Find Illinois Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Illinois Health Insurance Marketplace Guide

Starting November 1, 2025, for coverage effective in 2026, Illinois residents began using the state-run Get Covered Illinois website for enrollment, instead of HealthCare.gov.1 Existing HealthCare.gov accounts were transitioned to Get Covered Illinois, and enrollees were given instructions for logging into their new Get Covered Illinois accounts to select their coverage for 2026.2

Seven insurance companies are offering health insurance Marketplace coverage in Illinois for 2026,3 with service areas that vary quite a bit from one insurer to another. This is a decrease from 11 in 2025,4 due to the exit of Aetna CVS (two entities), Health Alliance, and Quartz, at the end of 2025.5

And for 2027, another insurer is exiting the Illinois Marketplace (See details below about premiums and carrier participation for 2027.)

Use this guide, including the FAQs below, to help you understand the Illinois Marketplace and choose the right health plan for you and your family. ACA Marketplace plans (also called Obamacare or exchange plans) are affordable choices for many people. Enrolling through the exchange/Marketplace is the only way to obtain a premium tax credit, which is income-based and available to most exchange enrollees.

Illinois ACA Marketplace quick facts

Frequently asked questions about health insurance in Illinois

Who can buy Marketplace health insurance in Illinois?

You can buy a health plan through the Illinois exchange if:8

- You reside in Illinois.

- You are a U.S. citizen or national.

- You are not incarcerated.

- You are not enrolled in Medicare.

Qualification for financial assistance, including premium subsidies and cost-sharing reductions (CSR), depends on your income and how it compares with the cost of the second-lowest-cost Silver plan in your area. This can vary based on where you live and your age. Moreover, to be eligible for financial aid for your Marketplace plan, you must:

- Not have affordable health coverage available through your job or your spouse’s job. If you have access to employer-sponsored insurance, but it seems too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might be eligible for premium subsidies on the Marketplace.

- Not qualify for Medicaid or CHIP.

- Not be eligible for premium-free Medicare Part A.9

- If married, file a tax return jointly with your spouse10 (with very limited exceptions)11

- Not be able to be claimed by someone else as a tax dependent.10

When can I enroll in an ACA-compliant plan in Illinois?

The next open enrollment period for Illinois ACA Marketplace individual and family health coverage will begin November 1, 2026, for coverage effective on January 1, 2027. The open enrollment window will have to end no later than December 31, due to a new federal rule that was finalized in 2025.

For 2026 coverage, open enrollment ended January 31, 2026 in Illinois. But enrollees whose 2025 HealthCare.gov coverage was automatically renewed — and who had not claimed their Get Covered Illinois account by February 1, 2026 — had until March 31, 2026 to pick a different plan.12 But that was a one-time provision, since Illinois switched to running its own Marketplace platform in the fall of 2025.

You can sign up for an exchange plan — or make changes to your coverage — outside of open enrollment if you meet special enrollment period (SEP) requirements. This generally means you must have a qualifying life event, such as losing your health insurance, getting married, or having a baby. American Indians and Alaska Natives can enroll anytime without a specific qualifying life event.

As of 2026, Illinois is among the states where pregnancy counts as a qualifying life event, triggering a special enrollment period.1314

Illinois is also among the states that have an easy enrollment program. Illinois residents can indicate on their state tax return whether they’d like their information to be shared with Illinois Medicaid and Get Covered Illinois (This is Step 12 on the Illinois state tax return) to determine eligibility for health coverage and facilitate enrollment.

This stems from legislation the state enacted in 2022.15 The program became available as of early 2023, when 2022 tax returns were being filed.

Prior to 2026, however, Illinois was not able to offer a special enrollment period for Marketplace plans in conjunction with the easy enrollment program, because the federally-facilitated exchange doesn’t have a way to incorporate state-specific SEP opportunities. That changed as of 2026, when Illinois started running its own exchange platform.

How do I enroll in a Marketplace plan in Illinois?

Here are the ways to enroll in a Marketplace health plan in Illinois:

- Online: You can sign up directly through Get Covered Illinois.

- By Phone: Dial 1-866-311-1119 to reach the Get Covered Illinois call center for enrollment assistance over the phone.

- In-person: Enrollment assistance is also available from brokers and Navigators who can answer your questions.16

How can I find affordable health insurance in Illinois?

Individuals and families who enroll in Marketplace coverage in Illinois can take advantage of two different types of income-based financial assistance:

- Premium subsidies: The ACA Marketplace is the only place where you can qualify for income-based subsidies known as Advance Premium Tax Credits (APTC) that help lower your monthly premiums. Eight out of 10 Illinois exchange enrollees were eligible for subsidies on 2026 plans, saving an average of $688 monthly with premium tax credits in Illinois. As a result, the average after-subsidy monthly premium was $142 for people who qualified for APTC.17

But because federal subsidy enhancements were allowed to expire at the end of 2025, subsidies don’t cover as much of enrollees’ premiums in 2026, and are not available to as many people. This has caused enrollees’ net premiums to increase significantly for 2026, even though many people downgraded to Bronze plans in an effort to keep premiums affordable.

