Find Connecticut Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Connecticut Health Insurance Marketplace Guide

This guide, including the FAQs below, can help you find the right health plan in Connecticut for you and your family. For many, an Affordable Care Act (ACA) health insurance Marketplace plan, also called Obamacare, can be an affordable and robust coverage solution.

Connecticut runs its own state-based exchange called Access Health CT. Individual and family plans on the ACA Marketplace are offered by two private insurance companies (one of which offers plans under two separate entities),1 for people who don’t have access to Medicaid, Medicare, or employer-sponsored health insurance. This includes:

- Self-employed people

- Early retirees needing coverage until Medicare

- Workers at small businesses without health benefits

Connecticut is among the states where state-funded subsidies are available in addition to federal subsidies. In Connecticut, this is known as the Covered Connecticut program, and it’s available to adults with household incomes up to 175% of the federal poverty level (FPL).2

In addition, Connecticut is spending $70 million to offset some of the reduction in federal subsidies for 2026, which was announced after the U.S. Senate failed to pass a measure that would have extended the federal subsidy enhancements that expired at the end of 2025. Connecticut residents lost about $295 million in federal subsidies due to the expiration of the federal subsidy enhancements, so Connecticut’s state funding makes up only a portion of the lost federal funding. But it kept premiums more affordable than they would otherwise have been.3

(Note that for 2027, Connecticut’s insurers filed rates based on the assumption that the state’s additional subsidies will not be extended.4 But as described below, Connecticut is funding a new program for 2027 to provide additional health insurance subsidies to early childhood educators who get coverage through Access Health CT.)

Access Health CT announced the details of the new state subsidies in early 2026, along with an announcement that open enrollment was being extended until January 31, 2026 to give people more time to enroll in 2026 coverage.5 Connecticut’s 2026 state subsidies:

- fully offset the reduced federal subsidies for enrollees with household income between 100% and 200% of FPL (who aren’t enrolled in Covered Connecticut).

- Offset 50% of the reduction in federal subsidies for enrollees with household income between 400% and 500% of FPL (who are losing all federal subsidies due to the expiration of the federal subsidy enhancements).

Connecticut subsequently announced a special enrollment period, starting February 1, for people eligible for the new state-funded subsidies.6 This special enrollment window continued through June 30, 2026.

Several other states are using their own funds to offset some or all of the reduction in federal premium subsidies for 2026.

Connecticut ACA Marketplace quick facts

Frequently asked questions about health insurance in Connecticut

Who can buy Marketplace health insurance in Connecticut?

To qualify for Marketplace coverage in Connecticut, you must:9

- Live in Connecticut

- Be a U.S. citizen, national, or lawfully present in the U.S.

- Not be incarcerated

- Not be enrolled in Medicare

Although that makes most people in Connecticut eligible to use the Marketplace, eligibility for financial assistance (premium subsidies and cost-sharing reductions) also depends on income. In addition, to be eligible for financial assistance through Access Health CT, you must:

- Not be eligible for employer-sponsored coverage that’s considered affordable and provides minimum value.

- Not be eligible for HUSKY (Medicaid/CHIP)

- Not be eligible for premium-free Medicare Part A.10

- If married, file a joint tax return with your spouse11 (with very limited exceptions)12

- Not be able to be claimed by someone else as a tax dependent.11

When can I enroll in an ACA-compliant plan in Connecticut?

Starting in the fall of 2026, for coverage effective in 2027, open enrollment will end no later than December 31, and all plans selected during open enrollment will take effect January 1.

Outside of open enrollment, you generally need a qualifying life event to enroll or switch policies (examples of qualifying life events are involuntarily losing other coverage, getting married, or moving to an area where different health plans are available). And Connecticut is among several states where pregnancy is considered a qualifying event.13

The qualifying event will trigger a special enrollment period (SEP) that will allow you to sign up for coverage or switch to a different plan.

But some people can sign up without a qualifying life event. For example:

Native Americans can enroll year-round.14

People eligible for the Covered Connecticut program can enroll anytime.15

Anyone eligible for HUSKY (Medicaid/CHIP) in Connecticut can also enroll year-round.

How do I enroll in a Marketplace plan in Connecticut?

There are multiple ways to enroll in an ACA Marketplace plan in Connecticut:16

- Online: Go to AccessHealthCT.com to create an account and apply.

