Medicare in Nevada

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Nevada

Medicare enrollment in Nevada

As of February 2026, there were 624,443 people enrolled in Medicare in Nevada.1

Most people become eligible for Medicare enrollment when they turn 65. But younger people are also eligible for Medicare if they’re disabled and have been receiving disability benefits for 24 months. (People with end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS) do not have to wait 24 months for their Medicare coverage to begin.)

In Nevada, about 8% of Medicare beneficiaries (roughly 48,000 people) are younger than 65 and eligible for Medicare due to a disability rather than age.1 Nationwide, about 9% of all Medicare beneficiaries – roughly 6.5 million people – are eligible due to disability.2

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Nevada’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

Medicare Advantage plan availability and enrollment in Nevada

In February 2026, the number of people enrolled in private Medicare plans in Nevada stood at 325,926 people.1 The other 298,507 beneficiaries were enrolled in Original Medicare.1

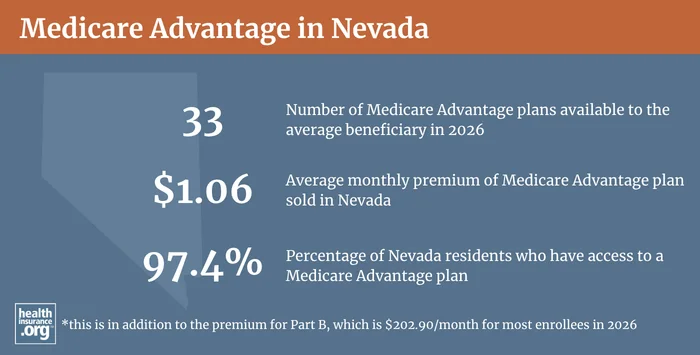

The average Medicare beneficiary in Nevada can choose from among 33 Medicare Advantage plans in 2026. However, eight of Nevada’s 17 counties have no individual Medicare Advantage plans available in 2026. But the other nine counties, where most of the state’s residents live, do have Medicare Advantage plans available.3

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Nevada by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in Nevada

According to AHIP, 99,601 Nevada residents supplemented their Original Medicare coverage with Medigap coverage as of 2023.4

Learn how Medigap plans are regulated and standardized.

Medigap coverage is offered in Nevada by 14 insurers in 2026. All of them use attained age rating,5 which means that enrollees’ monthly premiums increase as they get older, regardless of how old they were when they purchased the policy.6

Nevada’s Medigap birthday rule

Unlike other private Medicare coverage (Medicare Advantage and Medicare Part D plans), federal rules do not provide an annual open enrollment window for Medigap plans. Instead, there’s a one-time six-month window when Medigap coverage is guaranteed-issue. This window starts when a person is at least 65 and enrolled in Medicare Part B (you must be enrolled in both Part A and Part B to buy a Medigap plan). If you apply for a Medigap plan after it ends, federal rules allow insurers to use medical underwriting to determine your eligibility for coverage and your monthly premium.

But Nevada enacted legislation in 2021 that provides Medigap enrollees with an annual “birthday rule” opportunity to switch to a different plan, starting in 2022.7 It ensures that Medigap enrollees in Nevada have a 60-day window – starting the first day of their birthday month – during which they can switch to any other available Medigap plan that has equal or lesser benefits. Medigap plan change applications submitted during this window are guaranteed issue, which means the application cannot be rejected and the insurer cannot increase the premium due to medical history. (“Equal or lesser value” means the plan can be at the same letter level as the one they have, or any of the lower levels, but not a higher level.)

Medigap access for beneficiaries under age 65

Federal rules do not require Medigap insurers to offer coverage to Medicare beneficiaries under the age of 65, so coverage access for this population varies from state to state.

Nevada enacted legislation in 2025 to address this issue.8 Since October 1, 2025, Medigap insurers in Nevada have been required to make all of their policies available to applicants who are under age 65.9 For Medigap Plans A, B, and D, premiums must be the same as the premiums for an enrollee who is 65. For other Medigap plans, premiums can’t exceed 200% of the age-65 rates.10

Nevada offered a one-time enrollment window, from Oct. 1, 2025 to Apr. 1, 2026, so that existing under-65 Medicare beneficiaries could enroll in Medigap coverage.9 Going forward, newly-eligible disabled beneficiaries have the same six-month Medigap enrollment window that exists for people aging into Medicare, allowing them to sign up for guaranteed-issue Medigap during the first six months when they have Medicare Part A and Part B.

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

Medicare Part D plan availability and enrollment in Nevada

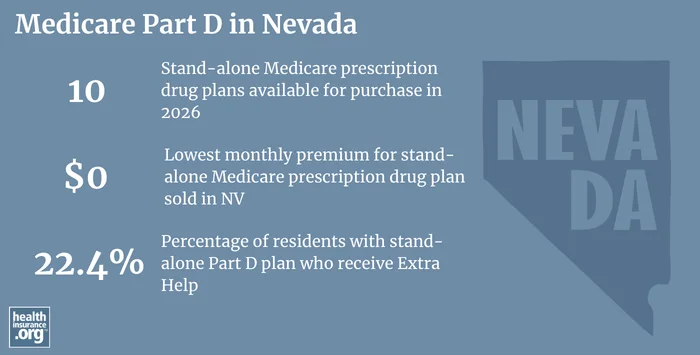

In 2026, there are 10 stand-alone Medicare Part D plans for sale in Nevada, with premiums that start at $0/month.11

As of February 2026, there were 176,959 Medicare beneficiaries in Nevada who were covered under stand-alone Medicare Part D plans.1 Another 307,062 had Part D prescription drug coverage integrated with their Medicare Advantage plans.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Nevada

Questions about Medicare eligibility or enrollment in Nevada?

- You can contact the Nevada State Health Insurance Assistance Program with questions related to Medicare enrollment in Nevada.

- The Nevada Aging and Disability Services Division offers a variety of resources for Nevada Medicare beneficiaries.

- The Governor’s Office for Consumer Health Assistance (OCHA) is part of the Nevada Department of Health and Human Services, and can provide advice, guidance, and information on a variety of health-related issues.

- The Nevada Department of Health and Human Services website also has a resource page with information on programs available to help lower-income Medicare beneficiaries afford their coverage and healthcare.

- The Medicare Rights Center is a national resource that includes a website and a call center where consumers throughout the United States can get answers to a wide range of questions about Medicare.

Looking for more information about other options in your state?

Need help navigating health insurance options in Nevada?

Explore more resources for options in NV including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Nevada” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed, May 2026. ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org. Dec. 9, 2025 ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025. Accessed Oct. 3, 2025 ⤶

- “2026 Medicare Supplement Insurance Premium Comparison Guide” Nevada Division of Insurance. Accessed May 31, 2026 ⤶

- “Choosing a Medigap Policy” Medicare.gov. Accessed Oct. 4, 2025 ⤶

- “Nevada AB250” BillTrack50. Enacted May 28, 2021 ⤶

- “Nevada SB292” BillTrack50. Enacted June 6, 2025 ⤶

- “Bulletin 25-002, Related to; Requiring Medicare Supplement issuers to offer a Medicare Supplement policy for purchase to certain Medicare eligible persons who are below age 65” Nevada Division of Insurance. Sep. 30, 2025 ⤶ ⤶

- ”Nevada Enacts Medigap Expansion Legislation Supported by the American Kidney Fund” American Kidney Fund. June 10, 2025 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