Find Oregon Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Oregon Marketplace quick facts

Oregon health insurance Marketplace guide

This guide, including the FAQs below, is designed to help you understand the health coverage options and possible financial assistance available to you and your family in Oregon. Many people find that an ACA Marketplace (exchange) plan, often called Obamacare, is a cost-effective choice.

Six private insurers offer health plans through the Oregon Marketplace for 2026 coverage4 (see below for details on insurer participation and rate changes for 2026). The average pre-subsidy rate increase in Oregon for 2026 was under 10%, as opposed to a nationwide average of more than 25%.5 But for most enrollees, net premium increases were much larger because Congress did not extend the subsidy enhancements that expired at the end of 2025.

Starting in July 2024, Oregon started operating a Basic Health Program, known as Oregon Health Plan (OHP) Bridge. Coverage under this program is available to adults under age 65 whose household income is between 138% and 200% of the federal poverty level.6

Oregon operates a state-based health insurance Marketplace but uses the HealthCare.gov enrollment platform (ie, an SBE-FP).7 That will change as of the fall of 2026, however, when Oregon will start running its own Marketplace platform, under the terms of legislation (SB972) the state enacted in 2023.8

(Oregon had a fully state-based exchange in 2014, but the website didn’t work well and the state opted to switch to an SBE-FP starting in the fall of 2014.9 The state plans to transition back to an SBE in the fall of 2026.)

For now, you can visit OregonHealthCare.gov to gather information about health insurance plans, eligibility, and more.10 When you’re ready to apply and enroll, you’ll be directed to HealthCare.gov to complete the enrollment (but starting in November 2026, this will no longer be the case, as Oregon will stop using the HealthCare.gov platform). Enrollment in OHP Bridge is done via one.Oregon.gov.

Frequently asked questions about health insurance in Oregon

Who can buy Marketplace health insurance in Oregon?

You can buy a health plan through the Oregon exchange if:11

- You reside in Oregon.

- You are a U.S. citizen or national.

- You are not incarcerated.

- You are not already enrolled in Medicare.

To qualify for financial assistance (premium subsidies and cost-sharing reductions), you must meet additional requirements:

- Your eligibility for premium subsidies depends on your income and how it compares with the cost of the second-lowest-cost Silver plan in your area. The cost of that Silver plan varies based on your age and location.

- You must not have access to affordable health coverage offered by an employer. If your employer offers health insurance, but you feel it’s too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies in the Marketplace.

- You must not be eligible for Medicaid or CHIP.

- You must not be eligible for premium-free Medicare Part A.12

- No one else can be able to claim you as a tax dependent.13

- If you’re married, you must file a joint tax return with your spouse.13 (with very limited exceptions)14

When can I enroll in an ACA-compliant plan in Oregon?

In Oregon, open enrollment for 2026 ACA Marketplace/exchange individual and family health coverage ended on January 15, 2026.

But starting in the fall of 2026, the open enrollment period will become shorter. In states that use HealthCare.gov, the enrollment window will end December 15. States that run their own enrollment platforms (which will include Oregon by that point)15 will have the option to extend the enrollment window, but not past December 31.

OHP Bridge enrollment and Medicaid enrollment are both open year-round.

Enrolling in an exchange plan or changing your coverage outside of the open enrollment period is possible if you meet the criteria for a Special Enrollment Period (SEP).16 This typically means you must have a qualifying life event, such as losing your health insurance, getting married, or having a baby. But Native Americans can enroll or switch plans year-round (the SEP for Native Americans is available nationwide, regardless of whether a state uses HealthCare.gov or runs its own exchange platform).

How do I enroll in a Marketplace plan in Oregon?

Here are the main ways to enroll in a Marketplace health plan in Oregon:

- Online: You can visit OregonHealthCare.gov to learn more about health insurance plans and eligibility.17 When it’s time to apply and enroll, you’ll be redirected to the federal Marketplace website, HealthCare.gov.

