Medicare in New York

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in New York

Medicare enrollment in New York

As of January 2026, over 4 million people were covered by Medicare in New York.1In most cases, individuals become eligible for Medicare enrollment at age 65, but individuals who have been receiving disability benefits for at least 24 months are also eligible for Medicare, as are those with amyotrophic lateral sclerosis (ALS) or end-stage renal disease (ESRD). (Those latter two groups do not have to wait 24 months for their Medicare eligibility to take effect.)

In New York, about 9% of Medicare beneficiaries are under 65 and eligible due to disability.2

- Understand the difference between Medigap, Medicare Advantage, and Medicare Part D (including tips for picking the best coverage combination to meet your needs).

- Learn how Medicaid can provide assistance to New York Medicare beneficiaries who have limited financial resources.

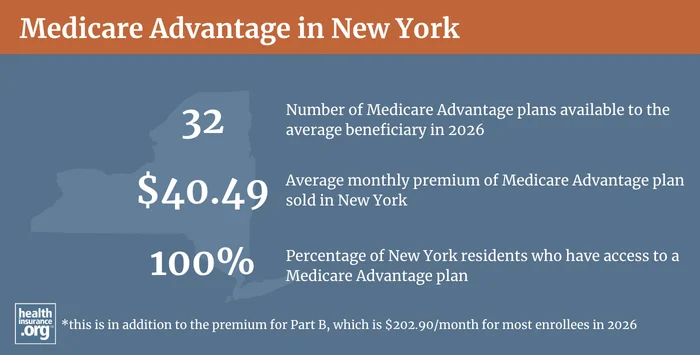

Medicare Advantage plan availability and enrollment in New York

New York has a fairly robust Medicare Advantage market. In 2026, the average Medicare beneficiary in New York can choose from among 25 Medicare Advantage plans.3 As of January 2026, 53% of New York’s Medicare beneficiaries were enrolled in Medicare Advantage, while 47% were enrolled in Original Medicare.2

Learn more about Medicare Advantage and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in New York by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in New York

There are 12 insurers that offer Medicare supplement (Medigap) plans in New York.4

New York has among the strongest Medigap consumer protections in the nation.5 As long as a person in New York is enrolled in Medicare Part A and Medicare Part B, they can enroll in a Medigap plan at any time, year-round, and premiums do not vary based on the applicant’s age or health status. This is also true for enrollees who are under 65 and eligible for Medicare due to a disability. Premiums do vary from one insurer to another, and from one area to another.6 2026 premiums are available here; an insurer can only vary the price of a particular Medigap plan based on where enrollees resides.

New York’s rules go far beyond the federal rules, and beyond the rules that most states have imposed on Medigap insurers. (Connecticut is the only other state where Medigap is available year-round, without medical underwriting; several other states offer windows each year when some or all plans are guaranteed-issue).7 Federal rules do not require an annual open enrollment window for Medigap plans. Instead, federal rules provide only a one-time six-month window when Medigap coverage is guaranteed-issue, starting when the person is at least 65 and enrolled in Medicare Part B. And federal rules don’t guarantee access to Medigap plans at all for people who are under 65 and enrolled in Medicare due to a disability. New York’s rules are much more robust.

Because of the year-round availability, community rating, and lack of medical underwriting, premiums for Medigap enrollees in New York are generally higher than they are in most other states when enrollees are 65.7

Although the Affordable Care Act eliminated pre-existing condition exclusions in most of the private health insurance market, those regulations don’t apply to Medigap plans, and New York allows Medigap insurers to conform to federal Medigap regulations for pre-existing conditions.8 Medigap insurers can impose a pre-existing condition waiting period of up to six months, if an applicant didn’t have at least six months of continuous coverage prior to enrolling. But beyond that, consumers are protected in New York. In most other states, people enrolling after their initial six-month open enrollment window can be denied coverage or charged higher premiums due to pre-existing conditions, and that’s not the case in New York.

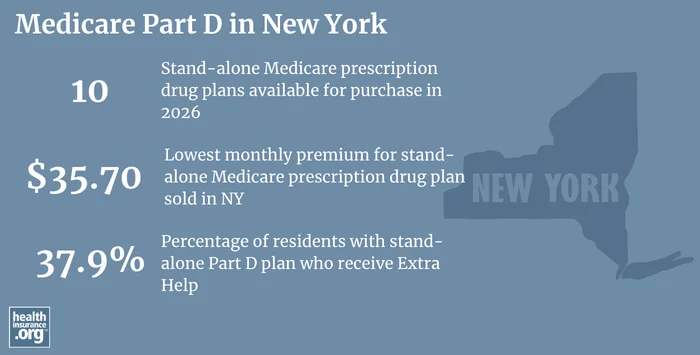

Medicare Part D plan availability and enrollment in New York

In 2026, insurers in New York are offering 10 stand-alone Medicare Part D prescription drug plans, with premiums starting at $35.70 per month.9

As of January 2026, 1,391,546 New Yorkers had stand-alone Medicare Part D prescription drug plans, while another 1,973,577 had Medicare Part D prescription drug coverage integrated with their Medicare Advantage plans.2

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in New York

Need help with your Medicare application in New York, or have questions about Medicare eligibility in New York? These resources provide free assistance and information.

- HIICAP, New York’s Health Insurance Information Counseling and Assistance program.

- The Medicare Rights Center provides helpful information geared to Medicare beneficiaries, caregivers, and professionals.

- Access the New York State Department of Financial Services for helpful information about Medicare.

Looking for more information about other options in your state?

Need help navigating health insurance options in New york?

Explore more resources for options in NY including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – New York” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶

- “Medicare Monthly Enrollment – New York” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶ ⤶ ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org. Dec. 9, 2025 ⤶

- “Medicare and Supplement or ‘Medigap’ Insurance” New York Department of Financial Services. Accessed May 4, 2026 ⤶

- “Why New York Is One of the Best States for Medicare Beneficiaries” New York State Bar Association. May 12, 2025 ⤶

- “58.1 Rules relating to content of forms for Medicare supplement insurance” New York Codes, Rules, and Regulations. Accessed May 4, 2026 ⤶

- “Key Facts About Medigap Enrollment and Premiums for Medicare Beneficiaries” KFF.org. Oct. 18, 2024 ⤶ ⤶

- “Health Insurance” New York Department of Financial Services. Accessed May 4, 2026 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