Medicare in Arkansas

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Arkansas

Medicare enrollment in Arkansas

As of early 2026, there were 689,868 Arkansas residents enrolled in Medicare.1 Medicare enrollment happens for most Americans when they turn 65 – either automatically, if they’re already receiving Social Security or Railroad Retirement benefits, or during a seven-month enrollment window when they can complete the process of filing for Medicare benefits.

But Medicare eligibility is also triggered for younger people if they’re disabled and have been receiving disability benefits for 24 months, or if they have amyotrophic lateral sclerosis amyotrophic lateral sclerosis (ALS) or end-stage renal disease (ESRD).

Nationwide, more than 90% of Medicare beneficiaries are eligible due to their age, while about 9% are eligible due to a disability.2 In Arkansas, about 15% of the people with Medicare are eligible due to disability rather than age.3

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how the Arkansas Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

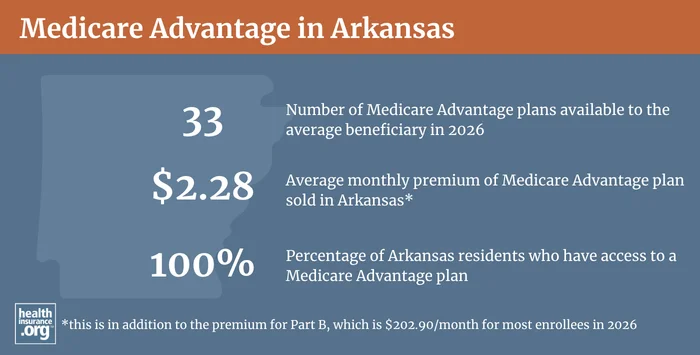

Medicare Advantage plan availability and enrollment in Arkansas

Private Medicare Advantage plans are an alternative to Original Medicare, and are available in all counties in Arkansas for 2026 coverage,4 although the service areas vary by plan, with availability varying across the state.5

About 47% of Arkansas Medicare beneficiaries had Medicare Advantage coverage as of January 20263 versus a nationwide average of almost 51%.6 As of January 2026, there were 323,764 Arkansas residents with private Medicare Advantage coverage, while the other 366,104 beneficiaries had coverage under Original Medicare.7

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Arkansas by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in Arkansas

As of the end of 2023, 178,052 people had Medigap coverage in Arkansas.8

Learn more about Medigap plans, including what they cover and how they’re standardized under federal rules.

Arkansas is one of just nine states9 where Medigap premiums cannot vary based on an enrollee’s age,10 as long as the enrollee is at least 65 years old (more on this below). Medigap premiums in Arkansas can still vary based on tobacco use and medical history, with preferred premiums and standard premiums for various scenarios.

There are 24 insurance companies that offer Medigap plans in Arkansas.11 Medigap insurers in the state are required to maintain minimum loss ratios of at least 65% for individual policies, and at least 75% for employer group policies. This means that at least 65% (or 75% for group plans) of the premium revenue that the insurers bring in must be spent on enrollees’ healthcare claims.

People who aren’t yet 65 can enroll in Medicare if they’re disabled and have been receiving disability benefits for at least two years or if they have amyotrophic lateral sclerosis (ALS) or kidney failure, and about 15% of Arkansas Medicare beneficiaries are under age 65.12 Federal rules do not guarantee access to Medigap plans for people who are under 65, but the majority of the states have implemented rules to ensure that disabled Medicare beneficiaries have at least some access to Medigap plans.

Arkansas joined them in 2018, with a law that was enacted in 2017 (Act 684). The law called for the Arkansas Insurance Department to amend the state’s rules so that people under age 65 would be able to purchase Medigap coverage by 2018. (Prior to that, Medigap insurers in Arkansas did not have to sell plans to people under the age of 65.)