(Oregon’s new state-based Marketplace platform will debut in the fall of 2026. To enroll in coverage for 2027 and future years, Oregon residents will no longer use HealthCare.gov.)18 - By Phone: Dial 1-800-318-2596 (TTY: 1-855-889-4325) to enroll with a Marketplace representative. The call center is available 24 hours a day, seven days a week, but it’s closed on holidays.

- In-person: Enrollment assistance is also available from trained Navigators and assisters who can answer your questions. Go to localhelp.HealthCare.gov or OregonHealthCare.gov/GetHelp to find local help in your area.19

Assistance is available from local Navigators and brokers. Enrollments can also be completed via an approved enhanced direct enrollment (EDE) entity, using the EDE’s website.20

How can I find affordable health insurance in Oregon?

Oregon’s ACA Marketplace (HealthCare.gov) is a one-stop shop where individuals and families can find affordable health insurance coverage in Oregon. There are two types of financial assistance available through the Marketplace:

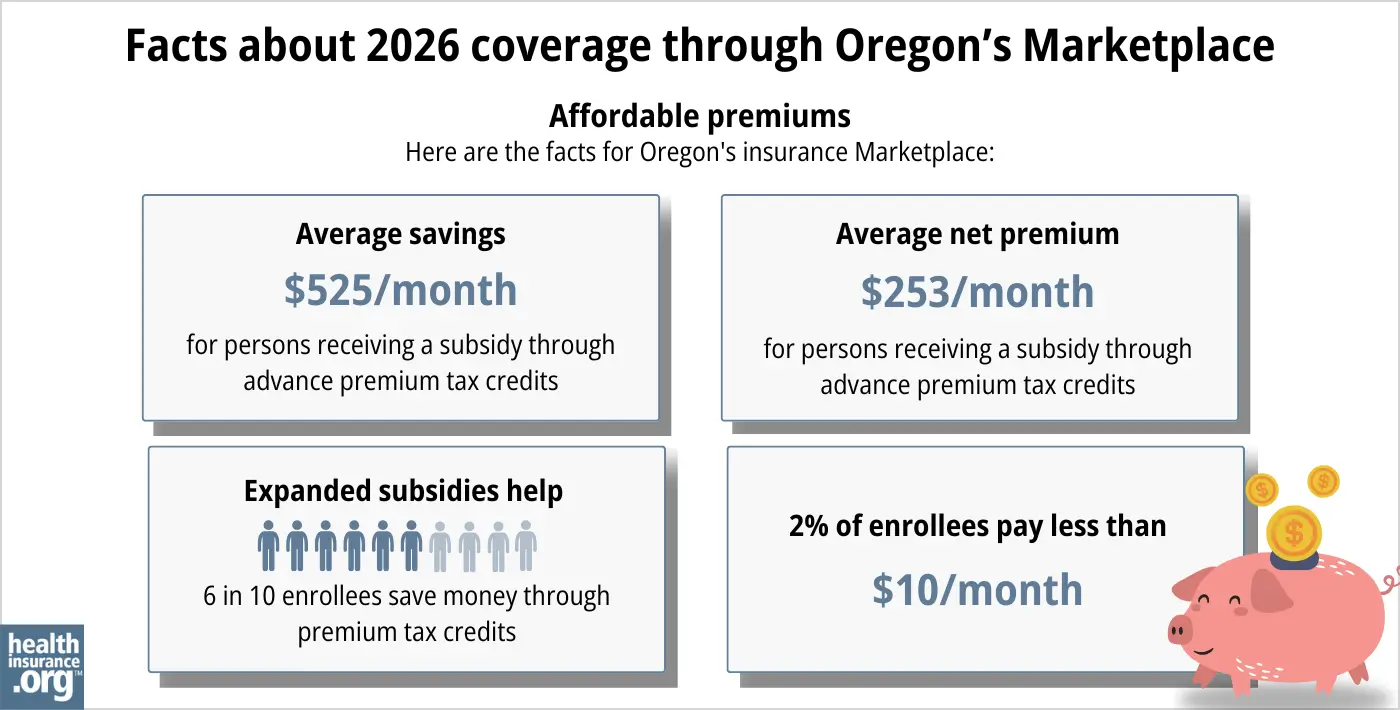

- Premium subsidies: You may qualify for income-based subsidies known as Advance Premium Tax Credits (APTC) that help lower your monthly premiums through the ACA Marketplace. About six out of 10 Oregon exchange enrollees qualified for premium subsidies in 2026, saving an average of $525 monthly. People who receive these subsidies pay an average monthly premium of $253 in 2026.1

