Medicare in Mississippi

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Mississippi

Key takeaways

- Of Mississippi’s Medicare beneficiaries, almost 16% are eligible due to a disability, rather than age.1

- 43% of Mississippi Medicare beneficiaries are enrolled in Medicare Advantage plans.1

- More than 500,000 Mississippi Medicare beneficiaries have Medicare Part D coverage, either stand-alone or integrated with Advantage plans.1

Medicare enrollment in Mississippi

As of September 2024, there were 640,993 people with Medicare in Mississippi.1 That was more than 17% of the state’s population.2

For most people, filing for Medicare benefits goes along with turning 65; most Americans become eligible for premium-free Medicare Part A when they turn 65, and are either automatically enrolled (if they’re already receiving Social Security benefits) or can apply for coverage starting three months before they turn 65.

But Medicare eligibility is also triggered once a person has been receiving disability benefits for 24 months, or when a person has ALS or kidney failure. Nationwide, about 11% of all Medicare beneficiaries are eligible due to disability,3 but almost 16% of people with Medicare in Mississippi are under the age of 65 and disabled.1

Learn about Medicare plan options in Mississippi by contacting a licensed agent.

Explore our other comprehensive guides to coverage in Mississippi

The ACA Marketplace allows individuals and families to shop for and enroll in ACA-compliant health insurance plans. Subsidies may be available based on household income to help lower costs.

Learn about the health insurance Marketplace in Mississippi.

Hoping to improve your smile? Dental insurance may be a smart addition to your health coverage. Our guide explores dental coverage options in Mississippi.

Learn about Mississippi’s Medicaid expansion, the state’s Medicaid enrollment and Medicaid eligibility.

Short-term health plans provide temporary health insurance for consumers who may find themselves without comprehensive coverage. Learn more about short-term plan availability in Mississippi.

Learn about short-term insurance regulations in Mississippi.

Frequently asked questions about Medicare in Mississippi

What is Medicare Advantage?

In most areas of the country, including all of Mississippi, Medicare beneficiaries have the option to get their healthcare coverage through Original Medicare (directly from the federal government) or from a private Medicare Advantage plan.

Plans include all the covered benefits of Original Medicare (hospital services and outpatient/physician services), although the out-of-pocket costs can be quite different, as Medicare Advantage plans set their own copays, deductibles, and coinsurance, within parameters established by CMS (the maximum out-of-pocket limit for in-network care under Advantage plans in 2025 is $9,350,4 but most Advantage plans set their out-of-pocket caps below the upper allowable limit).

Most Medicare Advantage plans also include Part D coverage for prescription drugs, although the aforementioned maximum out-of-pocket does not include the cost of prescription drugs. And most also include extra benefits such as dental and vision coverage. But Advantage plans tend to have limited localized provider networks, as opposed to Original Medicare’s nationwide network of providers. There are pros and cons to either option.

As of 2018, only 17% of Medicare beneficiaries in Mississippi had selected Medicare Advantage plans, compared with an average of 34% nationwide. The large majority of Mississippi Medicare beneficiaries had opted for Original Medicare instead.

By September 2024, however, 43% of Mississippi Medicare beneficiaries were enrolled in Medicare Advantage plans,1 mirroring the nationwide trend towards increasing Medicare Advantage enrollment (nationwide, Advantage enrollment had grown to about 50% of all Medicare beneficiaries by late 2024).5

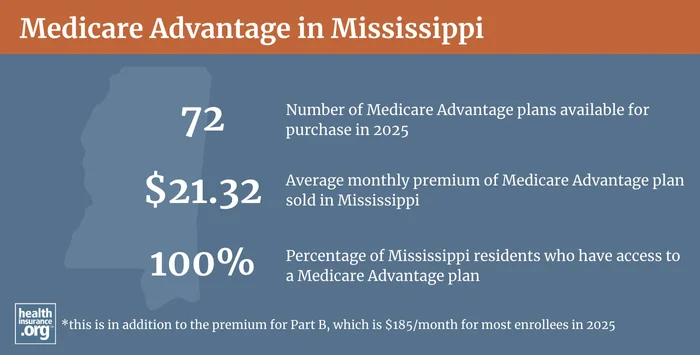

There are Medicare Advantage plans for sale in all 82 counties in Mississippi for 2025, although the number of available plans varies widely across the state: There are only seven plans available in Lowndes County, but residents in some counties can select from up as many as 30+ different Medicare Advantage plans.6