- Phone: Contact the Call Center at 855-805-4325.

- Get help from a navigator, certified application counselor, or agent/broker certified with Access Health CT. These individuals can provide help over the phone, in-person, or online.

How can I find affordable health insurance in Connecticut?

You can find affordable individual and family health plans in Connecticut through AccessHealthCT.com, the state’s ACA exchange.

Access Health CT is where you can:

- Shop, compare, and sign up for health and dental plans

- Qualify for financial help to lower your costs

- Enroll in HUSKY (Medicaid/CHIP) or the Covered Connecticut Program if eligible

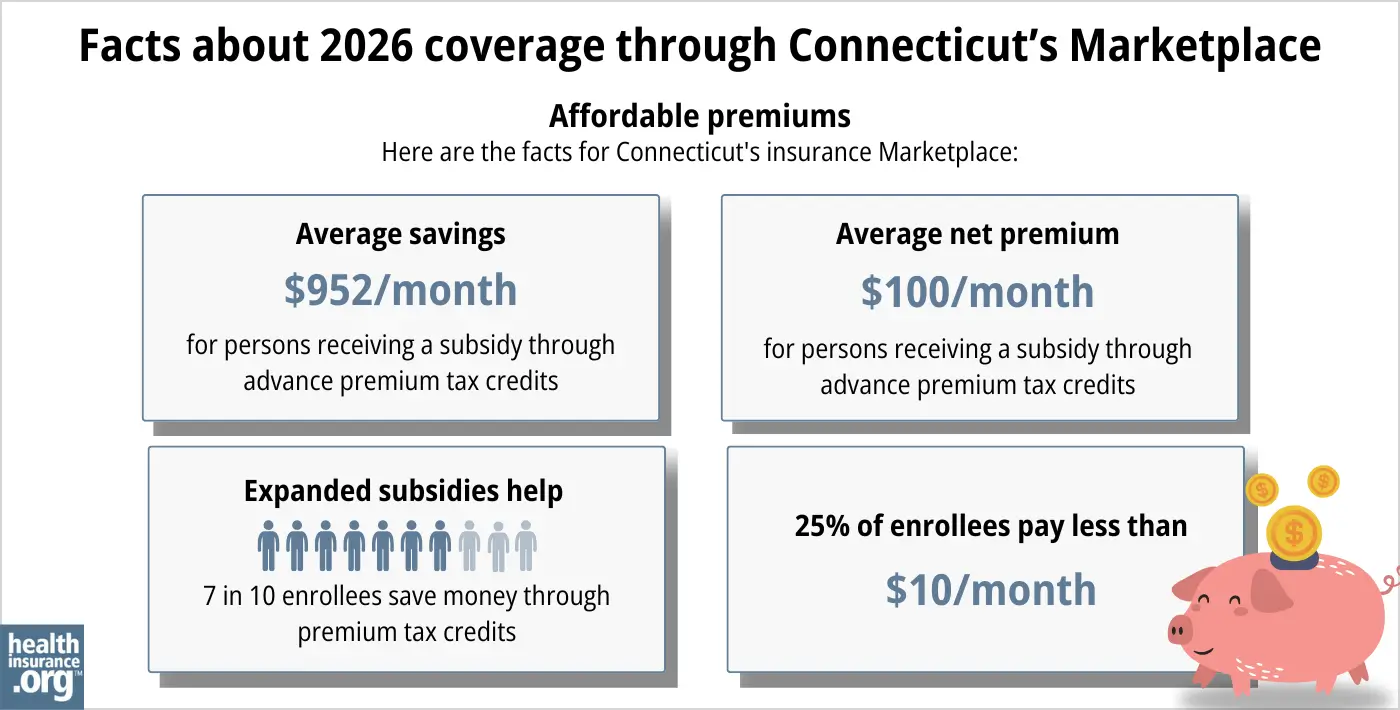

Almost eighty percent of Access Health CT enrollees receive subsidies, saving an average of $952 each month on their 2026 premiums17 (this average only includes federal subsidy amounts; Connecticut’s state-funded subsidies are provided in addition to federal subsidies). These federal subsidies are called Advance Premium Tax Credits (APTC). Subsidy-eligible Connecticut Marketplace enrollees pay an average of $100/month in after-subsidy premiums in 202617 (again, state subsidies are in addition to federal subsidies, so they bring the actual net premium further down).