Source: CMS.gov1

- Cost-sharing reductions: To be eligible for cost-sharing reductions (CSR), your income must be no more than 250% of the federal poverty level,21 and you must enroll in a Silver-level plan through the Oregon Marketplace. CSRs help lower your out-of-pocket costs, making coverage more affordable.22

Oregon implemented a reinsurance program starting in 2018, using a 1332 waiver that allows the state to capture federal savings generated by the program.23 Reinsurance is designed to keep unsubsidized (full-price) premiums lower than they would otherwise be. Although most enrollees do qualify for premium subsidies, the reinsurance program helps to minimize premiums for those who don’t.

Oregon also requires all state-regulated health plans, including Marketplace plans, to cover both female and male contraception (including vasectomies), as well as abortion, all without out-of-pocket costs.24 (There is an exception for HSA-qualified high-deductible health plans, to ensure those plans don’t lose their HSA eligibility.)

Medicaid: Oregon residents may qualify for Medicaid coverage if eligible based on income. Medicaid in Oregon is called Oregon Health Plan, and has no monthly premiums.25

Basic Health Program: Oregon has created a Basic Health Program — OHP Bridge —that became operational in July 2024.6 Federal approval for OHP Bridge was granted in June 2024.26

Coverage under OHP Bridge is available to Oregon adults (under age 65) with income above 138% of the poverty level but not above 200% of the poverty level.27 (Children at this income level were already eligible for OHP coverage, so OHP Bridge does not need to cover children.)

Short-term health insurance: If you’re not eligible for subsidies, Medicare, or Medicaid, short-term health insurance, available in Oregon with terms of up to three months, might be an affordable temporary solution. But note that these plans do not include ACA consumer protections, so they typically don’t cover pre-existing conditions and don’t include all of the essential health benefits.

How many insurers offer Marketplace coverage in Oregon?

Six insurers offer plans through Oregon’s exchange for 2026:4

- BridgeSpan Health Company

- Kaiser Foundation Healthplan of the NW

- Moda Health Plan, Inc.

- PacificSource Health Plans

- Providence Health Plan

- Regence BlueCross BlueShield of Oregon

All six carriers also offered coverage in 2025. Five carriers are continuing to offer plans statewide in 2026 (as they did in 2025), and Kaiser is offering plans in 11 counties for 2026.28

Are Marketplace health insurance premiums increasing in Oregon?

The following average rate changes were approved for 2026 for Oregon’s individual/family market health insurers, amounting to an overall average rate increase of 9.7%, before subsidies are applied.4 (This was a significantly smaller average rate increase than the national average for 2026.)29

Oregon’s ACA Marketplace Plan 2026 APPROVED Average Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| BridgeSpan Health Company | 12.6% |

| Kaiser Foundation Healthplan of the NW | 12.9% |

| Moda Health Plan, Inc. | 9.2% |

| PacificSource Health Plans | 3.9% |

| Providence Health Plan | 8.1% |

| Regence BlueCross BlueShield of Oregon | 12.4% |

Source: Oregon Department of Consumer and Business Services4

The average rate changes apply to full-price premiums. However, most Oregonians who enrolled in ACA plans were receiving subsidies in 2025 – which means they did not pay the full rate.30

Subsidy amounts are adjusted each year based on the cost of the second-lowest-priced Silver plan. But for 2026, subsidies cover a smaller portion of enrollees’ premiums than they did in 2025, because Congress allowed premium subsidy enhancements to expire at the end of 2025.

