EDITOR'S NOTE: Healthinsurance.org's Curbside Consult is a periodic informal dialogue with medical and health policy experts about pressing issues of the day.

Avik Roy, author of "Transcending Obamacare," left, and Curbside Consult Host Harold Pollack

As I noted in the introduction to my Curbside Consult interview with Avik Roy, his 20,000-word health reform plan - "Transcending Obamacare" - is a serious, though-provoking read. It is unlikely that Republicans will be able to hinder or modify the Affordable Care Act, but Roy's plan is a vision of how conservatives might use the new health insurance marketplaces to take our health care system in in a more conservative direction.

In Part 2 of our interview, our discussion is focused largely on its goal of controlling health care costs. Avik responds to my concern that his plan shifts costs - and in a way that ultimately may increase overall health care spending.

We also talk about how the plan might control costs in certain regions. (Avik says increased provider competition could be the key to reducing healthcare prices ... and that "the left" has given a "free pass to hospitals that charge whatever they want to charge.")

Avik also talks about his disagreement with the idea that health status should never matter for insurance prices. As he notes, ACA allows insurers to charge higher premiums for smokers. I've never been entirely comfortable with these provisions.

Enjoy!

Transcript of Part 2 (of 3):

Controlling prices

Harold: I want to move to the Obamacare. Everything we are talking about with Medicare now is really a revision to Medicare and not a revision to Obamacare. One the downsides is you are not going to reduce overall national health expenditures by raising the Medicare age. What you are really doing is that you are shifting those costs. And in fact, since Medicare pays lower prices than other payers except for Medicaid, you may actually increase overall health care spending ... even though it's not showing up on the federal dime.

There will be a very significant set of challenges if you really executed this. What does that mean for ... say ... the retirement plans of various employers and to individual savings if you have a bunch of middle-class people and above who will not be in the Medicare system and therefore will be paying higher unit prices for their health care as they get into their older years.

Avik: I wish I had a pen and a paper, because there is a lot I would dispute in what you just said. I think a lot of what you said is taken as an article of faith on the left. But I would contest it all pretty vigorously.

So first of all, the point about Medicare paying less than private insurers: It's true that Medicare pays less than traditional employment-based commercial insurance. But when it comes to competition on an exchange where there is enormous competitive pressure to keep premiums low and therefore reimbursements rates low, I think we are likely to see that over time reimbursements rates in the exchange-based market will be quite similar if not lower than Medicare.

And certainly we have a lot of reason to believe they'll be more cost efficient. For example in Medicare Advantage, we know that if you take an apples-to-apples comparison of benefits ... David Cutler and a couple of colleagues at Harvard did a study ... they found that an apples-to-apples comparison of insurance plans between traditional public options/government-run Medicare and comparable benefits in Medicare Advantage Part C, the Medicare Advantage plans were 9 percent less expensive.

I think there is a lot actually that private insurers can bring to the table. I think there has been a lot of kind of intellectual complacency on the left in terms of ... there's this dogma that Medicare is obviously the least expensive approach.

I would agree with you that if Medicare came with it more aggressive price controls and things like that, then you could see a more aggressive reduction in spending relative to the uncontrolled private market. But that isn't what Medicare is today. Medicare has limited ability to affect ... it has some ... but not nearly as much as I think the left would want.

Harold: By the way, I think both left and right would move increasingly to price controls in Medicare one way or another as we start to face the fiscal pressures of it.

Battling hospital monopolies

Avik: I think you may be right. I, certainly ... as a conservative free-market guy ... I don't like price controls. The way I tackle it in the plan is, I say, Look ... if you are going to have hospital monopolies that have effectively infinite pricing power within their regions, you've got to be able to do something to combat that, because the monopoly is already there. It's hard to break up an existing hospital monopoly.

One thing you could do is leverage Medicare's pricing power in that particular region, and I think when I talked to center-left health economists, that is something that people in the center-left are fairly receptive to. It may be more controversial on the right, but I think that's a way of tackling the problem in a more precise way than ... say ... progressives might want which is to say which is, my view, the best way to reduce prices is to have more provider competition. We don't have enough provider competition in this country.