If your income is no more than 250% of the federal poverty level, you may also qualify for cost-sharing reductions (CSR) to lower your deductibles and out-of-pocket costs,18 although CSR benefits are only available on Silver plans.

If you qualify for Covered Connecticut, the state will cover your portion of the monthly premiums and any expenses related to cost-sharing, such as your deductibles, copays, and co-insurance.

Covered Connecticut is available to enrollees with household income up to 175% of the poverty level (they must also not be eligible for Medicaid, which is available up to 138% of the poverty level).

Under the Covered Connecticut program, eligible enrollees must select a silver plan through Access Health CT and accept all of the federal subsidies available to them. Covered Connecticut then pays any remaining premiums and cost-sharing, resulting in a plan that has a $0 premium and $0 cost-sharing.19

Connecticut is also funding additional state subsidies for 2026, designed to mitigate some of the impact of the expiration of federal subsidy enhancements at the end of 2025.5

Connecticut Marketplace enrollees who are early childhood educators will qualify for a new state-funded health insurance subsidy in 2027 (available when open enrollment begins in the fall of 2026). The program is expected to make coverage more affordable for about 7,200 to 8,800 early childhood educators in the state. The annual subsidy amount (in addition to federal subsidies and Covered Connecticut subsidies) will be $1,000, $1,100, or $1,200, depending on the person’s income,20

Source: CMS.gov17

How many insurers offer Marketplace coverage in Connecticut?

For 2027 coverage, only two insurers will offer individual/family coverage through Access Health CT:

- Anthem

- ConnectiCare Benefits

Three insurance companies offer individual/family coverage through the Connecticut exchange in 2026, but ConnectiCare Insurance Company (which is a separate entity from ConnectiCare Benefits)21 is switching to off-exchange-only for 2027, as opposed to on-exchange-only in 2026.22

ConnectiCare Insurance Company has 3,719 enrollees in 2026, all of whom will need to select new coverage for 2027. They will have the option to switch to one of ConnectiCare Insurance Company’s new off-exchange plans, but subsidies are not available with off-exchange coverage.22

Are Marketplace health insurance premiums increasing in Connecticut?

For 2027, the following average rate increases have been proposed by the insurers that offer individual/family health coverage via Access Health CT,22 amounting to an overall average rate increase of 16.2% before subsidies are applied.23

Connecticut’s ACA Marketplace Plan 2027 PROPOSED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Anthem | 12.8% |

| ConnectiCare Benefits | 22.7% |

| ConnectiCare Insurance Company | Moving off-exchange |

Source: Connecticut Insurance Department22

The proposed rate changes apply to full price premiums, before subsidies are applied. Most enrollees receive subsidies, but those subsidies are no longer available to anyone with a household income over 400% of the federal poverty level. And the subsidies aren’t covering as much of the premium for everyone else, due to the failure of Congress to extend the federal subsidy enhancements that expired at the end of 2025.

Connecticut Gov. Ned Lamont announced in December 2025, soon after the U.S. Senate failed to pass a bill that would have extended the subsidy enhancements, that Connecticut would use $70 million to offset some of the $295 million reduction in federal subsidies for 2026. This helped to keep 2026 net premiums in Connecticut more affordable than they would otherwise have been.3

Access Health CT announced the details of the new state subsidies in early January, 2026. For 2026 coverage, the new state subsidy program:5

- fully covers the reduction in federal subsidies for enrollees with household income between 100% and 200% of FPL (who aren’t enrolled in Covered Connecticut).

- covers 50% of the reduction in federal subsidies for enrollees with household income between 400% and 500% of FPL (the expiration of the federal subsidy enhancements resulted in these enrollees losing all of their federal subsidies).

But the rates that insurers filed for 2027 are based on the assumption that Connecticut’s additional state subsidy program will not be extended into 2027. The insurers noted that if it is, the rates will be adjusted to account for that.23

For perspective, here’s an overview of how average unsubsidized premiums have changed in Connecticut’s individual/family market over the years:

- 2015: Average decrease of 1%.24

- 2016: Average increase of 3.5%.25

- 2017: Average increase of 24.8%.26

- 2018: Average increase of 28.4%.27

- 2019: Average insurance of 2.72%.28

- 2020: Average increase of 3.65%.29

- 2021: Average increase of 0.01%.30

- 2022: Average increase of 5.6%.31

- 2023: Average increase of 12.9%.32

- 2024: Average increase of 9.4%33

- 2025: Average increase of 5.9%34

- 2026: Average increase of 16.8%1

How many people are insured through Connecticut’s Marketplace?

