Medicare in New Jersey

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in New Jersey

Medicare enrollment in New Jersey

As of February 2026, Medicare enrollment in New Jersey stood at more than 1.8 million residents.1 Most of them – about 92% – are eligible for Medicare due to their age (meaning they’re at least 65). But roughly 8% are eligible for Medicare coverage due to a disability that lasts at least 24 months, or a diagnosis of amyotrophic lateral sclerosis (ALS) or end-stage renal disease (ESRD).1 Nationwide, about 91% of enrollees use Medicare benefits due to age, while 9% are eligible due to disability.2

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how New Jersey’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

Medicare Advantage plan availability and enrollment in New Jersey

As of February 2026, about 42% of Medicare beneficiaries in New Jersey had coverage under Medicare Advantage plans.1 Nationwide, the average is 51%.2 The other 58% of New Jersey’s Medicare beneficiaries opted instead for coverage under Original Medicare.1

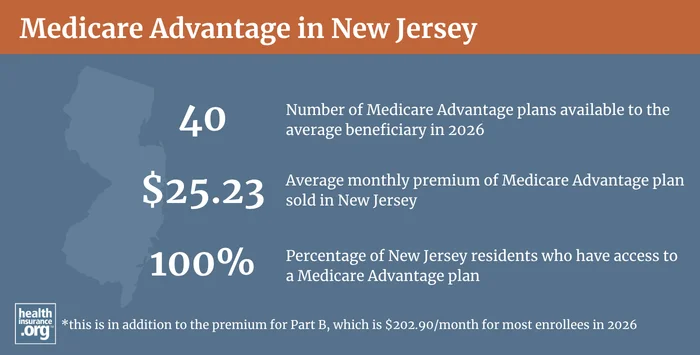

All counties in New Jersey have Medicare Advantage plans available in 2026, but plan options vary by county. On average, 40 plans are available to New Jersey beneficiaries.3

The average Medicare Advantage premium in New Jersey in 2026 is $25.23/month (in addition to the premium for Medicare Part B). But all Medicare beneficiaries in New Jersey have access to Medicare Advantage plans with $0 premiums (meaning the enrollee only has to pay the premium for Medicare Part B).4

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in New Jersey by contacting a licensed agent.

Medicare supplement (Medigap) plan availability in New Jersey

Medigap plans are used to supplement Original Medicare, covering some or all of the out-of-pocket costs (for coinsurance and deductibles) that people would otherwise incur if they only had Original Medicare on its own.

Twenty insurers offer Medigap plans in New Jersey as of 2026.5

Under federal rules, people are granted a six-month window, when they are at least 65 and enrolled in both Medicare Part A and Part B, during which Medigap plans are guaranteed-issue, regardless of medical history. However, federal rules do not guarantee access to a Medigap plan if you’re under 65 and eligible for Medicare as a result of a disability.

But New Jersey is among the majority of the states that have adopted rules to ensure at least some access to Medigap plans for enrollees under the age of 65. And New Jersey goes further than many other states by also ensuring that people under age 65 don’t pay higher premiums for their Medigap coverage.6

New Jersey’s consumer protections for disabled Medigap enrollees include provisions for those under age 50, and for those age 50-64. In both cases, as long as the person applies for a Medigap plan (Medigap Plan D, as of 2020) within six months of enrolling in Medicare Part B, the coverage is guaranteed issue and the price won’t be more than the insurer charges for enrollees who are eligible for Medicare due to their age (as opposed to a disability). But younger applicants only have guaranteed-issue access to Medigap Plan D (or Plan C, for those who became eligible for Medicare before 2020). And there is only one insurer option for those under age 50, while applicants between 50 and 64 can select Plan D (or Plan C, for those who became eligible for Medicare before 2020) from any Medigap insurer in their area:

- For Medicare beneficiaries who are under age 50, coverage is guaranteed issue only with the state’s contracted carrier (Horizon Blue Cross Blue Shield of New Jersey)7 and the available plan is Medigap Plan D (or Plan C for those who became eligible for Medicare prior to 2020). The state runs a program so that all carriers that offer health benefits in New Jersey share in the Medigap losses incurred by the contracted carrier for these enrollees.6 As of 2026, the monthly premium for Horizon’s Plan D for Medicare beneficiaries under age 50 was about $196/month for men and $182/month for women, which was the same as Horizon’s Plan D rates for 65-year-olds.8