If there are areas in the country where there isn't any provider competition ... for example in heavily rural areas, for example or in heavily consolidated areas where it is not realistic to expect a lot of provider competition ... then you may have to have some regulated approach to address that. I tried in that part of the plan to really ... to bring forward some ideas that may form a basis for some kind of again centrist approach to all this that will look out for the taxpayers ... because again ... as much as the Libertarians ... whom I like and know ... are going to be, you know, their hair is going to be standing on end when I talk about things like that. The way I look at it is: If you have a true market failure ... and I consider a provider monopoly to be a true market failure ...you have a lot of tools you can use that improve that situation like increasing the amount of competition. But, I think, one of the tools in the toolbox has to be that if this is a true monopoly, it needs to be regulated to some degree in the fashion that monopolistic utilities are.

Harold: By the way one of the challenges we also have is that if it's insurers versus providers, insurers just have no public credibility in many of these encounters and ...

A 'free pass' to providers?

Avik: Yeah you know, and that's a real shame because I think private insurers have had some practices that are appropriate to be criticized. But to a large degree, they get demonized for being the ones who are saying "No." Right? So in any health care system ... if you look at Europe, it is the government that gets attacked for that. If there is a very expensive medicine or an expensive treatment that the government says "no" to because it is too expensive, they are the ones that get attacked.

You are going to be attacked being the gatekeeper of a payer, no matter what kind of system you have. And I think one of the great failings of the left in all of this ... to the degree that that the left cares about affordable health coverage for people ... is that they have given a free pass to hospitals that charge whatever they want to charge. And, you talk about CEOs making a lot of money. You know, there are only five big publicly traded for-profit health insurers in America ... but the hospital executives all over America ... the top ten executives all make millions upon millions of dollars, and nobody seems to care about that because they're supposedly nonprofit entities, and that's really an accounting gimmick rather than a real economic analysis of their motives and interests.

Harold: I think one of the visions of ACA is by regulating the insurance side, by regulating medical loss ratio, by having guaranteed issue to that they can't discriminate against the sick, that we create a more legitimate health insurance system that's properly regulated that would have greater credibility to say: "No," sometimes ... especially if there is comparative effectiveness research available to look at some of the practices of providers and to say: "Hey orthopedic surgeons, you are doing way too many surgeries and I'm going to say no to some of these back surgeries that don't seem to be evidence-based."

It seems to me, if you believe in market-oriented solutions to health care, you also have to embrace something like a regulated exchange because in the absence of it, the sort of 'race to the bottom' among insurers and the individual and small-group market that rewards unethical practices or practices that may not be unethical but that American society increasingly rejects.

I think we reject as a society the idea that I am going to turn you away or charge you higher premiums because you have cancer. I think that debate is over. One way or another, we want the system that protects people who have preexisting conditions. But if we create a system that deals with all these problems, then it becomes much more credible to start saying to the providers: "Hey wait a minute. The insurers within this well-regulated system don't think this is a good investment that creates patient value."

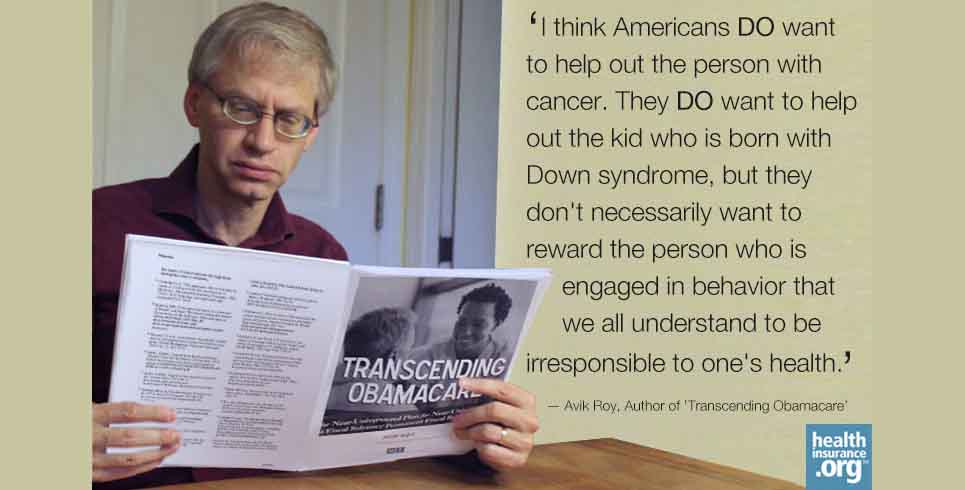

What about the Dorito-eating chain smoker?

