Medicare in New Hampshire

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in New Hampshire

In this article

Medicare enrollment in New Hampshire

As of February 2026, there were 357,517 residents with coverage through Medicare in New Hampshire.1

Most individuals become eligible for Medicare enrollment when they turn 65. But younger individuals gain Medicare eligibility after they have been receiving disability benefits for 24 months, or if they have end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS). In New Hampshire, about 10% of Medicare beneficiaries are under 65 and eligible due to disability rather than age.1

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how New Hampshire’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

Medicare Advantage plan availability and enrollment in New Hampshire

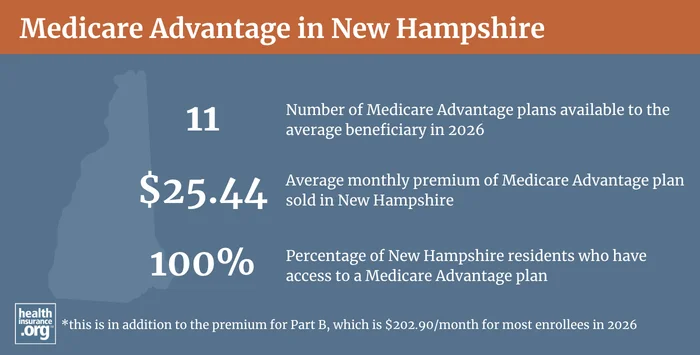

As of February 2026, over 51% of Medicare beneficiaries nationwide were enrolled in Medicare Advantage, while about 49% were enrolled in Original Medicare.2 But in New Hampshire, only about 31% of Medicare beneficiaries were enrolled in Medicare Advantage, and the other 69% were enrolled in Original Medicare.3

Medicare Advantage plan availability varies by county, but all counties in New Hampshire have individual Medicare Advantage plans available. In 2026, residents in New Hampshire have, on average, 11 plans from which to choose.4

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in New Hampshire by contacting a licensed agent.

Medicare supplement (Medigap) plan availability in New Hampshire

There were 99,250 New Hampshire residents with Medigap coverage as of 2023, according to an AHIP report.5

There were 23 insurers in New Hampshire approved to offer Medigap plans as of 2026.6

The state of New Hampshire maintains a Medigap rate comparison tool that residents can use to see pricing, benefits information, and plan availability.

Unlike other Medicare plan coverage (Medicare Advantage and Medicare Part D prescription drug plans), there is no Medicare Annual Open Enrollment window for Medigap plans. Instead, federal rules provide a one-time six-month window when Medigap coverage is guaranteed-issue. This window starts when a person is at least 65 and enrolled in Medicare Part B. (You must be enrolled in both Part A and Part B to buy a Medigap plan.) Once that initial enrollment window ends, Medigap insurers in nearly all states can use medical underwriting to determine an applicant’s eligibility for coverage, unless one of the limited guaranteed-issue rights applies.

New Hampshire lawmakers have considered some bills in the last several years that would have expanded Medigap consumer protections, plan change options, etc., including SB646 in 2020 and HB774 in 2025. But neither of those bills passed.

SB124, which initially included a “birthday rule” provision, was enacted in 2021. But the birthday rule guaranteed issue provision was removed from the bill during the legislative process, and the bill ultimately only ensured that Medigap insurers could not continue to charge the higher under-65 rates once a disabled Medigap enrollee turns 65.

Is Medigap available if you are under 65 in New Hampshire?

People who aren’t yet 65 can enroll in Medicare if they’re disabled and have been receiving disability benefits for at least two years, or if they have end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS); about 10% of New Hampshire Medicare beneficiaries are under age 65.7 Federal rules do not guarantee access to Medigap plans for people who are under 65, but the majority of the states have implemented rules to ensure that disabled Medicare beneficiaries have at least some access to Medigap plans. New Hampshire was among the first states to require Medigap insurers to offer plans to people under age 65, with a rule that took effect in the late 1990s. The state’s requirements were reiterated in a 2005 bulletin issued by the New Hampshire Insurance Department.8

All Medigap plans in New Hampshire are available to disabled enrollees under age 65, as long as they enroll during the six-month window that begins when they’re enrolled in Medicare Part B. Premiums are higher than the age-65 rates for these enrollees – substantially so for some insurers, and modestly higher for others.9 Disabled Medicare beneficiaries have another Medigap Open Enrollment Period when they turn 65. At that point, they can switch to a plan with the lower premiums that apply to people who are aging into Medicare, rather than qualifying due to disability. And SB124, enacted in 2021, prohibits Medigap insurers from continuing to charge the higher premiums once a disabled enrollee turns 65. So regardless of whether the person switches to a different plan or keeps the plan they already have, their Medigap rates will reset to the lower age-65 rates once they turn 65.

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

Medicare Part D plan availability and enrollment in New Hampshire

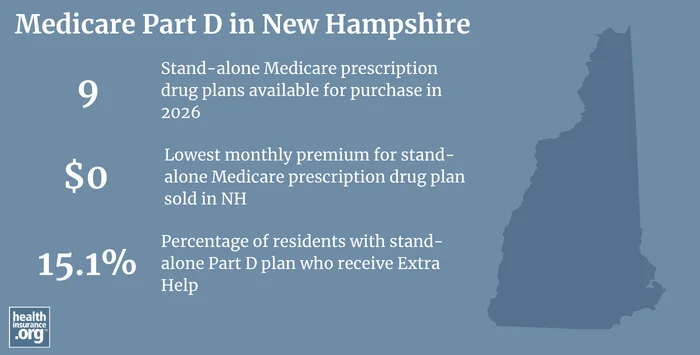

There are 9 stand-alone Medicare Part D prescription drug plans in New Hampshire for 2026, with premiums starting at $0 per month.10

In New Hampshire as of February 2026, there were 173,885 people with stand-alone Part D prescription drug coverage.3 Another 100,747 beneficiaries of Medicare in New Hampshire had Medicare Part D prescription coverage as part of their Medicare Advantage plans.3

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in New Hampshire

Need help filing for Medicare benefits? Got questions about Medicare eligibility in New Hampshire?

- You can contact New Hampshire’s Service Link Aging and Disability Resource Center with questions related to Medicare coverage in New Hampshire.

- The New Hampshire Insurance Department oversees and regulates health insurance companies in New Hampshire as well as the brokers and agents who sell policies in the state. They can provide assistance, answer questions, and address complaints from consumers regarding the entities they license and regulate.

- The Medicare Rights Center is a nationwide service, with a website and call center, that can provide information and assistance to Medicare beneficiaries.

- This overview of Medicaid programs for Medicare beneficiaries in New Hampshire is a helpful resource for beneficiaries with limited financial resources.

Looking for more information about other options in your state?

Need help navigating health insurance options in New hampshire?

Explore more resources for options in NH including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – New Hampshire” Centers for Medicare & Medicaid Services Data. Accessed, May 2026. ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶

- “Medicare Monthly Enrollment – New Hampshire” Centers for Medicare & Medicaid Services Data. Accessed, May 2026. ⤶ ⤶ ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org. Dec. 9, 2025 ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Medicare Supplement Rate Dashboard” New Hampshire Insurance Department. Accessed May 26, 2026 ⤶

- “Medicare Monthly Enrollment – New Hampshire” Centers for Medicare & Medicaid Services Data. Accessed May 27, 2026 ⤶

- “Ins 1905.10, Medicare Supplement Product” New Hampshire Insurance Department. Nov. 17, 2005 ⤶

- “New Hampshire’s 2026 Guide to Medicare Supplement Insurance, Version 2026-1.2” New Hampshire Insurance Department. May 15, 2026 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