Source: CMS.gov17

- Cost-Sharing Reductions: You may qualify for cost-sharing reductions (CSR) if your income is no more than 250% of the federal poverty level. CSRs help reduce your out-of-pocket costs, making coverage more affordable.

- Twenty-nine percent of Get Covered Illinois enrollees selected plans with CSR benefits during the open enrollment period for 2026 coverage.18 This was down from 51% the year before,19 because some people who previously had CSR benefits opted to downgrade to Bronze coverage for 2026 (which doesn’t include CSR benefits) to keep their monthly premiums affordable after federal subsidy enhancements expired.

Medicaid: Illinois residents may qualify for affordable Medicaid coverage if eligible.

Short-Term Health Insurance: Short-term health insurance is no longer available in Illinois, due to legislation the state enacted in 2024.20

How many insurers offer Marketplace coverage in Illinois?

Seven insurance companies offer Marketplace coverage in Illinois for 2026, with varying coverage areas:3

- Celtic Insurance Co./Ambetter (no Bronze plans offered in 2026)21

- Cigna HealthCare of Illinois, Inc. (all policies terminate at the end of 2026)

- Health Care Service Corporation (Blue Cross Blue Shield of Illinois)

- MercyCare HMO

- Molina Healthcare of Illinois, Inc.

- Oscar Health Plan, Inc.

- UnitedHealthcare

Six of the seven will continue to offer coverage in 202722 (see below for premium change details), but Cigna will not.

Illinois residents with 2026 coverage from Cigna will need to select a new plan for 2027, during the open enrollment period that begins November 1, 2026.

Eleven insurers offered Marketplace plans in Illinois in 2025, but four of them (including two Aetna entities) exited the market at the end of 2025,5 leaving seven participating insurers for 2026.3

Are Marketplace health insurance premiums increasing in Illinois?

The following average premium changes have been proposed for 2027 by the insurers that offer Marketplace coverage in Illinois, amounting to an overall average proposed rate increase of 14.1% (before subsidies are applied).23

Illinois’ ACA Marketplace Plan 2027 PROPOSED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Celtic Insurance Co. (Ambetter) | 9.2% |

| Cigna HealthCare of Illinois, Inc. | Exiting market |

| Health Care Service Corporation (Blue Cross Blue Shield of Illinois) | 14.9% |

| MercyCare HMO | 12.2% |

| Molina Healthcare of Illinois, Inc. | 1.8% |

| Oscar Health Plan, Inc. | 12.7% |

| UnitedHealthcare | 12.4% |

Source: Illinois Department of Insurance22

Illinois historically had very little transparency in terms of rate filing details for health plans, and state regulators did not have the authority to modify or reject rate changes proposed by insurers. But that changed as of the 2026 plan year (for rates filed in 2025), due to a new law that was enacted in 2023.24

And starting with the 2025 plan year, the Illinois Department of Insurance debuted a new summary page that contains an overview of the rate changes that insurers have filed, along with some of the filing details (final rates were added as open enrollment got underway).25 Although summary pages like this have long been displayed on many states’ insurance department websites, that was not the case in Illinois before 2024.

Illinois lawmakers also enacted legislation calling for a state-regulated load factor that is being added to all silver-level plans starting in 2026.26 This is also known as “premium alignment” and it has resulted in gold plans becoming relatively less expensive than silver plans, for people who aren’t eligible for cost-sharing reductions. Several other states, including Texas, Pennsylvania, Arkansas, Washington, and Vermont, have similar protocols.

For perspective, here’s how average individual/family health insurance premiums have changed in Illinois over the years:

