Medicare in Maine

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Maine

Key takeaways

- 378,117 residents were enrolled in Medicare in Maine.1

- Medicare Advantage enrollment in Maine has grown sharply, reaching nearly 58% of the state’s beneficiaries.1

- Only 34% of beneficiaries of Medicare in Maine have stand-alone Part D prescription coverage.1

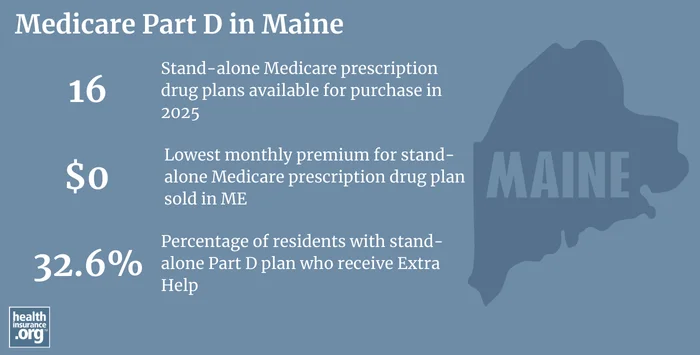

- 16 stand-alone Medicare Part D plans available in Maine for 2025, with premiums starting at $0 per month.2

Medicare enrollment in Maine

378,117 residents were enrolled in Medicare in Maine as of August 2024.1 That’s 23% of the state’s total population, compared with about 17% of the United States population with Medicare coverage.3

Maine’s substantial Medicare enrollment is not surprising, given that it has the highest percentage of residents age 65+ in the country. Medicare eligibility is also triggered for younger people who are disabled for at least two years, or diagnosed with ALS or end-stage renal disease. Nationwide, about 11% of Medicare beneficiaries are under the age of 65,4 but this is also higher in Maine, where 13% of Medicare beneficiaries were under 65 as of mid-2024.1

Medicare options

Medicare beneficiaries can choose from among several options to access Medicare coverage. The first choice is between Medicare Advantage plans, where coverage is through private Medicare Advantage plans, or Original Medicare, where coverage is provided directly by the federal government. Medicare beneficiaries also have options around Medigap policies and Medicare Part D (prescription drug) coverage, both of which are purchased separately by Original Medicare beneficiaries.

Original Medicare includes Part A (also called hospital insurance, which helps pay for inpatient stays) and Part B (also called medical insurance, which helps pay for outpatient care and preventive healthcare services). Medicare Advantage plans bundle Parts A and B under a single monthly premium and often include other services like Part D prescription drug coverage and dental/vision coverage. There are pros and cons to either option, and the “right” solution is different for each individual.

Learn about Medicare plan options in Maine by contacting a licensed agent.

Explore our other comprehensive guides to coverage in Maine

The ACA Marketplace allows individuals and families to shop for and enroll in ACA-compliant health insurance plans. Subsidies may be available based on household income to help lower costs.

Hoping to improve your smile? Dental insurance may be a smart addition to your health coverage. Our guide explores dental coverage options in Maine.

Learn about Maine’s Medicaid expansion, the state’s Medicaid enrollment and Medicaid eligibility.

Short-term health plans provide temporary health insurance for consumers who may find themselves without comprehensive coverage. Learn more about short-term plan availability in Maine.

Frequently asked questions about Medicare in Maine

What is Medicare Advantage?

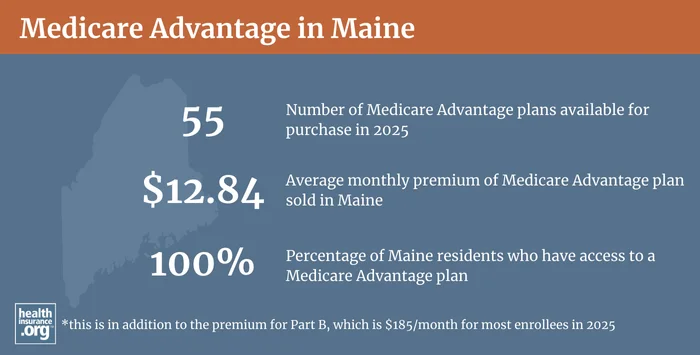

30% of Medicare beneficiaries in Maine were enrolled in private Medicare Advantage plans in 2018, but that had grown to nearly 58% as of August 2024.1 The remaining 42% of Maine’s Medicare beneficiaries had opted instead for coverage under Original Medicare.1 Nationwide, about 50% of all Medicare beneficiaries were enrolled in private Medicare Advantage plans as of mid-2024.4

