Medicare in Massachusetts

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Massachusetts

In this article

Medicare enrollment in Massachusetts

As of January 2026, 1,500,684 people had Medicare in Massachusetts.1

In most cases, transitioning to Medicare goes along with turning 65. But Medicare enrollment is also available to younger individuals after they have been receiving disability benefits for 24 months, or if they have amyotrophic lateral sclerosis (ALS) or end-stage renal disease (ESRD).

About 10% of Medicare beneficiaries in Massachusetts are under the age of 65,1 which is similar to the nationwide percentage.2

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how the Massachusetts Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

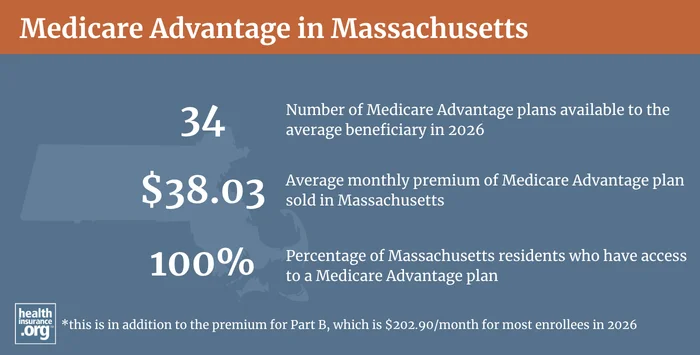

Medicare Advantage plan availability and enrollment in Massachusetts

Medicare Advantage plans are offered by private insurers, whose service areas vary from county to county. All of Massachusetts has an active Medicare Advantage market, with numerous plans available for 2026 – 103 in total.3

But plan availability varies from one area to another. The average Medicare beneficiary in Massachusetts can select from among 34 Medicare Advantage plans in 2026.4 As of January 2026, about 36% of Massachusetts Medicare beneficiaries had Medicare Advantage coverage.5 But Original Medicare continues to be more popular in Massachusetts than it is nationwide, with about 64% of Massachusetts Medicare beneficiaries enrolled in Original Medicare.1

Learn more about Medicare Advantage and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Massachusetts by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in Massachusetts

According to an AHIP (formerly called America’s Health Insurance Plans) analysis, there were 343,996 Massachusetts Medicare beneficiaries enrolled in Medigap coverage as of 2023.6

Eight insurers offer Medigap plans in Massachusetts for 2026.7

In all but three states, Medigap plans are standardized under federal rules. But Massachusetts is one of the three states where a waiver allows the state to design different Medigap plans. In other states, there are ten different Medigap plan designs. But in Massachusetts, there’s just the Medicare Core Plan and the Medicare Supplements 1 and 1A.8

Massachusetts added Medicare Supplement 1A as of 2020; it’s the same as Supplement 1 except that it does not cover the Medicare Part B deductible, which is $283 in 2026. The addition of Supplement 1A was necessary because federal law (MACRA) does not allow people who become eligible for Medicare in 2020 or later to enroll in a Medicare supplement that covers the Part B deductible. So people who were eligible for Medicare in Massachusetts in 2019 or earlier can choose from among all three supplement options, whereas people who become eligible for Medicare in 2020 or later cannot enroll in Supplement 1. (They can choose the Core Plan or Supplement 1A instead.)

Prior to 2006, Massachusetts also had Medicare Supplement 2, which included coverage for prescription drugs. Nationwide, all Medigap plans that included prescription drugs ceased to be available for purchase after the end of 2005 – people began enrolling in Medicare Part D instead – but people who had Supplement 2 in Massachusetts were allowed to keep it if they wanted to.

In addition to having different standardization rules for Medigap coverage, Massachusetts has among the country’s strongest consumer protections for Medigap plans. It’s one of nine states where insurers are required to use community rating, which means that premiums cannot vary based on age or medical history.9 Community rating even extends to disabled Medicare beneficiaries under age 65 in Massachusetts.10

The state also prohibits pre-existing condition waiting periods on Medigap plans. (In most states, Medigap insurers can impose pre-existing condition waiting periods of up to six months if the enrollee didn’t have continuous coverage before enrolling.)

Medigap plans are also available for purchase year-round in Massachusetts, without medical underwriting (meaning the person’s medical history does not affect their eligibility or premium).10

Technically, Massachusetts rules (see 211 CMR 17.10 (5)) require Medigap insurers to offer an open enrollment period in February and March each year. But the statute also prohibits insurers from “at any time” denying coverage or charging higher premiums based on medical history. In effect, this creates continuous year-round open enrollment for Medigap plans in Massachusetts.11

This is an unusual provision. People in most states who miss their initial six-month enrollment period or wish to pick a different plan later on do not have another guaranteed-issue opportunity to enroll, unless they qualify for one of the federal government’s limited guaranteed-issue rights for Medigap.

