Medicare in Oregon

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Oregon

Key takeaways

- Over 940,000 residents are enrolled in Medicare in Oregon.1

- More than half of Oregon Medicare beneficiaries opt for Medicare Advantage plans.1

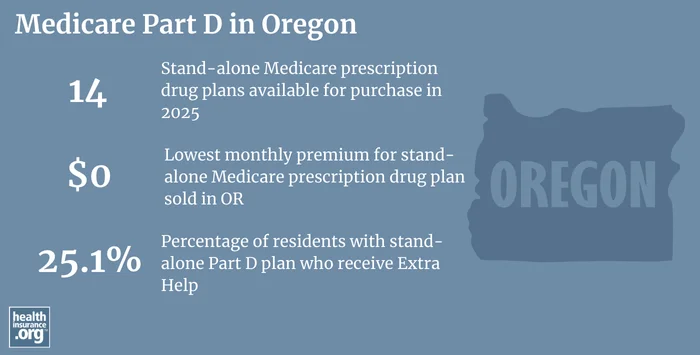

- Oregon has 14 stand-alone Medicare Part D drug plans in 2025, with premiums starting at $0 per month.2

Oregon Medicare enrollment

As of September 2024, enrollment for Medicare in Oregon stood at 944,474 people,1 amounting to nearly 20% of the state’s population.3

Most people become eligible for Medicare when they turn 65. But Medicare eligibility is also triggered when a person has been receiving disability benefits for 24 months, or has ALS or end-stage renal disease. Across the United States, about 11% of all Medicare beneficiaries are under the age of 65;4 in Oregon, just about 9% of Medicare beneficiaries are under 65 and eligible due to disability rather than age.1

Medicare options

Medicare beneficiaries can choose between Medicare Advantage plans, where coverage is through private health insurance companies, or Original Medicare, where benefits are provided directly by the federal government.

Original Medicare includes Part A (also called hospital insurance, which helps pay for inpatient stays at a hospital, skilled nursing facility, or hospice center) and Part B (also called medical insurance, which helps pay for outpatient care, like physician visits, durable medical equipment, preventive care, kidney dialysis, etc.).

Medicare Advantage plans provide all the benefits of Parts A and B, although cost-sharing amounts are generally different than they’d be with Original Medicare. Medicare Advantage plans usually also include other benefits like Part D prescription drug coverage, and dental and vision coverage. But they also tend to have much narrower provider networks and out-of-pocket costs are usually higher than they’d be with Original Medicare plus a Medigap plan. There are pros and cons to both options.

Learn about Medicare plan options in Oregon by contacting a licensed agent.

Explore our other comprehensive guides to coverage in Oregon

The ACA Marketplace allows individuals and families to shop for and enroll in ACA-compliant health insurance plans. Subsidies may be available based on household income to help lower costs.

Hoping to improve your smile? Dental insurance may be a smart addition to your health coverage. Our guide explores dental coverage options in Oregon.

Learn about Oregon’s Medicaid expansion, the state’s Medicaid enrollment and Medicaid eligibility.

Short-term health plans provide temporary health insurance for consumers who may find themselves without comprehensive coverage. Learn more about short-term plan availability in Oregon.

Frequently asked questions about Medicare in Oregon

What is Medicare Advantage?

Medicare Advantage plans allow beneficiaries to obtain their coverage via private plans instead of through Original — or traditional — Medicare (the federal government’s fee-for-service program). These plans are one option for consumers who desire additional benefits beyond what Original Medicare offers, and those who prefer lower total premiums (versus Medigap + stand-alone Part D) in trade for potentially higher out-of-pocket costs and more limited access to medical providers.

Medicare Advantage plans are run by private insurers that have more limited provider networks than Original Medicare. Although Medicare Advantage plans have caps on out-of-pocket costs (unlike Original Medicare on its own), the out-of-pocket exposure is generally more than a person would have if they purchased a Medigap plan and Part D plan to supplement Original Medicare.

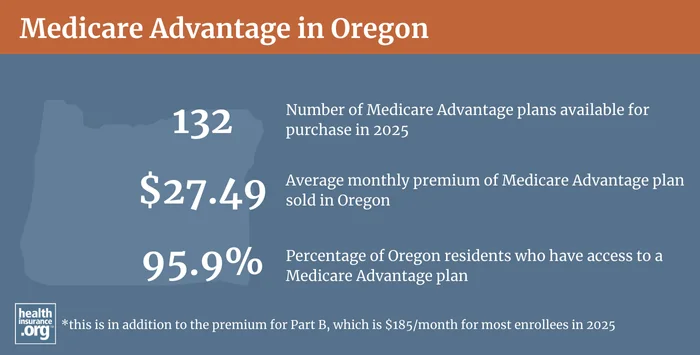

Over 519,000 of Oregon’s Medicare beneficiaries had Medicare Advantage plans as of September 2024.1

There are not Medicare Advantage plans available in every county in Oregon. The number of plans for sale in 2025 varies depending on the county.: 5

Medicare Advantage enrollment is available during the annual election period each fall (October 15 to December 7). And people who are already enrolled in Medicare Advantage plans can also use the Medicare Advantage open enrollment period that runs from January through March. It allows them to switch to a different Medicare Advantage plan or switch to Original Medicare.

