Find Montana Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Montana Marketplace quick facts

Montana health insurance Marketplace guide

We’ve created this guide, including the FAQs below, to help you understand the health insurance options available to you and your family in Montana. An ACA Marketplace (exchange) plan – or Obamacare – is a good option for people who need to buy their own individual or family health coverage. This includes people who aren’t eligible for Medicaid, Medicare, or an affordable plan offered by an employer.

Montana uses the federally-facilitated Marketplace, which is HealthCare.gov. Three private insurance companies offer coverage in the Montana Health Insurance Marketplace in 2026,4 although one is exiting at the end of 2026 and won’t offer plans for 2027 (see below for details about carrier participation and premiums).

Income-based subsidies are available through the Montana Marketplace: Most enrollees qualify for premium subsidies, and many also qualify for subsidies that reduce out-of-pocket medical costs.5 But as described below, premium subsidies don’t cover as much of enrollees’ total premiums as they did in 2025, and some people lost their subsidies altogether at the end of 2025.

If the Marketplace determines that you or your kids are likely eligible for Medicaid or CHIP (Healthy Montana Kids), they will refer you to Montana Medicaid/CHIP.

Frequently asked questions about health insurance in Montana

Who can buy Marketplace health insurance in Montana?

To enroll in private health coverage through Montana’s Marketplace (HealthCare.gov), you must:6

- Live in Montana and be lawfully present in the United States

- Not be incarcerated

- Not have Medicare coverage

So most people are eligible to enroll in Marketplace coverage. But qualifying for financial assistance (premium subsidies and cost-sharing reductions) is a bit more complex. Eligibility for financial assistance depends on your income, and you must also:

- Not have access to affordable health coverage offered by an employer. If you’re eligible to enroll in an employer-sponsored plan but it seems too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies in the Marketplace.

- Not be eligible for Medicaid or CHIP (Montana Healthy Kids).

- Not be eligible for premium-free Medicare Part A.7

- If married, file a joint tax return with your spouse.8

- Not be able to be claimed by someone else as a tax dependent.8

When can I enroll in an ACA-compliant plan in Montana?

You can sign up for an ACA-compliant individual or family health plan in Montana during the annual open enrollment period. The next open enrollment period will run from November 1 – December 15, 2026, for coverage effective January 1, 2027. This is shorter than the window that was used for the last several years, due to a federal rule change finalized in 2025.

Outside of the open enrollment period, you may still be eligible to enroll or make a plan change if you experience a qualifying life event, such as giving birth or losing other health coverage. American Indians and Alaska Natives can enroll year-round without a qualifying life event.

Enrollment in Montana Medicaid and Healthy Montana Kids (CHIP) is available year-round.9 If you’re eligible for either program, you can enroll anytime.

How do I enroll in a Marketplace plan in Montana?

To enroll in an ACA Marketplace (exchange) plan in Montana, you can:

- Visit HealthCare.gov, which is Montana’s Marketplace (exchange). This platform lets Montana residents comparison shop for health coverage, determine subsidy eligibility, and select the plan that best meets their needs.

- Enroll in Marketplace coverage with the help of an insurance agent or broker, or a Navigator or certified application counselor.

- Enroll via an approved enhanced direct enrollment entity (EDE).10 (EDEs can also offer off-exchange plans and non-ACA-compliant plans, so be sure to specify that you want to enroll in Marketplace/exchange coverage, as that’s the only way to obtain any subsidies for which you might be eligible.)

You can also call HealthCare.gov’s contact center by dialing 1-800-318-2596 (TTY: 1-855-889-4325). The call center is available 24 hours a day, seven days a week, except for holidays.

How can I find affordable health insurance in Montana?

You may find affordable health insurance coverage in Montana by enrolling through HealthCare.gov. This is especially true if you qualify for subsidies, and most enrollees in Montana are subsidy-eligible.

The Affordable Care Act created income-based premium subsidies called Advance Premium Tax Credits (APTC).11 If you’re eligible for APTC, it will reduce the amount you owe in premiums each month – potentially even to $0, depending on your income, age, and the plan you select.