The availability of Medicare Advantage plans varies from one county to another. Across Maine’s 16 counties, Medicare Advantage availability in 2024 ranges from 1 plans to 53 plans.5

Medicare beneficiaries can switch from Medicare Advantage enrollment to Original Medicare or vice versa, each year during the annual election period in the fall (October 15 through December 7). There is also a Medicare Advantage open enrollment period (January 1 to March 31) during which people who are already enrolled in Medicare Advantage plans can switch to a different Medicare Advantage plan or drop their Medicare Advantage plan and enroll in Original Medicare instead.

What are Medigap plans?

Medigap plans are used to supplement Original Medicare, covering some or all of the out-of-pocket costs (for coinsurance and deductibles) that people would otherwise incur if they only had Original Medicare on its own.

Medigap plans are standardized under federal rules — plans are designated by letter, from A through N; all Medigap insurers must offer at least Plan A and also offer at least Plan C or Plan F in addition to Plan A (note that under federal rules, Plan C and Plan F cannot be sold to people who weren’t already eligible for Medicare in 2019 or earlier).

People are granted a six-month window, when they turn 65 and enroll in Original Medicare, during which coverage is guaranteed issue for Medigap plans. Federal rules do not, however, guarantee access to a Medigap plan if you’re under 65 and eligible for Medicare as a result of a disability. And after the initial six-month open enrollment period ends, federal rules do not allow enrollees guaranteed-issue access to Medigap plans (including switching from one plan to another) unless they experience one of the limited situations that trigger a guaranteed-issue right.

But Maine has much more extensive Medigap regulations, designed to protect consumers and ensure greater access to Medigap. Maine’s rules are explained in the state’s Consumer Guide to Medicare Supplement Plans, and include several provisions:

- All Medigap insurers in Maine must designate at least one month per year when all applicants will be accepted for enrollment in Medigap Plan A, regardless of their medical history (Plan A offers the least amount of benefits). Insurers can be more lenient than this basic requirement and two insurers (Anthem Blue Cross Blue Shield, and Colonial Penn) offer year-round access to Medigap Plan A. The rest of the insurers have varying one-month windows when Plan A is available on a guaranteed-issue basis.6

- People under age 65 in Maine are granted the same six-month open enrollment period for guaranteed-issue Medigap plans (starting when they’re enrolled in Medicare Part B) as people who are 65 and enrolling in Medicare due to their age. These enrollees also have access to another six-month open enrollment period — during which they can switch to any Medigap plan on a guaranteed-issue basis — when they turn 65. Maine Rule 275, Section 11 clarifies that insurers cannot condition eligibility or premiums on a person’s medical history as long as they enroll during their six-month open enrollment window, or in the 60 days preceding it (to ensure that people can have a seamless transition to Medicare, with Medigap coverage effective the same day Medicare begins).7

- After the initial six-month window ends, Medigap enrollees in Maine are allowed to switch to a different plan from their current insurer or a different insurer, as long as they pick a plan with equal or lesser benefits (this chart on page 5 shows which plans are available, depending on the plan the person already has) and as long as they haven’t had a break of more than 90 days in their Medigap coverage since their initial open enrollment period.

- Medigap insurers in Maine must allow a Medicare beneficiary to enroll in a Medigap plan if they apply within 90 days of losing coverage under an individual market plan (not counting a short-term health plan or fixed indemnity plan), an employer-sponsored plan, or MaineCare (Medicaid).