What is Medigap?

Medigap plans are subject to various federal rules, but states also have a lot of say in how the plans operate. Oregon has a rule to ensure that Medigap enrollees aren’t stuck with their plan forever, regardless of their health status. And the state also guarantees access to Medigap plans for Medicare beneficiaries under age 65.

Medigap plans are standardized at the federal level, and federal law guarantees access to Medigap plans when people turn 65 and enroll in Medicare Part B (you have to also be enrolled in Medicare Part A in order to have Medigap, but the six-month open enrollment period for Medigap plans starts when you are at least 65 and enrolled in Part B).

But unlike Medicare Advantage and Part D, there’s no federal annual open enrollment period for Medigap plans; once that initial six-month window ends, it’s gone forever (except for the limited circumstances that trigger a guaranteed-issue right for Medigap). People who want to switch to a different Medigap plan are generally subject to medical underwriting, so healthy people can change plans, but those with pre-existing medical conditions may not be able to do so. And people under age 65 (who are eligible for Medicare due to a disability or having end-stage renal disease or ALS) are not guaranteed access to Medigap under federal rules.

To address this, Oregon implemented a “birthday rule” in 2013 that allows Medigap enrollees an annual opportunity to change to a plan with equal or lesser benefits during the 30 days following their birthday. The new plan is guaranteed issue during that window.

Oregon also allows Medicare beneficiaries under age 65 a six-month window (after enrolling in Medicare Part B) during which they have a guaranteed-issue right to a Medigap plan. Eligible enrollees can select a Medigap plan with no medical underwriting during a six-month window after they enroll in Medicare Part B, and the premium cannot exceed the premiums that are charged to enrollees who are 65.

In 2025, there are 21 insurers that offer Medigap plans in Oregon.6

There are three approaches to premiums that Medigap insurers can use: Attained-age rating, issue-age rating, and community rating. Oregon does not mandate one or the other, so most insurers in the state use attained-age rating. That means premiums increase as the enrollee gets older. There are a few Medigap insurers that use issue-age rating (premiums are based on the age the person was when they enrolled), while the rest use attained-age rating.

According to an AHIP analysis, 189,083 Medicare beneficiaries in Oregon had Medigap coverage as of late-2022.7

What is Medicare Part D?

Original Medicare does not cover prescription drugs, so most beneficiaries rely on optional Part D coverage to help cover drug costs. Some enrollees have prescription coverage via an employer-sponsored plan, but Medicare Part D plans are available for those who need to obtain their own prescription coverage (prior to 2006, there were some Medigap plans that included prescription coverage; those are no longer for sale, but people who still have them are allowed to keep them).

Medicare Part D was created under the Medicare Modernization Act of 2003. Medicare Part D coverage can be purchased on a stand-alone basis or integrated with a Medicare Advantage plan.

As of September 2024, there were 270,257 Oregon Medicare beneficiaries enrolled in stand-alone Medicare Part D plans.1 Another 495,905 beneficiaries had Medicare Part D coverage integrated with their Medicare Advantage plans.1

For 2025 coverage, there are 14 stand-alone Medicare Part D plans available in Oregon, with premiums starting at $0/month.8

Medicare Part D enrollment is available during Medicare’s annual open enrollment period in the fall (October 15 to December 7). Plan selections made during this window are effective as of the following January.

What additional resources are available for Medicare beneficiaries and their caregivers in Oregon?

If you need help with your Medicare application in Oregon or have questions about Medicare eligibility in Oregon, look into one of these resources. You can visit a website and browse for information, or call for more personalized assistance.

- Senior Health Insurance Benefits Assistance (SHIBA) can provide help with a wide range of issues related to Medicare in Oregon. SHIBA also maintains a page of FAQs about Medicare that include provisions specific to Oregon, such as the Medigap protections. The phone number is 1-800-722-4134.

- The Medicare Rights Center is also an excellent resource for Medicare-related questions. The national helpline number is 1-800-333-4114.

Looking for more information about other options in your state?

Need help navigating health insurance options in Oregon?

Explore more resources for options in OR including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Oregon.” Centers for Medicare & Medicaid Services Data. Accessed January, 2025. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- ”Fact Sheet: Medicare Open Enrollment for 2025” (PAGE NUMBER FOR APPLICABLE STATE) Centers for Medicare & Medicaid Services. Sep. 27, 2024 ⤶

- U.S. Census Bureau Quick Facts: United States & Oregon.” U.S. Census Bureau, July 2024. ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed January, 2025. ⤶

- ”Medicare Advantage 2025 Spotlight: First Look” KFF.org Nov. 15, 2024 ⤶

- “Explore your Medicare coverage options.” Medicare.gov. Accessed November, 2024. ⤶

- ”The State of Medicare Supplement Coverage” AHIP. May 2024 ⤶

- ”Fact Sheet: Medicare Open Enrollment for 2025” (113) Centers for Medicare & Medicaid Services. Sep. 27, 2024 ⤶