Because the subsidy enhancements expired:

- Only 60% of Oregon Marketplace enrollees qualified for subsidies for 2026,31

down from 80% in 2025.32 Subsidies are no longer available to anyone with a household income above 400% of the federal poverty level. - Average after-subsidy premiums grew to $426/month in 2026, up from $272/month in 2025.33

- Marketplace enrollment dropped by more than 15% from 2025 to 2026.33

- More people selected Bronze plans, which have lower premiums but higher out-of-pocket costs.

For perspective, here’s a summary of how average full-price (unsubsidized) premiums have changed in Oregon’s individual market over the years:

- 2015: Average decrease of 5%.34

- 2016: Average increase of 24.2%.35

- 2017: Average increase of 26.5%.36

- 2018: Average increase of 15.7%.37 (reinsurance took effect;38 Federal CSR funding eliminated39)

- 2019: Average increase of 7.3%40

- 2020: Average increase of 1.5%.41

- 2021: Average increase of 2.1%.42

- 2022: Average increase of 1.5%.43

- 2023: Average increase of 6.7%.44

- 2024: Average increase of 6.2%.45

- 2025: Average increase of 8.3%.46

How many people are insured through Oregon’s Marketplace?

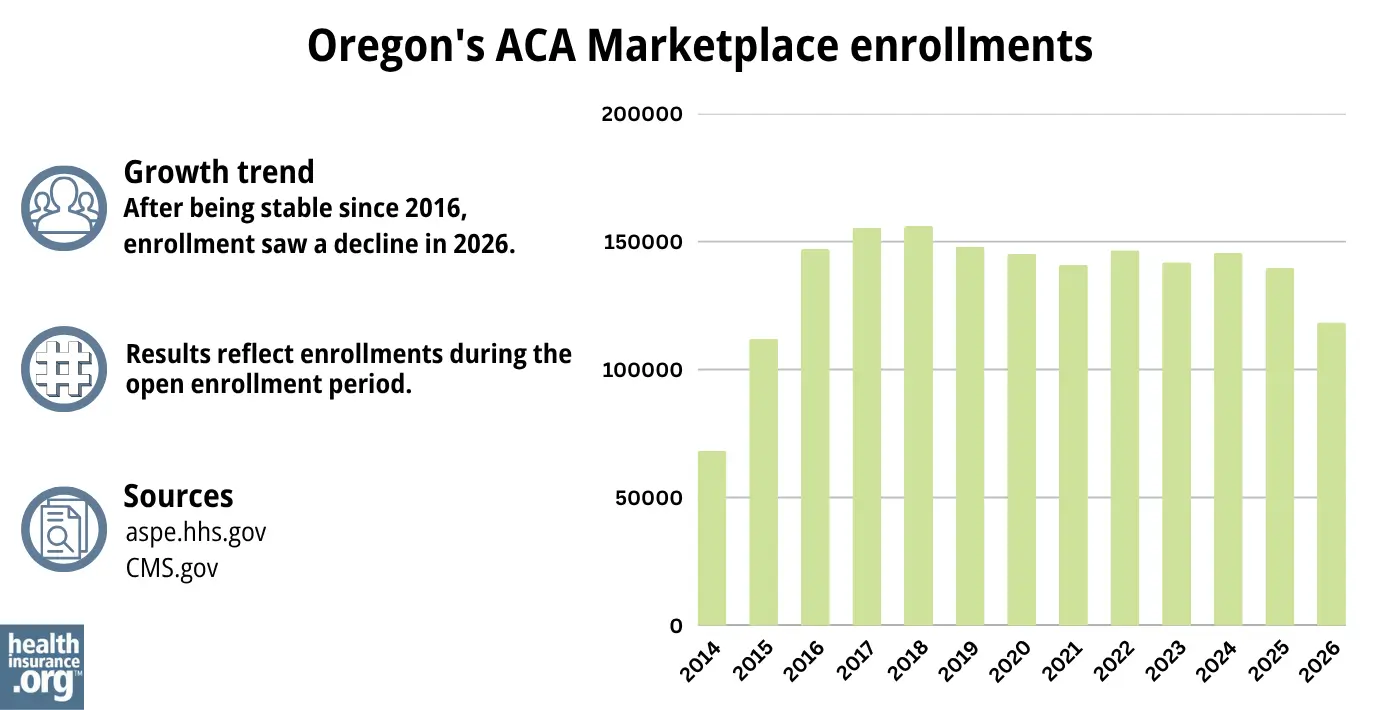

During the 2026 open enrollment period, 118,372 people signed up for individual/family health coverage through the Oregon Marketplace/exchange.1

Source: 2014,47 2015,48 2016,49 2017,50 2018,51 2019,52 2020,53 2021,54 2022,55 2023,56 2024,57 202558 20261

As was the case in most states, Oregon’s 2026 enrollment was a decrease from 2025, due to the expiration of federal subsidy enhancements.

Although nationwide Marketplace enrollment had grown to significant record highs in recent years (prior to 2026), Oregon’s enrollment had hovered around the same level for many years before declining in 2026.

For 2024 and 2025, when nationwide Marketplace enrollment grew significantly, Oregon’s did not. But that’s likely because Oregon allowed people to remain on Medicaid with income up to 200% of the poverty level during the post-pandemic “unwinding” process, and then those individuals were able to transition to the new BHP (Oregon Health Plan Bridge) starting in mid-2024, rather than a private Marketplace plan.

What health insurance resources are available to Oregon residents?

OregonHealthCare.gov

A state-run service that connects Oregon residents with health coverage options.

HealthCare.gov