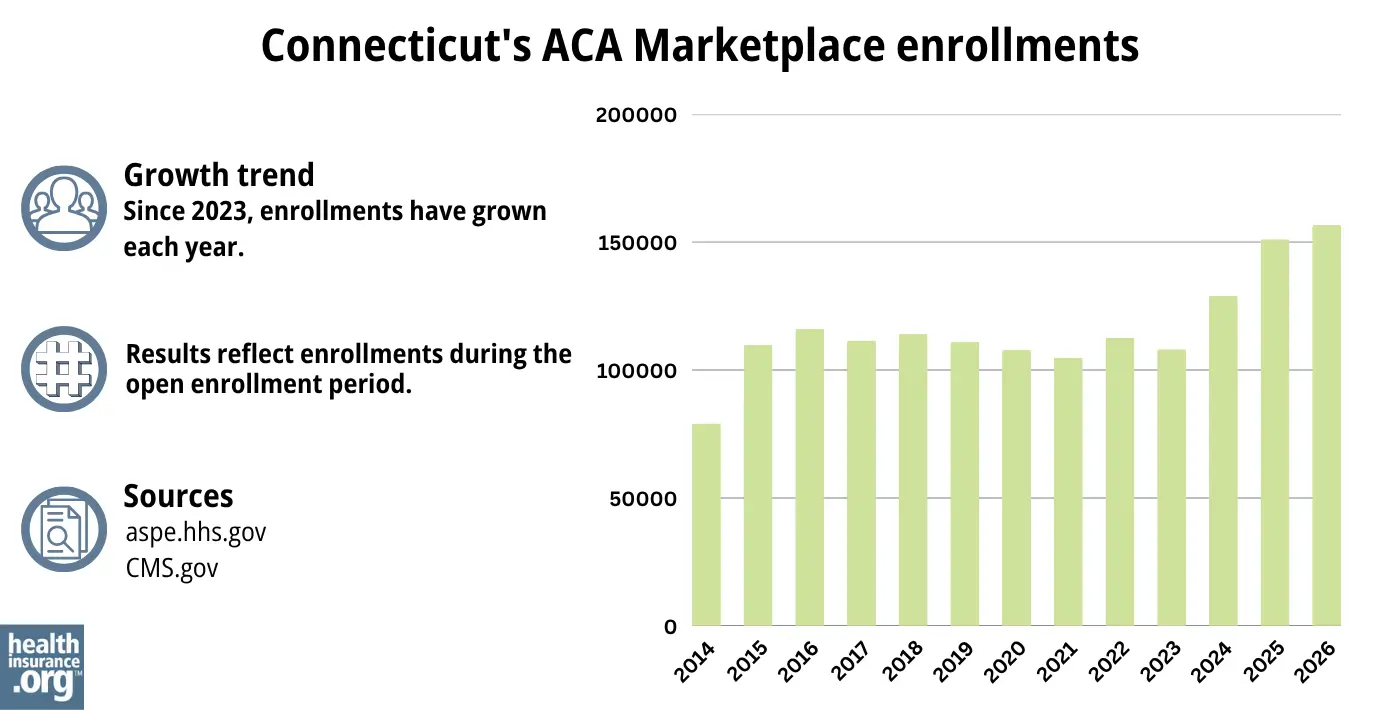

A record-high of more than 156,745 people enrolled in private plans through the Connecticut exchange during the open enrollment period for 2026 coverage.17

The enrollment growth in Connecticut was fairly unique, as most states saw a decrease in enrollment in 2026 due to the expiration of federal subsidy enhancements.

Access Health CT credits the record high enrollment to multiple factors, including increased outreach, encouraging enrollees to work with brokers, and the additional state-funded subsidies that offset some of the reduction in federal subsidies.35

Source: 2014,36 2015,37 2016,38 2017,39 2018,40 2019,41 2020,42 2021,43 2022,44 2023,45 2024,46 202547 202617

What health insurance resources are available to Connecticut residents?