Since July 2018, Medigap insurers must offer at least one Medigap plan to Medicare beneficiaries under the age of 65.13 Insurers can pick which plan they want to offer to disabled enrollees, and nearly all of them have chosen Plan A (the least comprehensive Medigap plan), although Arkansas Blue Cross Blue Shield also offers other options.14

There is no requirement that Arkansas Medigap insurers extend the “no age rating” rule to people under the age of 65, and most of the insurers charge significantly higher premiums for disabled enrollees.14

Disabled Medicare beneficiaries have another Medigap open enrollment period when they turn 65. At that point, they can pick from any available plan, and with the lower premiums that apply to people who are age 65.

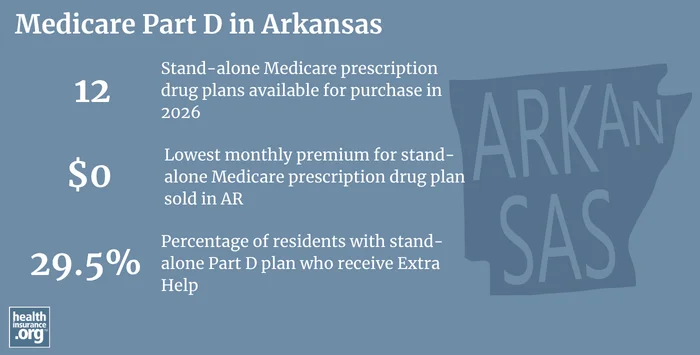

Medicare Part D plan availability and enrollment in Arkansas

For 2026, there are 12 stand-alone Medicare Part D plan options for sale in Arkansas,4 with premiums that start as low as $0/month.4

As of January 2026, 250,500 Medicare beneficiaries in Arkansas had prescription coverage under stand-alone Medicare Part D plans.15 Another 301,435 had Part D prescription coverage integrated with their Medicare Advantage plans.15

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Arkansas

- If you have questions about Medicare eligibility in Arkansas, Medicare enrollment in Arkansas, or need general information about health coverage for seniors, you can contact the Arkansas Senior Health Insurance Information Program (SHIIP). This state-based resource is designed to provide assistance on a wide range of Medicare-related questions.

- Arkansas SHIIP Quick Guide to Medicare

- The Arkansas Insurance Department’s Senior Health Page includes a variety of resources and information that are useful for people with Medicare in Arkansas.

- The Medicare Rights Center is a nationwide service that can provide assistance and information regarding Medicare enrollment, eligibility, and benefits.

Looking for more information about other options in your state?

Need help navigating health insurance options in Arkansas?

Explore more resources for options in AR including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment, January 2026” Centers for Medicare & Medicaid Services Data. Accessed April 2026 ⤶

- “Medicare Monthly Enrollment, January 2026” Centers for Medicare & Medicaid Services. Accessed April 2026. ⤶

- “Medicare Monthly Enrollment, January 2026” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶ ⤶

- “Fact Sheet: Medicare Open Enrollment, 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶ ⤶ ⤶

- “Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings” KFF.org. Dec. 9, 2025 ⤶

- “Medicare Monthly Enrollment, January 2026” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶

- “Medicare Monthly Enrollment” Centers for Medicare & Medicaid Services Data. Accessed Apr. 2026. ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Key Facts About Medigap Enrollment and Premiums for Medicare Beneficiaries” KFF.org. Oct. 18, 2024 ⤶

- “Act 710 of the 1989 Regular Session” (Section 2(5)) Arkansas Legislature. Accessed Jan. 29, 2026 ⤶

- “Supplement Insurance (Medigap) Plan A policies” Medicare.gov. Accessed Apr. 23, 2026 ⤶

- “Medicare Monthly Enrollment – January 2026, Arkansas” Centers for Medicare & Medicaid Services Data. Accessed Apr. 23, 2026. ⤶

- “054.00.17 Ark. Code R. 003 – Proposed Rule 27: Minimum Standards for Medicare Supplement Policies” (Section 25). Cornell Legal Information Institute. Accessed Jan. 29, 2026 ⤶

- “Supplement Insurance (Medigap) plans in Arkansas” (zip code 72002) Medicare plan comparison tool. Accessed Apr. 23, 2026 ⤶ ⤶

- “Medicare Monthly Enrollment, January 2026, Arkansas” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶ ⤶