Medicare in Wisconsin

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Wisconsin

Medicare enrollment in Wisconsin

Medicare enrollment in Wisconsin stood at 1,360,081 people as of January 2026.1

In most cases, individuals are eligible for enrollment in Medicare when turning 65. But Medicare also provides coverage for disabled individuals under age 65 if they have been receiving disability benefits for 24 months, and for people with amyotrophic lateral sclerosis (ALS) or end-stage renal disease. Nationwide, about 9% percent of Medicare beneficiaries are under age 65,2 and around the same proportion of Wisconsin beneficiaries are under 65.3

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Wisconsin’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

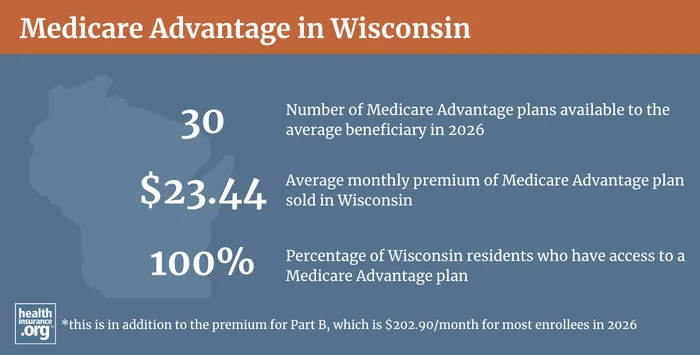

Medicare Advantage plan availability and enrollment in Wisconsin

Medicare Advantage includes all of the coverage provided by Medicare Parts A and Medicare Part B, and the plans often provide additional benefits, typically including integrated Medicare Part D prescription drug coverage and often coverage for expenses like dental and vision care. But Medicare Advantage insurers establish their own provider networks, which are generally localized and more limited than the nationwide network for Original Medicare. Out-of-pocket costs for Medicare Advantage are often higher than they would be if a beneficiary had Original Medicare plus a Medigap plan.

Medicare Advantage plans in Wisconsin are available for purchase statewide, and residents on average have access to 21 Medicare Advantage plans in 2026.4

As of January 2026, there were 781,420 Wisconsin Medicare beneficiaries enrolled in Medicare Advantage coverage.1

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Wisconsin by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in Wisconsin

Medigap plans (also known as Medicare supplement insurance plans, or MedSupp) will pay some or all of the out-of-pocket costs that enrollees would otherwise have to pay if they had only Original Medicare – which does not have a cap on out-of-pocket costs.

Sixteen insurers offer individual Medigap plans in Wisconsin in 2026, and three offer Medicare SELECT plans (Medigap with a provider network).5

According to an AHIP analysis, 299,015 Wisconsin Medicare beneficiaries had Medigap coverage as of 2023.6

Although private insurers sell Medigap plans, the policies in nearly every state are standardized under federal rules.7 But Wisconsin is one of just three states that have waivers from the federal government allowing the state to conduct its own Medigap standardization.7 So, Medigap plans in Wisconsin are not the same as they are in most of the rest of the country.8

Instead of having ten different plan designs available (as is the case in most states), Wisconsin Medigap is structured so that there’s one Medigap Basic Plan, plus versions with higher out-of-pocket costs (similar to Medigap Plans K and L that are available in other states). Then enrollees can choose to add riders that make the coverage more comprehensive.9 So instead of buying “Plan G” (as newly eligible enrollees in many states would do if they want the most comprehensive Medigap plan), Wisconsin Medigap enrollees buy the Medicare Basic Plan and then add on the optional riders.10

Wisconsin Medigap insurers have to offer “basic benefits” that include coverage for Medicare Part A coinsurance (including the Medicare Part A hospice coinsurance and hospital coinsurance), Medicare Part B coinsurance, and up to three pints of blood each year. Each Wisconsin Medigap insurer has to offer a “Basic Plan,” which includes the basic benefits in addition to Medicare Part A skilled nursing facility coinsurance, additional coverage for home health care and inpatient mental health care (both have limits on the number of days that are covered), outpatient mental health care, and Wisconsin state-mandated benefits.10

In addition, Wisconsin Medigap insurers can offer up to seven optional policy riders that beneficiaries can purchase, with coverage for expenses like the Medicare Part A deductible, additional home health care, the Medicare Part B deductible (for those who became eligible for Medicare prior to 2020)11 and excess charges, and foreign travel coverage for emergencies abroad.12

Medigap coverage similar to the various lettered plans sold in other states can thus be obtained in Wisconsin by layering various riders on top of the Basic Plan.10

Medigap insurers in Wisconsin can also offer cost-sharing plans that require the enrollee to pay a portion of the out-of-pocket costs until they reach a specified out-of-pocket limit (similar to Medigap Plans K and L that are sold in other states), and high-deductible plans that require the member the pay all costs until they meet the deductible for the year (similar to the high-deductible versions of Medigap Plans F and G that are sold in other states).10

Can I get Medigap in Wisconsin if I’m under 65 and disabled?