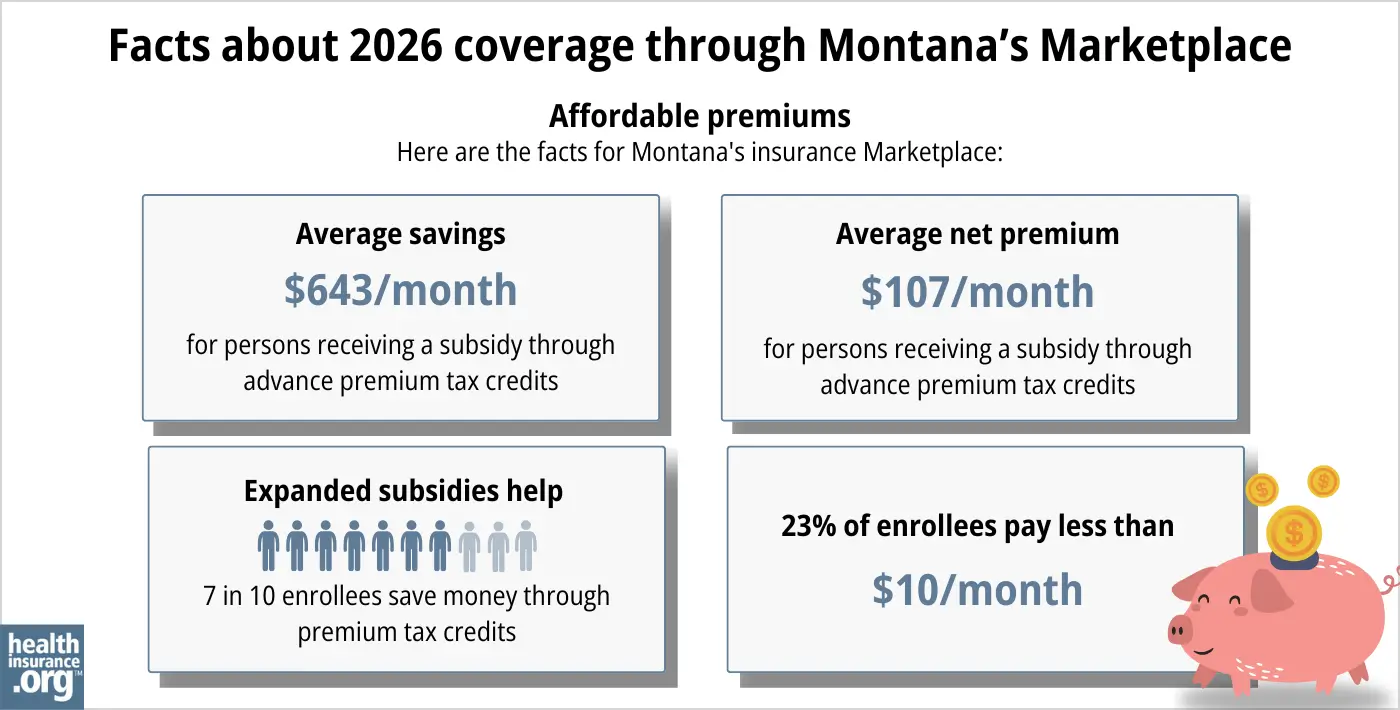

During the open enrollment period for 2026 coverage, nearly eight out of ten Montana Marketplace enrollees were eligible for APTC. These subsidies paid an average of $643/month, reducing the average subsidy-eligible enrollee’s premium to about $107/month.1

But federal subsidy enhancements expired at the end of 2025. Most enrollees still qualify for subsidies (although not as many as in 2025), but after-subsidy premiums are significantly higher as a result of the expiration of the subsidy enhancements.

In addition to premium subsidies, you may also qualify for cost-sharing reductions (CSR) if your household income isn’t more than 250% of the federal poverty level. CSR subsidies will make the deductible and other out-of-pocket expenses (for a Silver-level plan) smaller than they would otherwise be. Twenty-four percent of Montana’s Marketplace enrollees were receiving CSR benefits in 2026.5

You can combine APTC and CSR benefits if you’re eligible for both, as long as you select a Silver-level plan (APTC can be used with plans at any metal level, but CSR benefits are only available on Silver plans).

Source: CMS.gov1

Montana implemented a reinsurance program in 2020, which resulted in overall average rate decreases that year and relatively flat rates the following year.12 So if you’re not eligible for premium subsidies in Montana, the reinsurance program keeps your premiums lower than they would otherwise be.

Depending on your income and circumstances, you may find that you’re eligible for free or low-cost health coverage through Montana Medicaid or Healthy Montana Kids (CHIP). Check to see if you meet the criteria for these programs in Montana.

How many insurers offer Marketplace coverage in Montana?

Three private insurance companies offer Marketplace health insurance coverage in Montana in 2026.13

- BCBS of Montana (Health Care Service Corporation)

- Montana Health CO-OP (one of three ACA-created CO-OPs still operational)

- PacificSource (PacificSource plans will terminate at the end of 2026)

PacificSource has announced that it will no longer offer Marketplace coverage after the end of 2026.14 All PacificSource enrollees will need to select new plans during the open enrollment period for 2027 coverage, which begins November 1, 2026.