The Marketplace for individuals and families buying their own health coverage; premium subsidies and cost-sharing reductions are available for eligible enrollees who use the Marketplace. (Oregon will no longer use HealthCare.gov starting November 1, 2026.)

Oregon Division of Financial Regulation

Licenses and regulates health insurance companies in Oregon, as well as agents and brokers. Can address consumer questions and complaints about regulated entities.

Medicare Rights Center

A nationwide resource that can answer questions about Medicare and provide information that beneficiaries need.

Oregon Senior Health Insurance Benefits Assistance

A local service that can provide assistance, information, and enrollment counseling to Medicare beneficiaries and their caregivers.

Looking for more information about other options in your state?

Need help navigating health insurance options in Oregon?

Explore more resources for options in OR including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶ ⤶

- ”Oregonians continue to have at least five health insurance companies to choose from in every Oregon county as companies file 2026 health insurance rate requests for individual and small group markets” Oregon Department of Consumer and Business Services. June 2, 2025 *The above is based on the most current data available. ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” and “Marketplace 2025 Open Enrollment Period Report: National Snapshot” Centers for Medicare & Medicaid Services, April 2026 ⤶

- ”ACA-Compliant Plans 2026 Health Insurance Rate Requests” Oregon Division of Financial Regulation. Accessed Dec. 7, 2025 ⤶ ⤶ ⤶ ⤶

- ”2026 Rate Change Project” ACA Signups. Nov. 2, 2025 ⤶

- ”Oregon Health Plan (OHP) Bridge” and ”Oregon Health Plan (OHP) Bridge — Frequently Asked Questions” Oregon Health Authority. Accessed Dec. 7, 2025 ⤶ ⤶

- ”State-based Exchanges” Centers for Medicare & Medicaid Services. Accessed Dec. 7, 2025 ⤶

- Oregon Senate Bill 972. BillTrack50. Enacted August 2023. ⤶

- Oregon decides to ditch its online health exchange for federal site. PBS News Hour. April 2014. ⤶

- “Explore your coverage and savings options” OregonHealthCare.gov, Accessed Apr. 21, 2026 ⤶

- “Are you eligible to use the Marketplace?” HealthCare.gov, Accessed Apr. 21, 2026 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Dec. 7, 2025 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Dec. 7, 2025 ⤶ ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- ”State-based Marketplace Project” Oregon.gov. Accessed Apr. 21, 2026 ⤶