During the Medicare annual election period (October 15 to December 7), people with Medicare in Mississippi can switch between Medicare Advantage plans and Original Medicare (and can add or drop a Medicare Part D prescription plan), with their coverage changes effective January 1. People who are enrolled in Medicare Advantage plans also have the option to make coverage changes during the Medicare Advantage open enrollment period (January 1 to March 31). During this window, they can switch to a new Medicare Advantage plan or drop their Medicare Advantage plan and enroll in Original Medicare instead.

What are Medigap plans?

More than half of Original Medicare beneficiaries have employer-sponsored insurance or Medicaid to supplement their Medicare coverage. But for those who don’t, optional Medigap plans (also known as Medicare supplement plans) will cover some or all of the out-of-pocket healthcare costs for Medicare coinsurance and deductibles that the enrollee would otherwise have to pay themselves. Original Medicare does not cap out-of-pocket costs, and coinsurance and deductibles can add up quickly.

Medigap plans are sold by private insurers, but are standardized under federal rules, with ten different plan designs (differentiated by letters, A through N). The covered benefits of a particular plan (Plan A, Plan G, etc.) are the same from one insurer to another, making it fairly easy for consumers to compare plans (the plans will differ on things like price and customer service).

As of 2025, there are 38 insurers licensed to sell Medigap plans in Mississippi.7 And 164,457 people had Medigap coverage in Mississippi as of December 20222, according to an AHIP analysis.8

Read the Mississippi Insurance Department’s Medicare Supplement Shopper’s Guide.

Medigap plans differ from other private Medicare coverage (Medicare Advantage and Medicare Part D plans) in that there is not an annual open enrollment window for Medigap. Instead, people are given a single six-month guaranteed-issue window that begins when they are at least age 65 and enrolled in Medicare Part B (you have to be enrolled in both Part A and Part B to buy a Medigap plan).

Federal rules do not guarantee access to Medigap plans for people who are under 65 and enrolled in Medicare due to a disability. But Mississippi is one of the majority of the states that have implemented rules to ensure at least some access to Medigap coverage for people under age 65.

As explained in the state guide to Medicare supplement plans, people who become eligible for Medicare under the age of 65 are granted the same six-month open enrollment window for Medigap as people who gain eligibility for Medicare when they turn 65. Insurers have to offer all of their Medigap plans to disabled enrollees, but the premiums can be higher — the state notes that they can be up to 50% higher than the rates that apply to people who are 65 years old. A disabled beneficiary under age 65 will have another Medigap open enrollment period upon turning 65, allowing them the option to switch plans and enroll at a lower price than they were paying before turning 65.

It’s important to understand that although pre-existing conditions are no longer an issue in most of the private health insurance market as a result of the Affordable Care Act, those regulations don’t apply to Medigap plans. When you enroll in a Medigap plan, the insurer can impose a pre-existing condition waiting period of up to six months, if you didn’t have at least six months of continuous coverage prior to your enrollment. And if you apply for a Medigap plan after your initial enrollment window closes (and assuming you aren’t eligible for one of the limited guaranteed-issue rights), the insurer can use your medical history to determine your eligibility for coverage and your premium amount.

What is Medicare Part D?

Original Medicare does not cover outpatient prescription drugs. Many Original Medicare beneficiaries have supplemental coverage from an employer-sponsored plan, and these plans often include prescription coverage.

But Medicare beneficiaries who don’t have such coverage need to obtain prescription coverage under a Medicare Medicare Part D plan. These can be purchased as stand-alone coverage, or as part of a Medicare Advantage plan that includes Part D prescription drug coverage. Part D coverage is optional, but there’s a late enrollment penalty for people who didn’t enroll when they were first eligible and didn’t have creditable coverage.