Are Marketplace health insurance premiums increasing in Montana?

The following average premium changes were approved for 2026 for the insurers that offer individual/family health insurance in Montana, amounting to a weighted average increase (before subsidies are applied) of 29.1%.15

Montana’s ACA Marketplace Plan 2026 APPROVED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| BCBS of Montana (Health Care Service Corporation, or HCSC) | 24.8% |

| Montana Health CO-OP | 21.7% |

| PacificSource | 11.3% |

Source: Federal rate review database13 and ACA Signups15

Average rate increases are for full-price plans. Most Marketplace enrollees in Montana receive income-based premium tax credits that cover some or all of their monthly premium costs.1

The subsidy amounts change each year. For 2026, they no longer cover as much of enrollees’ total premiums, and are available to fewer people because Congress did not extend the federal subsidy enhancements that expired at the end of 2025. This means Marketplace enrollees in Montana (and throughout the country) are paying significantly higher premiums in 2026.15

For perspective, here’s an overview of how average full-price premiums have changed in Montana’s individual/family health insurance market over the years:

- 2015: Average increase of 3%.16

- 2016: Average increase of 25.9%.17

- 2017: Average increase of 47.6%.18

- 2018: Average increase of 19.5%.19

- 2019: Average increase of 5.7%.20

- 2020: Average decrease of 13.1%.21 (reinsurance program took effect)

- 2021: Average increase of 1.4%.22

- 2022: Average increase of 0.5%.23

- 2023: Average increase of 9.6%.24

- 2024: Average increase of 4.9%25

- 2025: Average increase of 8.3%26

How many people are insured through the Marketplace in Montana?

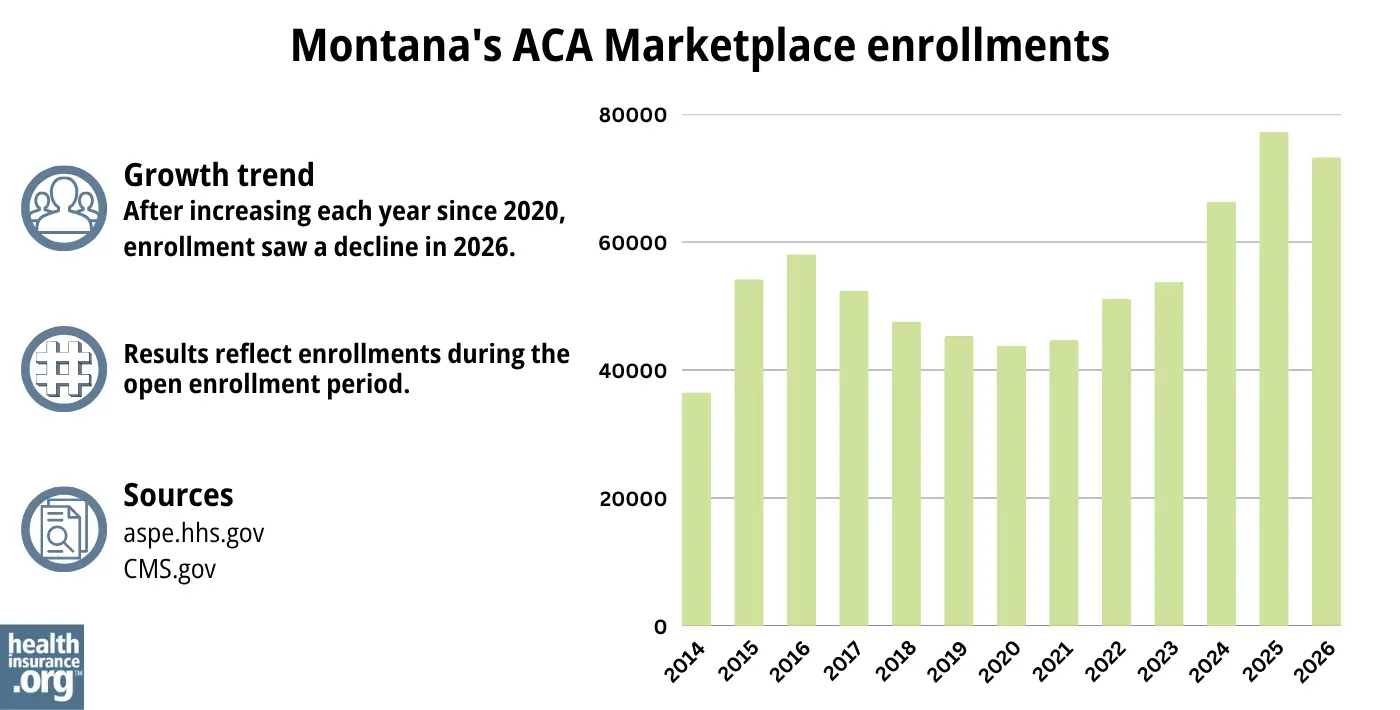

During the open enrollment period for 2026 coverage, 73,255 people enrolled in plans through Montana’s exchange.1 This was down from a record high of 77,221 the year before.27

