Medicare in Oklahoma

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Oklahoma

Medicare enrollment in Oklahoma

As of February 2026, there were 825,143 Oklahoma residents with Medicare coverage.1

In most cases, enrolling in Medicare goes along with turning 65, and people who are already receiving Social Security or Railroad Retirement benefits are automatically enrolled in Medicare when they turn 65.

But people also become eligible for Medicare if they have end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS), or after they’ve been receiving disability benefits for 24 months. As of early 2026, about 12% of Medicare beneficiaries in Oklahoma were eligible due to a disability rather than age.1 Nationwide, about 9% of all Medicare beneficiaries are under 65.2

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn about how the Oklahoma’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

Medicare Advantage plan availability and enrollment in Oklahoma

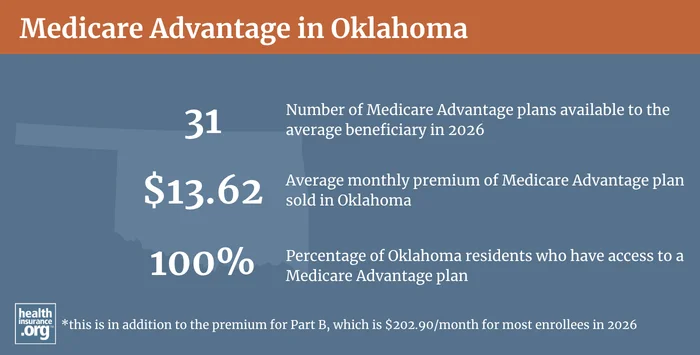

As of February 2026, enrollment in Medicare Advantage plans in Oklahoma had grown to nearly 43% of the state’s total Medicare population,1 with 350,742 Oklahoma Medicare beneficiaries enrolled in Medicare Advantage plans. The other 474,401 enrollees had Original Medicare.1

The availability of Medicare Advantage plans in Oklahoma varies from county to county, but all counties in the state have Medicare Advantage plans available in 2026. The average Medicare beneficiary in Oklahoma can choose from among 31 Medicare Advantage plans in 2026.3

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Oklahoma by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in Oklahoma

Twenty-nine insurers offered Medigap plans in Oklahoma as of 2026,4 and according to an AHIP analysis, there were 187,452 Medicare beneficiaries in Oklahoma who had Medigap coverage as of late 2023.5

Unlike other Medicare coverage (Medicare Advantage plans and Medicare Part D prescription drug plans), there is no annual open enrollment window for Medigap plans.6 Instead, federal rules give enrollees a one-time six-month window when Medigap coverage is guaranteed-issue. This window starts when a person is at least 65 and enrolled in Medicare Part B (you must be enrolled in both Part A and Part B to buy a Medigap plan).

However, Oklahoma has created an annual opportunity for Medigap enrollees to switch to another Medigap plan with equal or lesser benefits, on a guaranteed-issue basis, as long as they haven’t had more than a 90-day gap in coverage since they first enrolled in Medigap. This opportunity became available in September 2023. To comply with the rule, Medigap carriers must, at a minimum, provide an opportunity for enrollees to switch to another plan with equal or lesser benefits during a 60-day window that starts on the enrollee’s birthday.7 This document has a chart showing which plans are available, depending on the enrollee’s current plan.

People who aren’t yet 65 can enroll in Medicare if they’re disabled and have been receiving disability benefits for at least two years, and more than 102,000 Medicare beneficiaries in Oklahoma are under age 65.8 Federal rules do not guarantee access to Medigap plans for people who are under 65, but Oklahoma is among the majority of the states that have implemented rules to ensure that disabled Medicare beneficiaries have at least some access to Medigap plans.