Access Health CT

This website is used by Connecticut residents to sign up for private individual market or small-group coverage and income-based Medicaid/CHIP coverage.

Connecticut CHOICES Program

Offers free enrollment counseling and assistance for older adults, people with disabilities, and their caregivers.

Connecticut Insurance Department

Regulates and licenses the state’s health insurance companies, brokers, and agents. They also address inquiries and complaints from consumers about entities under their regulation.

Husky Healthcare

Provides health coverage for Connecticut residents with lower and moderate incomes.

Medicare Rights Center

This nationwide service offers help and information to Medicare beneficiaries and their caregivers.

Looking for more information about other options in your state?

Need help navigating health insurance options in Connecticut?

Explore more resources for options in CT including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”Health Insurance Rates for 2026” Connecticut Insurance Department. Accessed Aug. 25, 2025 ⤶ ⤶

- Covered Connecticut Program. Access Health CT. Accessed Dec. 14, 2025 ⤶

- ”Lamont pledges $70M for health care after US Senate deadlocks” CT Mirror. Dec. 11, 2025 ⤶ ⤶

- ”Health Insurance Rates for 2027” Connecticut Insurance Department. Accessed June 9, 2026 ⤶

- ”Deadline to Enroll in Health and Dental Coverage Through Access Health CT Has Been Extended to Jan. 31” Access Health CT. Jan. 2, 2026 ⤶ ⤶ ⤶

- ”Access Health CT to Offer Special Enrollment Period for Eligible Customers to Enroll in Coverage with New State Subsidy” Access Health CT. Jan. 23, 2026 ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Health Insurance Rates for 2026” Connecticut Insurance Department. Accessed Aug. 25, 2025 *The above is based on the most current data available. ⤶

- ”What is Access Health CT?” Access Health CT. Accessed Dec. 14, 2025 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Dec. 14, 2025 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Dec. 14, 2025 ⤶ ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- Special Enrollment Periods. Access Health CT. Accessed Dec. 14, 2025 ⤶

- “Who doesn’t need a special enrollment period?“ healthinsurance.org, Accessed August 2023 ⤶

- ”Covered Connecticut Program” Connecticut.gov. Accessed Dec. 14, 2025 ⤶

- “Get Help” Access Health CT, Accessed Dec. 14, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶ ⤶

- “Federal Poverty Level (FPL)” HealthCare.gov, 2023 ⤶

- Covered Connecticut Program. Access Health CT. Accessed November 2023. ⤶

- ”New Health Insurance Subsidy, New Laws, and Summer Food Assistance” State Rep. Kate Farrar, Connecticut House Democrats. June 29, 2026 ⤶

- ”2026 Summary of Companies, Lines of Business, Networks, and Benefit Plans” ConnectiCare. Accessed June 10, 2026 ⤶

- ”Requested Rate Increases Effective 2027” Connecticut Insurance Department. Accessed June, 9, 2026 ⤶ ⤶ ⤶ ⤶

- ”Health Insurance Rates for 2027” Connecticut Insurance Department. Accessed June, 9, 2026 ⤶ ⤶

- Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums. The Commonwealth Fund. December 2014. ⤶

- Connecticut: *Approved* 2016 Weighted Avg. Rate Hikes: +3.5%, -2.9% Sm. Group. ACA Signups. September 2015. ⤶

- Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC). ACA Signups. October 2016. ⤶

- 2018 Rate Hikes. ACA Signups. October 2017. ⤶

- Health Insurance Rates for 2020. Connecticut Insurance Department. September 2018. ⤶

- Health Insurance Rates for 2020. Connecticut Insurance Department. September 2019. ⤶

- Health Insurance Rates for 2021. Connecticut Insurance Department. September 2020. ⤶

- Health Insurance Rates for 2022. Connecticut Insurance Department. September 2021. ⤶

- Many CT health insurance plans will see double-digit rate hikes in 2023. Connecticut Mirror. September 2022. ⤶

- “Health Insurance Rates for 2024” Connecticut Insurance Department, Accessed September 2023 ⤶

- ”Health Insurance Rates for 2025” Connecticut Insurance Department. Sep. 6, 2024 ⤶

- ”Access Health CT Enrolls Record Number of Connecticut Residents in Health Insurance for 2026” Access Health CT. Feb. 19, 2026 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “2023 Marketplace Open Enrollment Period Public Use Files” CMS.gov, March 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