current data available. ⤶

- ”A quick guide to the Health Insurance Marketplace” HealthCare.gov ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed June 16, 2026 ⤶

- Premium Tax Credit — The BasicsInternal Revenue Service. Accessed June 16, 2026 ⤶ ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- ”Columbus v. Kennedy; Memorandum Opinion” US District Court for the District of Maryland. June 12, 2026 ⤶

- “When can you get health insurance?” HealthCare.gov, 2023 ⤶

- “Understanding special enrollment periods” CMS.gov, March 2023 ⤶

- “Entities Approved to Use Enhanced Direct Enrollment” CMS.gov, Apr. 7, 2026 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files“ CMS.gov. March 2026 ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- ”APTC and CSR Basics” Centers for Medicare and Medicaid Services. June 2023. ⤶

- ”ARHOME” Arkansas Department of Human Services. Accessed June 16, 2026 ⤶

- ”Health Insurance Rate Changes for 2026” acasignups.net, October, 2025. ⤶ ⤶

- ”Health Insurance Rate Changes for 2026” acasignups.net. October, 2025 ⤶

- ”2026 Final Gross Rate Changes: Arkansas +22.2% (updated MANY times…)” ACA Signups. Oct. 9, 2025 ⤶

- ”2025 Marketplace Open Enrollment Period Public Use Files“ CMS.gov. Accessed June 16, 2026 ⤶

- ”Subchapter F. Rate Review for Health Benefit Plans, 28 TAC §3.505” Texas Department of Insurance. Accessed Dec. 17, 2025 ⤶

- ”Rule Making Order” Washington Office of the Insurance Commissioner. June 29, 2025 ⤶

- ”2026 FINAL Gross Rate Changes – Vermont: +6.7%, WAY down from 17.4% requested…but BCBS is on verge of insolvency??” ACA Signups. Aug. 29, 2025 ⤶

- ”See Plans & Prices” (zip code 72002). HealthCare.gov. Accessed Dec. 17, 2025 ⤶

- 2015 Projected Qualified Health Plan Individual Premium Rates for Arkansas. Arkansas Insurance Department. Accessed November 2023. ⤶

- Arkansas: Approved 2016 Rate Hikes Confirmed At 4.4% Weighted Avg. ACA Signups. August 2015. ⤶

- Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC). ACA Signups. October 2016. ⤶

- 2018 Rate Hikes. ACA Signups. October 2017. ⤶

- Arkansas: APPROVED 2019 ACA Rate Hikes: 4.1%, But Would Have DROPPED By ~1% W/Out #ACASabotage. ACA Signups. August 2018. ⤶

- Arkansas: *Approved* Avg. 2020 #ACA Exchange Rate Changes: 2.3% Increase. ACA Signups. September 2019. ⤶

- Arkansas: Approved Avg. 2021 #ACA Rate Changes: +3.4% Indy Market, -0.4% Sm. Group Market. ACA Signups. October 2020. ⤶

- Arkansas: Approved Avg. 2022 #ACA Premium Rate Changes: +4.4% Indy Market; +4.0% Sm. Group. ACA Signups. October 2021. ⤶

- Arkansas: (Updated) Final Avg. Unsubsidized 2023 #ACA Rate Changes: +5.9%. ACA Signups. July 2022. ⤶

- Arkansas *Final* Avg. Unsubsidized 2024 #ACA Rate Changes: +4.1%. ACA Signups. September 2023. ⤶

- ”Arkansas: *Final* avg. unsubsidized 2025 #ACA rate changes: +6.2% (updated)” ACA Signups. Sep. 19, 2024 ⤶

- Unwinding data for April, May, June, July, August, and September. Arkansas Department of Human Services. Accessed December 2, 2023. ⤶

- HealthCare.gov Marketplace Medicaid Unwinding Report. Centers for Medicare and Medicaid Services. Data through April 2024, Accessed Aug. 3, 2024 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