Avik: This is a bit of a digression, but I am not sure I agree with you that society has accepted that we should have a society where health status doesn't matter for insurance prices. I actually ... in my plan, I do prohibit health status-based underwriting, so I keep that feature of the ACA. But you know, you brought up the person who has cancer and making sure THAT person has the same health insurance premiums as a perfectly healthy person. That's stacking the deck in terms of the question.

How about if I asked you this question: What about the guy who eats Doritos all day and sits on his couch and smokes ... chain smokes two packs a day? Should I, as a non-smoker who exercises, pay the same health premiums as THAT person? Now, of course the ACA does have a feature for tobacco use specifically ...

Harold: I am not overjoyed by that provision by the way.

Avik: Yeah, I think Americans DO want to help out the person with cancer. They DO want to help out the kid who is born with Down syndrome, but they don't necessarily want to reward the person who is engaged in behavior that we all understand to be irresponsible to one's health. So I think the ethical questions involved and the moral questions involved are a little bit more complicated than you've described.

But having said that, I do agree with your basic premise which is that a regulated exchange is an attractive way to deliver health insurance to those who can't afford it ... either because of their income or their health status. And I do think that is a model that we ought to build on under the right circumstance.

I think, again, this is the attraction of ... this is where Switzerland can point the way, broadly speaking. As you know, I don't agree with everything that Switzerland does, but the general framework of having a regulated exchange where we subsidize on a sliding scale ... on a graduated scale ... the premiums ... the costs of those plans ... I think is an attractive one that can and could achieve the objectives of both the left and the right: the objective of the left to make sure that everyone has the security of health insurance and the objective of the right that that that program is fiscally sustainable in the long term.

Proposal's effect on the generosity of 'metal plans'

Harold: This is Harold Pollack talking to Avik Roy at healthinsurance.org. Let me ask you a few questions about Medicaid and the Obamacare-specific aspects. You would pare back the generosity of health insurance, compared to the current ACA. Your bronze, silver, gold, platinum plans are less ... they cover a lower actuarial value of care than the current ACA envisions. Instead of going up to 400 percent of poverty, as I understand it, your subsidies would go up to 317 percent of the poverty line. You are clearly constricting in some ways ... and it seems to me a lot of the discussion of deregulating these plans, it's not exactly clear to me in all of the detail what you would do to the essential health benefits, but ...

Avik: Let me address that because it is an important topic. I think there has been some confusion particularly among my progressive friends as to how this is structured. The important thing to understand ... there are a couple of important things to understand ... under Obamacare, the way it works is that you have these metal tiers on the exchange. And the subsidy is geared to the second-cheapest silver plan in a particular area.

And so, if you're low-income, you are basically incentivized ... if you qualify for an Obamacare subsidy ... you're incentivized to buy a silver plan because that's basically mostly fully paid for ... or largely paid for ... under the subsidy set-up under Obamacare. This plan is different. In this plan the metal tiers are completely separate from the subsidy structure. The metal tiers are there for consumer friendliness.

Leave the subsidies aside. If you're just someone who needs to buy health coverage for himself and you want to be able to say: Okay here are a bunch of plans. The details of this plan might differ. But I can compare them all because the effective financial value of these plans is the same. Say an actuarial value say of ... let's call it 70 percent or something like that ... So the plans may actually peel that onion in a completely different way. Some may add certain benefits they emphasize over others ... have certain cost-sharing features versus others ... but you know that in general the actuarial value of the plan is the same. That allows consumers to decide what things they actually want health insurers to provide in a plan with a 70 percent actuarial value benefit ... within certain brackets in terms of benefit requirements and guaranteed issue, community rating, and the rest.

Help from HSA subsidies

The tiers under my plan are meant for that purpose, for user-friendliness. The subsidies ... in terms of what kind of plan would you be subsidized for if you're are eligible of subsidies ... the actuarial value or the financial generosity of that subsidy and that benefit is quite comparable to the ACA. The way it is calculated in the plan is you start out with a ... for the average person of average age and average health status ... about a $7,000 deductible and $1,800 dollar HSA subsidy. So remember ... it's average age and average health status. So if you are older and/or sicker, the deductible would be lower,and the HSA subsidy would be larger. That's one element of how this plan would work.