People who aren’t yet 65 can enroll in Medicare if they’re disabled and have been receiving disability benefits for at least two years. About 9% of Medicare beneficiaries in Wisconsin are under age 65. Federal rules do not guarantee access to Medigap plans for people who are under 65, but the majority of the states – including Wisconsin – have implemented rules to ensure that disabled Medicare beneficiaries have at least some access to Medigap plans.

Medigap insurers in Wisconsin are required to offer coverage to disabled enrollees under age 65, with the same six-month open enrollment period that begins when the person is enrolled in Medicare Part B.12 But premiums for people under the age of 65 are considerably higher than premiums for people who are 65 and over. And insurers are only required to offer the Medigap Basic Plan to applicants under the age of 65. There are only a handful of insurers that also offer the high-deductible plan or the plans with additional cost-sharing.13

Disabled Medicare beneficiaries also have access to the Medigap Open Enrollment Period when they turn 65. At that point, they can select from among any of the available Medigap plans, with lower premiums that apply to people who are aging onto Medicare when they turn 65.

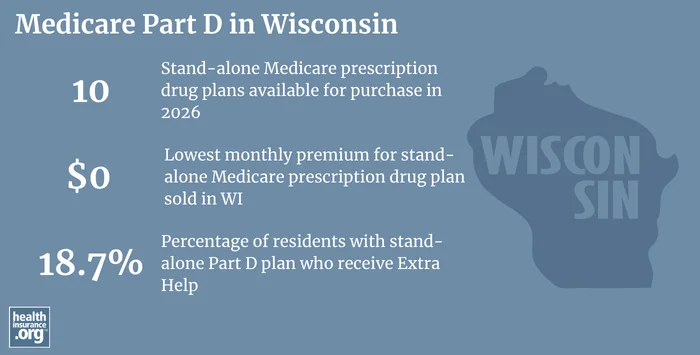

Medicare Part D plan availability and enrollment in Wisconsin

There are 10 stand-alone Medicare Part D prescription drug plans in Wisconsin in 2026, with premiums starting at $0 per month.14

As of January 2026, 455,187 of Wisconsin’s Original Medicare beneficiaries had stand-alone Medicare Part D plans.1 Another 635,424 Wisconsin Medicare beneficiaries had Medicare Part D prescription drug coverage integrated with their Medicare Advantage plans.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Wisconsin

Need help with your Medicare application in Wisconsin, or have questions about Medicare eligibility in Wisconsin? These resources provide free assistance and information.

- The Wisconsin Department of Health Services has a comprehensive list of resources related to Medicare coverage in Wisconsin.

- The Medicare Rights Center provides helpful information geared to Medicare beneficiaries, caregivers, and professionals.

Looking for more information about other options in your state?

Need help navigating health insurance options in Wisconsin?

Explore more resources for options in WI including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Wisconsin” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data, Accessed April 2026. ⤶

- “Medicare Monthly Enrollment – Wisconsin” Centers for Medicare & Medicaid Services Data. Accessed January, 2025. ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org Dec. 9, 2025 ⤶

- “Medicare Supplement Insurance Policies List 2026” Wisconsin Office of the Commissioner of Insurance. Accessed May 3, 2026 ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Get Medigap Basics” Medicare.gov. Accessed May 3, 2026 ⤶ ⤶

- “Medigap in Wisconsin” Medicare.gov. Accessed May 2, 2026 ⤶

- “Medigap in Wisconsin” Medicare.gov. Accessed Aug. 9, 2023. ⤶

- “2026 Wisconsin SHIP Counselor Toolkit” Wisconsin Department of Health Services. Accessed May 3, 2026 ⤶ ⤶ ⤶ ⤶

- “Medicare Supplement Insurance” Medicare.gov. Accessed May 3, 2026 ⤶

- “2026 Guide to Health Insurance for People with Medicare in Wisconsin” Wisconsin Office of the Commissioner of Insurance. Accessed May 3, 2026 ⤶ ⤶

- “Wisconsin Supplement Insurance (Medigap) Basic Plan policies” Medicare.gov. Accessed May 3, 2026 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. September 26, 2025. ⤶