- Maine is one of eight states where Medigap premiums cannot vary based on age, and that provision also includes people under age 65 (some of the states that ban age-based Medigap premiums only apply that requirement to plans sold to people who are at least 65 years old). Medigap premiums in Maine only vary based on tobacco use.8

- Federal law gives people a “trial right” to try Medicare Advantage and then switch to Original Medicare instead, with guaranteed-issue access to Medigap as long as the person makes the switch to Original Medicare within a year. But Maine law extends that trial right period to three years. If a person in Maine signs up for Medicare Advantage when they’re first eligible for Medicare and then switches to Original Medicare within three years, they have a guaranteed-issue right to buy any Medigap plan available in their area, as long as they purchase it within 90 days of their Medicare Advantage plan ending.

- Maine residents who have Medigap coverage and terminate it to switch to Medicare Advantage also have a three-year trial period, although it’s a little more restrictive. As long as they switch back to Original Medicare within three years and apply for a Medigap plan within 90 days of the Medicare Advantage plan ending, they have a guaranteed issue right to buy a Medigap plan with benefits that are equal to or less than their original Medigap plan’s benefits (again, this chart on page 5 shows which plans have equal or lesser benefits).

17 insurers in Maine offer Medigap plans as of 2025.6 Insurers cannot exclude pre-existing conditions if the applicant had a least six months of creditable coverage prior to enrolling in Medigap (if they had creditable coverage but for a period of less than six months, the insurer can implement a pre-existing condition waiting period of up to six months minus the amount of time the person had creditable coverage in the prior six months).

What is Medicare Part D?

Original Medicare does not cover outpatient prescription drugs. But Medicare beneficiaries can get prescription coverage via a Medicare Advantage plan, an employer-sponsored plan (offered by a current or former employer), or a stand-alone Medicare Part D plan.

As of August 2024, there were 309,616 Medicare beneficiaries in Maine enrolled in Part D coverage.1 The majority of them — more than 205,000 — had Part D coverage integrated with Medicare Advantage plans.1 And there were also more than 103,000 who had stand-alone Part D plans.1

For 2025 coverage, there are 16 stand-alone Medicare Part D plans available in Maine, with premiums starting at $0 per month.2

Medicare Part D enrollment is available when a person is first eligible for Medicare, and there’s also an annual open enrollment period (October 15 – December 7) when beneficiaries can enroll in Part D coverage or switch to a different plan for the coming year.

What additional resources are available for Medicare beneficiaries and their caregivers in Maine?

Need help with your Medicare application in Maine, or have questions about Medicare eligibility in Maine? These resources provide free assistance and information.

- You can contact the Maine State Health Insurance Assistance Program.

- The website for the Maine Bureau of Insurance includes a page of frequently asked Medicare questions.

- Visit the Medicare Rights Center. This website provides helpful information geared to Medicare beneficiaries, caregivers, and professionals.

Looking for more information about other options in your state?

Need help navigating health insurance options in Maine?

Explore more resources for options in ME including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Maine.” Centers for Medicare & Medicaid Services Data. Accessed December, 2024. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- ”Fact Sheet: Medicare Open Enrollment for 2025” (59) Centers for Medicare & Medicaid Services. Sep. 27, 2024 ⤶ ⤶

- U.S. Census Bureau Quick Facts: United States & Maine.” U.S. Census Bureau, July 2023. ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data, December 2024. ⤶ ⤶

- ”Medicare Advantage 2024 Spotlight: First Look” KFF.org Nov. 15, 2023 ⤶

- “A Consumer’s Guide to Medicare Supplement Insurance” Maine Bureau of Insurance. May 2025. ⤶ ⤶

- ”Medicare FAQs” (first question includes a link that will allow a download of Rule 275) Maine Bureau of Insurance. Accessed Apr. 16, 2025 ⤶

- ”Medicare Supplement Annual Rates” Maine Bureau of Insurance. Accessed July 1, 2025 ⤶