Medicare in Pennsylvania

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Pennsylvania

Medicare enrollment in Pennsylvania

As of January 2026, there were 3,017,975 Pennsylvania residents enrolled in Medicare.1

For most people, eligibility for Medicare benefits is tied to turning 65. But Medicare eligibility is also triggered when a person has been receiving disability benefits for at least two years. (People with amyotrophic lateral sclerosis (ALS) or end-stage renal disease (ESRD) do not have to wait 24 months for their Medicare enrollment.)

As of early 2026, nearly 10% of Pennsylvania’s Medicare beneficiaries were under 65 and eligible for Medicare due to a disability.1

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Pennsylvania’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

Medicare Advantage plan availability and enrollment in Pennsylvania

As of January 2026, almost 55% of Pennsylvania’s Medicare beneficiaries were enrolled in private Medicare Advantage plans.1 The remaining 1,372,096 Pennsylvania Medicare beneficiaries had Original Medicare.1

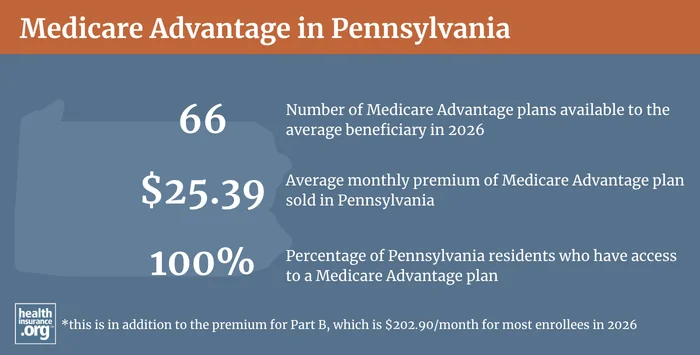

Pennsylvania stands out as having among the most robust Medicare Advantage markets in the country. There are a total of 334 Medicare Advantage plans for sale in Pennsylvania for 2026.2 Plan availability varies by county, but the average Medicare beneficiary in Pennsylvania can choose from among 53 Medicare Advantage plans in 2026, which is the highest of any state in the nation.3

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Learn about Medicare plan options in Pennsylvania by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in Pennsylvania

There are 50 insurers that offer individual Medigap plans in Pennsylvania as of 2026.4 According to data compiled by AHIP, 680,688 Pennsylvania residents had Medigap coverage as of 2023.5

Learn more about how Medigap plans are standardized and what they cover.

There’s no federally guaranteed access to Medigap plans for people under the age of 65 who are eligible for Medicare due to a disability, but Pennsylvania is among the majority of the states that have rules ensuring at least some access to Medigap plans for enrollees who are under the age of 65. In Pennsylvania, the six-month open enrollment window for Medigap plans starts when you’re enrolled in Part B, and it applies regardless of age.6 Pennsylvania state law regarding Medigap plans (Chapter 89, Subchapter K) is available here.

Pennsylvania statute (Title 31, § 89.778) prohibits Medigap insurers from charging higher premiums based on medical history when a person enrolls during their initial six-month enrollment window, so premiums cannot be higher for disabled enrollees (in many states, Medigap coverage is guaranteed-issue for beneficiaries under 65, but premium can be higher; Pennsylvania does not allow this).

Medicare Part D plan availability and enrollment in Pennsylvania

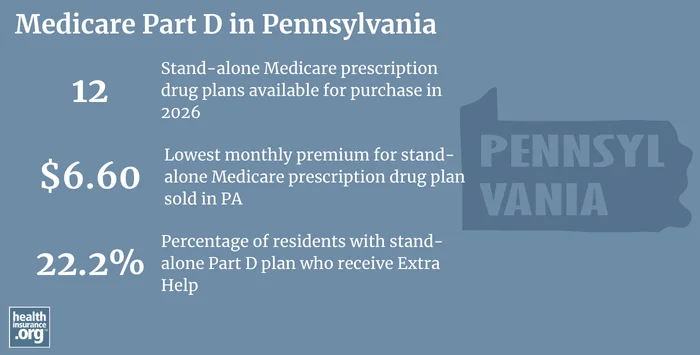

In 2026, there are 12 stand-alone Medicare Part D plans for sale in Pennsylvania, with monthly premiums that start at $6.60.7

As of January 2026, there were 1,086,447 beneficiaries of Medicare in Pennsylvania with stand-alone Part D coverage, and another 1,462,788 had Part D coverage integrated with Medicare Advantage plans.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Resources for Medicare beneficiaries in Pennsylvania

These free resources can help you access and manage your Medicare coverage.

- You can contact APPRISE, Pennsylvania’s State Health Insurance Assistance Program (SHIP), with questions related to Medicare coverage in Pennsylvania. Visit the APPRISE website or call 1-800-783-7067.

- For Medicare beneficiaries with limited income and assets, Pennsylvania Medicaid might be available to help make coverage and care more affordable. You can contact the Pennsylvania Department of Human Services website for more information or call 1-866-550-4355.

- Medicare coverage is regulated by both federal and stage agencies, depending on the type of coverage. The Pennsylvania Insurance Department regulates Medigap plans in the state as well as brokers and agents who sell Medicare coverage, and is a great resource for Pennsylvania residents.

- Visit the Medicare Rights Center. This website provides helpful information geared to Medicare beneficiaries, caregivers, and professionals.

Looking for more information about other options in your state?

Need help navigating health insurance options in Pennsylvania?

Explore more resources for options in PA including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Pennsylvania” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶ ⤶ ⤶ ⤶ ⤶

- “Fact Sheet – Medicare Open Enrollment 2026” Centers for Medicare & Medicaid Services. September 26, 2025. ⤶

- “Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings” KFF.org. Dec. 9, 2025 ⤶

- “Pennsylvania Medicare Supplement Available Plans” PA.gov. Mar. 31, 2026. ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Your Guide to Choosing a Medigap Policy” PA.gov. Accessed Apr. 29, 2026 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025. ⤶