Oklahoma was one of the first states to address this issue, and has guaranteed access to Medigap plans for people under age 65 since 1994. The initial rule just required Medigap insurers to offer at least one plan to applicants under the age of 65. But since 2017, state law has also limited the premiums that insurers can charge disabled beneficiaries (see OAC 365:10-5-129(d)). Medigap insurers in Oklahoma have to offer at least one Medigap plan to enrollees under the age of 65, during a six-month open enrollment period that begins when the person is enrolled in Medicare Part B. And insurers cannot charge a premium higher than the lowest available age-based premium that applies to that plan (meaning the highest rate that would be charged for someone older than 65; insurers typically have age bands for this, so the rates for an 80-year-old are higher than the rates for a 65-year-old, but a person under age 65 can’t be charged more than the highest rate for people age 65+).

All of Oklahoma’s Medigap insurers have opted to offer only Medigap Plan A for enrollees under the age of 65.9

People who have Medicare prior to age 65 are granted a six-month Medigap Open Enrollment Period when they turn 65, during which they can select any available plan from any insurer in their state, at the regular rates that are charged at age 65.6 Many more Medigap options are available to people who are turning 65 than to people below that age, so this is an opportunity for an enrollee to obtain more robust coverage if they prefer it (Plan A, which is the option that Oklahoma Medigap insurers make available to people under age 65, is the least comprehensive Medigap plan). Oklahoma requires Medigap insurers to notify under-65 enrollees (prior to their 65th birthday) that their window to enroll in any plan on a guaranteed-issue basis is approaching.10

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

Medicare Part D plan availability and enrollment in Oklahoma

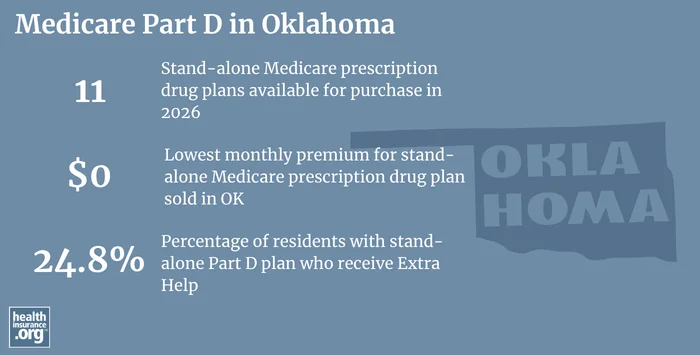

For 2026 coverage, there are 11 stand-alone Medicare Part D prescription drug plans in Oklahoma, with premiums that start at $0/month.11

As of February 2026, 309,196 Oklahoma Medicare beneficiaries had prescription drug coverage under stand-alone Medicare Part D prescription drug (PDP) plan enrollment.1 Another 314,274 Oklahoma Medicare beneficiaries had Medicare Part D prescription drug coverage integrated with their Medicare Advantage Prescription Drug (MAPD) plans.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries and their caregivers in Oklahoma

Questions about Medicare eligibility in Oklahoma or Medicare enrollment in Oklahoma?

- Visit the website for the Oklahoma Senior Health Insurance Counseling Program for answers to questions related to Medicare coverage in Oklahoma. If you prefer to call, the number is 1-800-763-2828.

- The Oklahoma Insurance Department maintains a page of resources for people who are eligible for Medicare in Oklahoma.

- Visit the Medicare Rights Center website or call 1-800-333-4114. This nationwide resource provides helpful information geared to Medicare beneficiaries, caregivers, and professionals.

Looking for more information about other options in your state?

Need help navigating health insurance options in Oklahoma?

Explore more resources for options in OK including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Oklahoma” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org. Dec. 9, 2025 ⤶

- “Explore your Medicare coverage options” Medicare.gov. Accessed May 28, 2026 ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Get Medigap Basics” Medicare.gov. Accessed May 28, 2026 ⤶ ⤶

- “New Medicare Supplement Open Enrollment FAQs” Oklahoma Insurance Department. Accessed May 28, 2026 ⤶

- “Medicare Monthly Enrollment – Oklahoma” Centers for Medicare & Medicaid Services Data. Accessed May 28, 2026 ⤶

- “Supplement Insurance (Medigap) Plans in Oklahoma” Medicare.gov. Accessed May 28, 2026 ⤶

- “Bulletin 10-2023: New Medicare Supplement Enrollment Requirements” Oklahoma Insurance Department. Sep. 1, 2023 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