Can I get Medigap in Massachusetts if I’m under 65 and disabled?

Under federal Medicare rules, people who aren’t yet 65 can enroll in Medicare if they’re disabled and have been receiving disability benefits for at least two years, or if they have ALS or end-stage renal disease. But federal rules do not guarantee access to Medigap plans for people who are under 65.

Massachusetts is among the majority of the states that have implemented rules to ensure that disabled Medicare beneficiaries have at least some access to Medigap plans. Massachusetts requires Medigap insurers to offer coverage to disabled Medicare beneficiaries under age 65 and does not allow insurers to charge those enrollees higher premiums. The state’s Medigap community rating rules extend to disabled beneficiaries as well. This is unusual: while the majority of the states do require Medigap insurers to offer at least some plans to disabled beneficiaries, most states allow them to charge these enrollees higher premiums.

But while most of those states simply require Medigap insurers to offer at least some plans to any Medicare beneficiary under the age of 65, Massachusetts law notes that Medigap insurers are not required to offer coverage to people who are eligible for Medicare due to having end-stage renal disease. These individuals can enroll in a Medigap plan once they turn 65.10

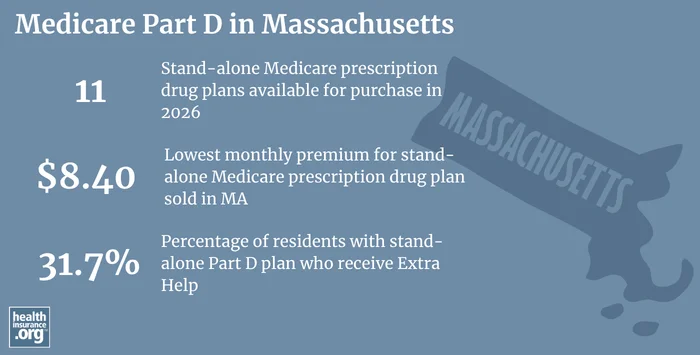

Medicare Part D plan availability and enrollment in Massachusetts

There are 11 stand-alone Medicare Part D prescription drug plans for sale in Massachusetts for 2026 with premiums starting at $8.40.3

As of January 2026, 751,215 Medicare beneficiaries in Massachusetts had stand-alone Medicare Part D prescription drug coverage . Another 502,490 had Medicare Part D prescription drug coverage as part of their Medicare Advantage plans.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Massachusetts

- If you have questions about Medicare eligibility in Massachusetts or Medicare enrollment in Massachusetts, the SHINE Program (Serving the Health Insurance Needs of Everyone) can help.

- Massachusetts also maintains a web page devoted to Massachusetts Medicare laws.

- The Medicare Rights Center is a nationwide service that can provide a variety of information and assistance with questions related to Medicare eligibility, enrollment, and benefits.

Looking for more information about other options in your state?

Need help navigating health insurance options in Massachusetts?

Explore more resources for options in MA including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Massachusetts” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – U.S” Centers for Medicare & Medicaid Services Data. Accessed April 20265 ⤶

- “Fact Sheet – Medicare Open Enrollment 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025. ⤶ ⤶

- “Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings” KFF.org. Dec. 9, 2025 ⤶

- “Medicare Monthly Enrollment – Massachusetts” Centers for Medicare & Medicaid Services Data. Accessed April 2026 ⤶

- “The State of Medicare Supplement Coverage” Page 12. AHIP, May 2025 ⤶

- “Medicare Supplement Plans Offered in Massachusetts, 2024/2025” Mass.gov. Accessed May 12, 2026 ⤶

- “Medigap in Massachusetts” Medicare.gov. Accessed May 12, 2026 ⤶

- “Key Facts About Medigap Enrollment and Premiums for Medicare Beneficiaries” KFF.org. Oct. 18, 2024 ⤶

- “2026 Medicare Beginner’s Guide for Massachusetts Consumers” Mass.gov. Revised Mar. 2026 ⤶ ⤶ ⤶

- “211 CMR, § 71.10 – Open Enrollment and Guarantee Issue for Medicare Supplement Insurance” Cornell Law School, Legal Information Institute. Accessed May 12, 2026 ⤶