- For Medicare beneficiaries between the ages of 50 and 64, coverage for Plan D (or Plan C for those who became eligible for Medicare prior to 2020) is guaranteed issue with any insurer in New Jersey that offers Medigap plans.9 And insurers must maintain loss ratios of at least 65% for individual policies and 75% for group policies.6

Under federal law (MACRA) that was enacted in 2015, Medigap Plans C and F can no longer be sold to people who become eligible for Medicare on or after January 1, 2020. So New Jersey enacted legislation (S.3651) in 2019 to align the state’s existing law with the new federal requirements. Starting in 2020, Plan D became the guaranteed-issue Medigap plan for newly-eligible disabled Medicare beneficiaries in New Jersey, instead of Plan C.

Legislation under consideration in New Jersey in 2026 (A2301 and S2592) would require Medigap plans to have continuous open enrollment in New Jersey. But similar legislation introduced in 2019(A.4834 and S.2895) and 2023 (S.1162) did not advance. The current rules (which mirror federal requirements) only grant people a one-time six-month window during which they can pick a Medigap plan with guaranteed-issue rights. People who miss that window or wish to change their plan later on are often unable to pick a different plan at a later date, because insurers can use medical underwriting to determine eligibility for coverage after that one-time enrollment window closes.

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

Medicare Part D plan availability and enrollment in New Jersey

As of February 2026, there were 930,086 Medicare beneficiaries in New Jersey who were enrolled in stand-alone Part D prescription drug plans. In addition, another 549,166 New Jersey Medicare beneficiaries had Part D coverage integrated with a Medicare Advantage plan.1

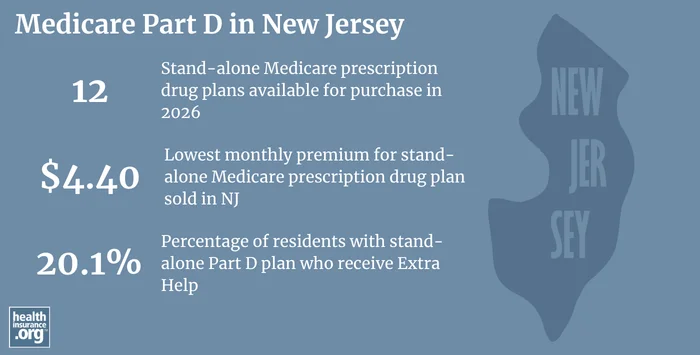

For 2026 coverage, there are 12 stand-alone Part D plans available in New Jersey, with premiums starting at $4.40/month.4

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in New Jersey

These resources provide free assistance and information about Medicare programs and availability in New Jersey.

- The New Jersey State Health Insurance Assistance Program can help with questions related to Medicare coverage in New Jersey.

- New Jersey’s Division of Aging Services website has a variety of resources that are helpful for people with Medicare in New Jersey.

- The New Jersey State Library website has a page devoted to social services for seniors in New Jersey.

Looking for more information about other options in your state?

Need help navigating health insurance options in New jersey?

Explore more resources for options in NJ including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – New Jersey” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶

- “Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings” KFF.org. Dec. 9, 2025 ⤶

- “Fact Sheet – Medicare Open Enrollment 2026” Centers for Medicare and Medicaid Services. Sep. 26, 2025. ⤶ ⤶

- “New Jersey Medicare Supplement Policies (Medigap) Monthly Premium at Age 65” NJ.gov. Revised Jan. 13, 2026 ⤶

- “Medicare Supplement Coverage for Individuals Eligible for Medicare due to Disability” NJ.gov. Accessed May 29, 2026 ⤶ ⤶ ⤶

- “Medicare Supplement Coverage Sold in New Jersey for those Under Age 50” and “Medicare Supplement Coverage for Individuals Eligible for Medicare due to Disability” NJ.gov. Accessed May 29, 2026 ⤶

- “2026 Medicare Supplement Plan Outline of Coverage” Horizon BCBS. Accessed May 29, 2026 ⤶

- “NJ Medicare Supplement Coverage for People Between Ages 50 and 65 on Medicare Due to Disability January 2025” NJ.gov. Accessed Jan. 22, 2025 ⤶