- “Special enrollment opportunities” HealthCare.gov. Accessed Dec. 7, 2025 ⤶

- “Explore your coverage and savings options” OregonHealthCare.gov, Accessed Apr. 21, 2026 ⤶

- ”State-based Marketplace Project” Oregon.gov. Accessed Dec. 7, 2025 ⤶

- “Find Local Help” OregonHealthCare.gov, Accessed Apr. 21, 2026 ⤶

- “Entities Approved to Use Enhanced Direct Enrollment” CMS.gov, Apr. 7, 2026 ⤶

- “Federal Poverty Level (FPL)” HealthCare.gov, 2023 ⤶

- APTC and CSR Basics. Centers for Medicare and Medicaid Services. Oct. 2025 ⤶

- Section 1332: State Innovation Waivers-Oregon. Centers for Medicare and Medicaid Services. Accessed Apr. 21, 2026 ⤶

- Reproductive Health Equity Act FAQs. Planned Parenthood. Accessed Dec. 7, 2025 ⤶

- Oregon Health Plan. Oregon Health Authority. Accessed Dec. 7, 2025 ⤶

- ”Approval letter for Oregon’s Basic Health Program (BHP) Blueprint” U.S. Department of Health & Human Services. June 7, 2024 ⤶

- ”Oregon Health Plan (OHP) Bridge — Frequently Asked Questions” Oregon Health Authority. May 3, 2024 ⤶

- ”Oregonians continue to have at least five health insurance companies to choose from in every Oregon county as companies file 2026 health insurance rate requests for individual and small group markets” Oregon Department of Consumer and Business Services. June 2, 2025 ⤶

- ”How Much and Why ACA Marketplace Premiums Are Going Up in 2026” KFF.org. Aug. 6, 2025 ⤶

- ”Effectuated Enrollment: Early 2025 Snapshot and Full Year 2024 Average” CMS.gov, July 24, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” Centers for Medicare & Medicaid Services. Mar. 27, 2026 ⤶

- ”2025 Marketplace Open Enrollment Period Public Use Files” Centers for Medicare & Medicaid Services. May 11, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” And “2025 Marketplace Open Enrollment Period Public Use Files” Centers for Medicare & Medicaid Services. Accessed Apr. 21, 2026 ⤶ ⤶

- Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums. The Commonwealth Fund. December 2014. ⤶

- Oregon: Final 2016 Rate Hikes Approved…24.2% Weighted Average Increase, But… ACA Signups. July 2015. ⤶

- Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC). ACA Signups. October 2016. ⤶

- 2018 Rate Hikes. ACA Signups. October 2017. ⤶

- Section 1332: State Innovation Waivers-Oregon. Centers for Medicare and Medicaid Services. Accessed November 2023. ⤶

- State announcement regarding Trump administration discontinuation of cost-sharing reduction payments. Oregon.gov. October 2017. ⤶

- 2019 Rate Hikes. ACA Signups. October 2018. ⤶

- Final health insurance rate decisions lower 2020 premiums by $44 million. Oregon.gov. July 2019. ⤶

- Oregon: Final Avg. 2021 ACA Rate Change: +2.1%; +3.7% For Sm. Group. ACA Signups. October 2020. ⤶

- ”Oregon Health Insurance Marketplace Report – CY 2024 Administrative Charges Health Insurance Marketplace Advisory Committee Material” OBIZ Otpumas. Mar. 7, 2023 ⤶

- ”Oregonians get early glimpse of 2023 health insurance rates” Oregon Department of Financial Regulation. May 23, 2022 ⤶

- Oregon finalizes 2024 health rates for individual, small group markets; sees robust options in all counties. Oregon.gov, September 2023. ⤶

- ”Oregon Division of Financial Regulation issues final health rates for 2025; five insurance companies now statewide in individual market” Oregon Division of Financial Regulation. Sep. 5, 2024 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