The other thing to understand is that ... so that HSA subsidy ... there's two ways to think about it. One way would be to say, well, just add the HSA subsidy to the deductible so it's a $5,200 dollar deductible. That's one way to think about it. The other way to remember is ... the key thing is that if it were a $5,200 dollar deductible you would be liable for the first $5,200. That is not how the HSA works. The HSA covers the first $1,800 of your expenses. Then you would have the deductible. Then you have the kind of ... what they call in Medicare Part D the gap or the donut hole, and then you have the deductible kick in. The key is this: if you stay healthy over time, that HSA rolls over and so the cumulative actuarial value of the HSA component can be quite significant if you are able to stay healthy and be mindful of all the things that one does to try and stay healthy.

[crosstalk] Harold: So what happens if you have a chronic illness?

Avik: Again another thing to keep in mind is that for low-income people that HSA subsidy would be substantially larger, because the plan takes the cost-sharing subsidies in the ACA and converts those into additional HSA subsidies. So the idea here is actually to take a benefit of comparable actuarial value, comparable financial benefit but turn it into a real nest egg. If you are low income today and you are on subsidized health care under my plan, over time hopefully you can build a real nest egg that can allow you to save. You can pass it down to your kids, you can actually build wealth instead of handing over all of your money to insurance companies ... which is what the ACA does and which is why the insurance companies really love the ACA.

Harold: By the way I should say that the day that ... during the Supreme Court argument when it looked like the ACA might be overturned, Aetna stock jumped by several percent in the moment of awkward argument ... so we can debate what the insurance companies ... the insurance companies have a complicated view of what they like and don't like on the ACA. But it does seem to me ...

Avik: Look at the five-year chart of Aetna, and tell me that investors haven't been happy with Aetna's performance under Obamacare. I think their stock has tripled in that time frame.

Harold: Well, Mazol Tov to them. In terms of healthy people subsidizing the sick, of course what you just described many people would find problematic. If you have Type II diabetes and you have significant health expenses year after year, or you have a mental health problem ... whatever it is ... this structure is much more problematic. Within ACA, you can actually ...

Subsidy and deductible adjustments

Avik: It is only problematic if you don't adjust the core benefit for health status and age. Because the core benefit is adjusted for health status and age, that problem is addressed. That is the key thing to understand is that $7,000 deductible and $1,800 HSA is for the person of average health and average age. If you are somebody who has a high degree of health consumption, as the system gets underway, the subsidies and the deductibles would be adjusted to account for that. So the idea here is to be very careful and very thoughtful so that those individuals are accounted for. The idea here is not to screw over the sick and the elderly. Quite the opposite.

Harold: By the way, this is why ... if this became legislation ... there's one thing I totally disagree with in your thing ... or at least what you say ... Many people criticize the ACA for its length and complexity. The paragraph that you just spoke illustrated why any sensible health reform is going to be pretty lengthy and complex, either in the law or in the Midrash that's sitting on the shelf at the IRS and HHS trying to operationalize what this means.

Avik: And I say that, right I say the sentence you didn't quote, that's right after that sentence, is that my plan will also be complex. And so I don't think it will be as complex as the ACA in the sense that for example the Medicare reform is fairly simple.

I think that the most complicated thing in my plan is not the exchange reforms we just described. It's the Medicaid piece, and not for the reasons that we are talking about, but for the reason that Medicaid is different in every state. Because it is jointly funded by the states and the states have some modest autonomy in the way that they run their programs. Every state is different and every state's population is different. So transitioning from the current gemish of Medicaid into a more rational system, that is the real kind of legislative heavy lifting in terms of how to do that well.

Harold: By the way, there's also the political economy of our three trillion dollar health system, which as you point out ... You and I probably agree on more things than you and I would agree with the typical committee chair who happens to have a wheelchair factory in his district about a bunch of the things that we've been talking about.

Harold Pollack is the Helen Ross Professor at the School of Social Service Administration. He is also Co-Director of The University of Chicago Crime Lab. He has published widely at the interface between poverty policy and public health. Pollack serves as a Fellow at the MacLean Center for Clinical Ethics at the University of Chicago, and as an Adjunct Fellow at the Century Foundation.