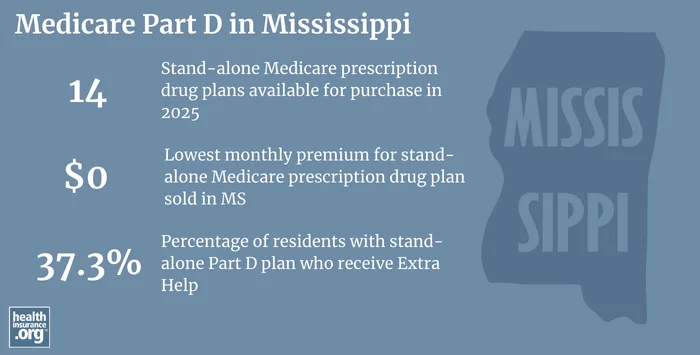

There are 14 stand-alone Medicare Part D plans for sale in Mississippi for 2025, with monthly premiums starting at $0/month.9

506,317 Mississippi Medicare beneficiaries (more than three-quarters of the state’s total Medicare population) had Medicare Part D coverage as of September 2024.1That included more than 244,161 with stand-alone Part D plans, and more than 262,156 who had Part D coverage integrated with Medicare Advantage plans.1 Although overall enrollment in Part D coverage has been increasing in Mississippi in line with increasing Medicare enrollment, the number of people with stand-alone Part D coverage has been decreasing, since an increasing percentage of the Medicare population is choosing Medicare Advantage plans.

Medicare Part D enrollment follows the same schedule as Medicare Advantage enrollment. Beneficiaries can pick a plan when they’re first eligible for Medicare, and there’s also an annual window each fall (October 15 – December 7) when Medicare beneficiaries can enroll for the first time or change to a different plan.

Seven rules for shopping for Medicare Part D plans

What additional resources are available for Medicare beneficiaries and their caregivers in Mississippi?

If you have questions about Medicare eligibility in Mississippi or Medicare enrollment in Mississippi, you can contact the Mississippi Health Insurance Assistance Program (SHIP). They can provide information and assistance with a wide range of questions related to Medicare coverage in Mississippi.

The Mississippi Insurance Department has a resource page for state residents who need help or have questions about Medicare in Mississippi, and a useful Medigap shopper’s guide. The Insurance Department regulates the insurers that offer Medigap plans in the state, as well as agents and brokers who sell any type of Medicare coverage (governance of Medicare Advantage plans and Part D plans is mostly done by CMS, although states do license the insurers and oversee them to ensure financial solvency). Their office can provide assistance with a range of insurance-related inquiries and complaints.

The Medicare Rights Center is a nationwide service that can provide information and assistance with questions related to Medicare eligibility, enrollment, and benefits.

Read more about how Medicaid supports more than one in five Medicare beneficiaries nationwide, and the specifics of how Mississippi Medicaid can assist Medicare beneficiaries with limited income and assets.

Looking for more information about other options in your state?

Need help navigating health insurance options in Mississippi?

Explore more resources for options in MS including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Mississippi.” Centers for Medicare & Medicaid Services Data. Accessed January, 2025. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- U.S. Census Bureau Quick Facts: United States & Mississippi.” U.S. Census Bureau, July 2024. ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed January, 2025. ⤶

- “Maximum out-of-pocket limit.” Medicare Interactive. Accessed January, 2025. ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed January, 2o25. ⤶

- ”Medicare Advantage 2025 Spotlight: First Look” KFF.org January, 2025 ⤶

- “Explore your Medicare coverage options.” Medicare.gov. Accessed October, 2024. ⤶

- ”The State of Medicare Supplement Coverage” AHIP. May 2024 ⤶

- ”Fact Sheet: Medicare Open Enrollment for 2025” (74) Centers for Medicare & Medicaid Services. Sep. 27, 2024 ⤶