- 2015: Average increases ranged from 2.6% to 11%.27

- 2016: Average increases ranged from 5.3% to 11.3%.28

- 2017: Overall average increase of 45.1%.29

- 2018: Overall average increase of 30%.30

- 2019: Average rate changes generally ranged from -4% to +6%.31

- 2020: Average rate decrease of 0.3%.32

- 2021: Relatively flat rates for most insurers33

- 2022: Average increase of roughly 5%.34

- 2023: Average increase of roughly 7%35

- 2024: Average increase of 5.7%36

- 2025: Average increase of 4.6%37

- 2026: Average increase of 30.1%3

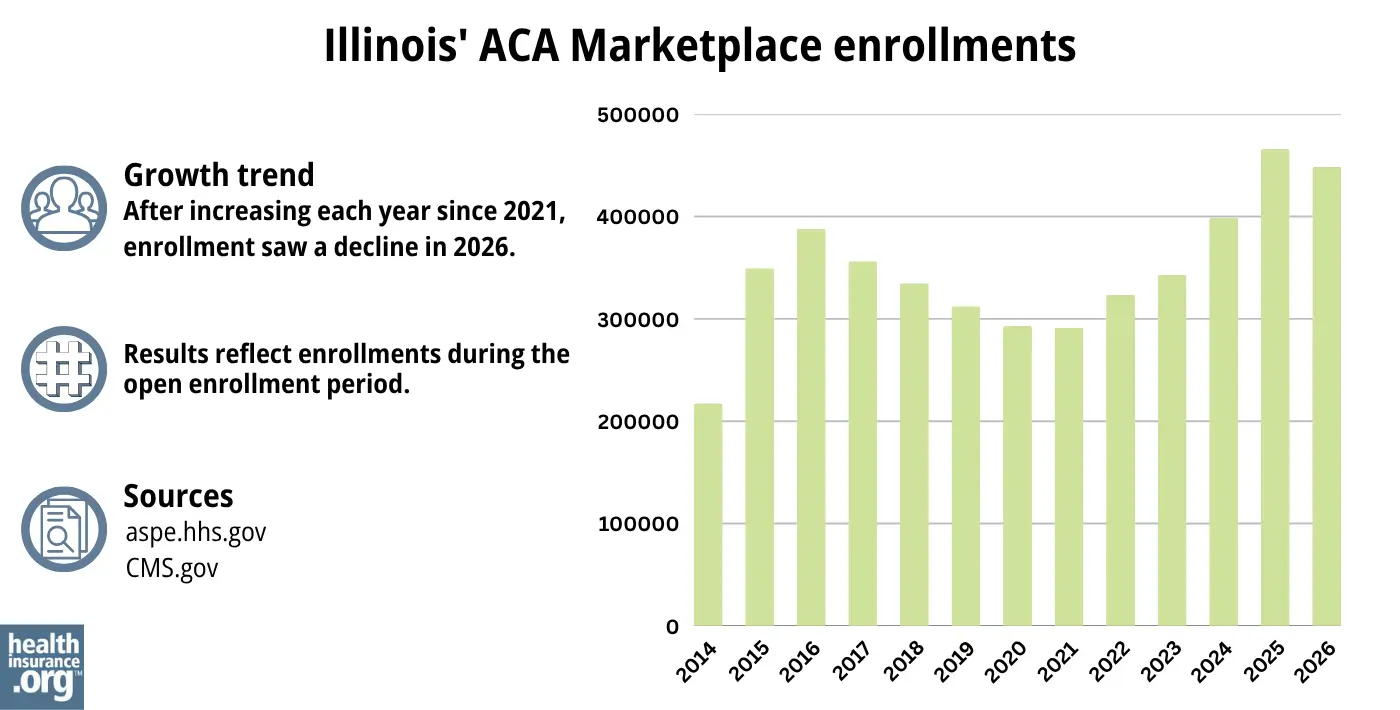

How many people are insured through Illinois’ Marketplace?

448,568 people signed up for private health coverage through the Illinois exchange during the open enrollment period for 2026 coverage.17

This was lower than the record high enrollment the year before, due in large part to the higher net premiums that enrollees faced as a result of the expiration of federal subsidy enhancements at the end of 2025.

Enrollment over time in the Illinois Marketplace is illustrated in the chart below. The increase in recent years prior to 2026 was due in large part to the subsidy enhancements provided by the American Rescue Plan and Inflation Reduction Act, but again, those expired at the end of 2025. The increase in 2024 and 2025 was also partially driven by the return to normal disenrollments for the Medicaid program, which was paused for three years during the pandemic. CMS reported that more than 105,000 Illinois residents transitioned from Medicaid to a Marketplace plan during the “unwinding” of the pandemic-era continuous coverage rule.38

Source: 2014,39 2015,40 2016,41 2017,42 2018,43 2019,44 2020,45 2021,46 2022,47 2023,48 2024,49 202550 202617

What health insurance resources are available to Illinois residents?

Get Covered Illinois

Premium tax credits are available only through the ACA Marketplace, which is now Get Covered Illinois.

Illinois Department of Insurance

The Illinois Department of Insurance regulates individual, small-group, and large-group health plans in the state (excluding self-insured ones). They also regulate brokers and agents selling private health insurance.

Illinois Senior Health Insurance Program (SHIP)

Contact them for assistance with Medicare questions.

Illinois Department of Healthcare and Family Services

Assistance with Medicaid eligibility or enrollment in Illinois and with All Kids, the state’s Children’s Health Insurance Program, and Family Care, the state’s Medicaid coverage for parents with minor children.

Looking for more information about other options in your state?