As shown in the graph below, enrollment had been trending higher for the last several years, before declining in 2026. The previous enrollment increases were driven in large part by the federal subsidy enhancements that were available between 2021 and 2025.

The enrollment spike in 2024 and 2025 was also driven partly by the “unwinding” of the pandemic-era pause on Medicaid disenrollments. For three years during the pandemic, people were not disenrolled from Medicaid even if they were no longer eligible. That ended in the spring of 2023, and some people who were previously enrolled in Medicaid shifted to Marketplace coverage insteat.

Source: 2014,28 2015,29 2016,30 2017,31 2018,32 2019,33 2020,34 2021,35 2022,36 2023,37 2024,38 202527 20261

What health insurance resources are available to Montana residents?

HealthCare.gov

The Marketplace in Montana, where residents can enroll in individual/family health coverage and receive income-based subsidies. You can reach HealthCare.gov at 800-318-2596.

Montana Commissioner of Securities and Insurance

Licenses and regulates health insurance companies, agents, and brokers; can provide assistance to consumers who have questions or complaints about entities the Commissioner regulates.

Montana Primary Care Association

Montana’s federally funded Navigator organization

Montana State Health Insurance Assistance Program

A local service that provides assistance and enrollment counseling for Medicare beneficiaries and their caregivers.

Montana Medicaid and Healthy Montana Kids

(Montana’s Children’s Health Insurance Program)

Looking for more information about other options in your state?

Need help navigating health insurance options in Montana?

Explore more resources for options in MT including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- “Montana Rate Review Submissions” HealthCare.gov, Accessed Sep. 18, 2025 *The above is based on the most current data available. ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” and “Marketplace 2025 Open Enrollment Period Report: National Snapshot” Centers for Medicare & Medicaid Services, April 2026 ⤶

- “Montana Rate Review Submissions” HealthCare.gov, Accessed Dec. 18, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov, Accessed May 27, 2026 ⤶ ⤶

- “A quick guide to the Health Insurance Marketplace®” HealthCare.gov, Accessed Feb. 4, 2026 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Feb. 4, 2026 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Feb. 4, 2026 ⤶ ⤶

- “Montana Medicaid and Healthy Montana Kids (HMK) Plus” Montana.gov, Accessed September 2023 ⤶

- “Entities Approved to Use Enhanced Direct Enrollment” CMS.gov, Dec. 8, 2025 ⤶

- “APTC and CSR Basics” CMS.gov, Oct. 2025 ⤶

- Montana Individual Health Reinsurance. Montana Reinsurance Association. Accessed Feb. 4, 2026 ⤶

- “Montana Rate Review Submissions” HealthCare.gov, Accessed Sep. 18, 2025 ⤶ ⤶

- “PacificSource to exit ACA market, pull out of Montana entirely” Becker’s Payer Issues. May 22, 2026 ⤶

- ”2026 FINAL Gross Rate Changes – Montana: +21.9% (updated)” ACA Signups. Aug. 29, 2025 ⤶ ⤶ ⤶

- Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums. The Commonwealth Fund. December 2014. ⤶

- FINAL PROJECTION: 2016 Weighted Avg. Rate Increases: 12-13% Nationally* ACA Signups. October 2015. ⤶

- Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC). ACA Signups. October 2016. ⤶

- 2018 Rate Hikes. ACA Signups. October 2017. ⤶

- 2019 Rate Hikes. ACA Signups. October 2018. ⤶

- 2020 Rate Changes. ACA Signups. October 2019. ⤶

- 2021 Rate Changes. ACA Signups. October 2020. ⤶

- 2022 Rate Changes. ACA Signups. October 2021. ⤶

- “Montana: Final Avg. Unsubsidized 2023 #ACA Rate Change: +9.6% (Up From +8.9%)” ACASignups.net, Oct. 12, 2022 ⤶

- So How’d I Do On My 2024 Avg. Rate Change Project? Not Bad At All! ACA Signups. December 2023. ⤶

- ”Montana: Preliminary avg. unsubsidized 2025 #ACA rate changes: +8.3%” ACA Signups. Sep. 5, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶ ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, Accessed August 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