Need help navigating health insurance options in Illinois?

Explore more resources for options in IL including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”Gov. Pritzker Signs Legislation Authorizing a State-Based Marketplace for Health Insurance, Rate Review” Illinois.gov. June 27, 2023. And “Letter from CMS to Illinois” CMS.gov. Aug. 5, 2025 ⤶

- ”How do I claim my Get Covered Illinois account?” Get Covered Illinois. Accessed Oct. 8, 2025 ⤶

- ”Affordable Care Act (ACA) – Illinois Rate Filings” Illinois Department of Insurance. Accessed Oct. 19, 2025 ⤶ ⤶ ⤶ ⤶

- ”IDOI Announces Open Enrollment for the Get Covered Illinois Health Insurance Marketplace and Releases Rates for the 2025 Plan Year” Illinois Department of Insurance. Nov. 1, 2024 ⤶

- ”2026 Analysis of Illinois On-Exchange Plans” Illinois Department of Insurance. Accessed July 9, 2026 ⤶ ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Affordable Care Act (ACA) – Illinois Rate Filings” Illinois Department of Insurance. Accessed July 11, 2025 *The above is based on the most current data available. ⤶

- “Frequently Asked Questions” Get Covered Illinois. Accessed June 10, 2026 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Dec. 16, 2025 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Dec. 16, 2025 ⤶ ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- ”Limited-time marketplace transition year Special Enrollment Period” Get Covered Illinois. Accessed Feb. 6, 2026 ⤶

- ”Illinois SB3130” BillTrack50. Enacted Aug. 2, 2024. ⤶

- ”Life changes and special enrollment” Get Covered Illinois. Accessed Feb. 4, 2026 ⤶

- ”Illinois HB5142” BillTrack50. Enacted May 13, 2022 ⤶

- ”Free Local Help” Get Covered Illinois. Accessed Oct. 19, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov, Accessed June 10, 2026 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, Accessed July 11, 2025 ⤶

- ”Illinois HB2499” BillTrack50. Enacted July 10, 2024 ⤶

- ”Insurer Changes for 2026 Marketplace Coverage” Get Covered Illinois. Accessed Oct. 19, 2025 ⤶

- ”Affordable Care Act (ACA) – Illinois Rate Filings” Illinois Department of Insurance. Accessed June 10, 2026 ⤶ ⤶

- ”Affordable Care Act (ACA) – Illinois Rate Filings” (weighted average is based on enrollment totals pulled from the filings on that page: HCSC has 240,252 enrollees, Celtic has 16,493, Mercy Care has 2,070, Molina has 118, Oscar has 22,291, and United Healthcare has 59,068). Illinois Department of Insurance. Accessed June 10, 2026 ⤶

- ”Illinois House Bill 2296” BillTrack50. Enacted 2023 2023 ⤶

- ”Affordable Care Act (ACA) – Illinois Rate Filings” Illinois Department of Insurance. Accessed July 29, 2024 ⤶

- ”Illinois HB5395” BillTrack50. Passed May 24, 2024 ⤶

- ”Obamacare rates in Illinois: Higher premiums, more options in 2015” Venteicher, Wes, et al. Chicago Tribune. November 7, 2014 ⤶

- ”UnitedHealthcare of Illinois, Inc. History” Zippia.com ⤶

- ”Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC)” ACA Signups ⤶

- ”Illinois: RATE-HIKE-A-PALOOZA! Six More States Added At Once!” ACA Signups ⤶

- ”Illinois Department of Insurance releases ACA Exchange health care insurance rates for 2019” Illinois.gov. October 10, 2018. ⤶

- ”Illinois: *Final* Avg. 2020 #ACA Premiums: 0.3% Decrease” ACA Signups. October 30, 2019. ⤶

- ”Illinois: Preliminary Avg. 2021 #ACA Premiums: -1.8% Indy; +5.2% Sm. Group (Unweighted)” ACA Signups. October 15, 2020. ⤶

- ”*APPROVED* Avg. 2022 #ACA Rate Changeapalooza! AK, CA, GA, HI, IL, KS, LA, MA, MS, MO, NE, NH, TX, WY” ACA Signups. November 2, 2021. ⤶

- ”Illinois: Final Avg. Unsubsidized 2023 #ACA Rate Changes: +7.1% (Updated)” ACA Signups. August 5, 2022. ⤶

- So How’d I Do On My 2024 Avg. Rate Change Project? Not Bad At All! ACA Signups. December 2023. ⤶

- ”Illinois: Preliminary avg. unsubsidized 2025 #ACA rate changes: +4.6%” ACA Signups. July 16, 2024 ⤶

- ”HealthCare.gov Marketplace Medicaid Unwinding Report” Centers for Medicare & Medicaid Services. Data through April 2024; Accessed Dec. 29, 2024 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