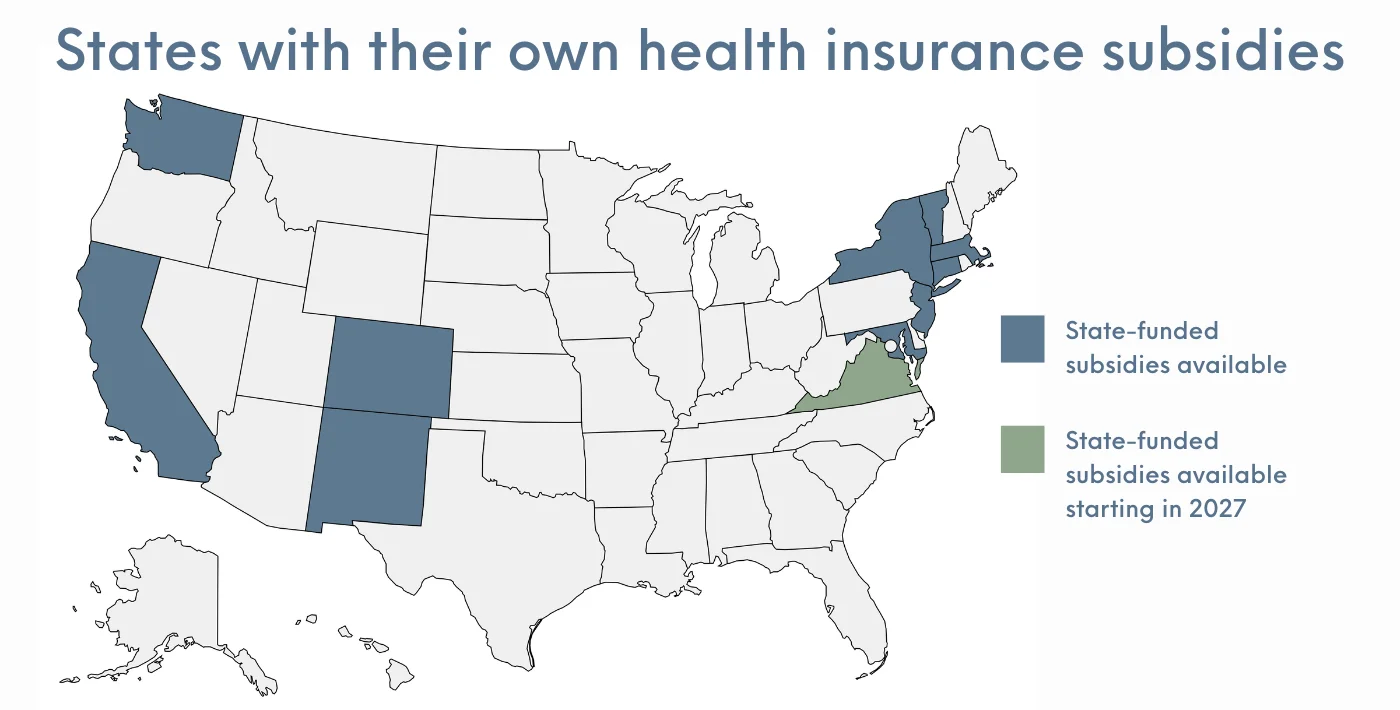

Which states offer their own health insurance subsidies?

In this article

The Affordable Care Act (ACA) created an income-based federal subsidy program for people who buy their own health insurance. In every state, federal premium tax credits (premium subsidies) are available to reduce the amount that most enrollees pay for their coverage, and cost-sharing reductions are available to limit out-of-pocket costs for lower income enrollees.

But several states have created additional state-funded subsidy programs that make coverage and/or medical care even more affordable than it would be with the federal subsidies alone. Eligibility for these programs varies by state, as does the scope of the available subsidies.

As detailed below, some of the states modified or enhanced their subsidy programs for 2026, in an effort to mitigate the impacts of the expiration of the federal subsidy enhancements at the end of 2025. Virginia has added state-funded subsidies that will become available for the 2027 plan year, and some other states are considering the creation of state-funded subsidy programs to address the reduction in federal subsidies.

Which states provide state-funded health insurance subsidies?

Several states have state-funded subsidies available in addition to federal subsidies, with specifics that vary from one state to another:

- For 2026, California allocated $190 million to provide additional state-funded premium subsidies to those with household income up to 150% of the federal poverty level (FPL). However, this offsets only a small portion of the $2.5 billion that California residents lost in 2026 due to the expiration of the federal subsidy enhancements.1

- For 2027, California has increased the funding for the state subsidy program to $300 million.2 The specific details of the 2027 subsidy structure will need to be approved by the Covered California board, but they had previously announced that an increase in funding to $300 million would allow the program to assist enrollees with household income up to 200% of FPL.3

- Prior to 2026, California’s state-funded subsidies were additional cost-sharing reductions.4,5,6

- Starting with the 2026 plan year, Colorado’s state-funded subsidy transitioned to an extra premium subsidy, rather than an extra cost-sharing reduction.7 For 2026 enrollees with household income up to 400% of the federal poverty level, the state is covering $80/month for the primary applicant (on top of their federal premium subsidies), plus an additional $29/month for other applicants on a family policy.8

- Legislation enacted in 2026 extends the state’s additional premium assistance through the end of 2027 (it was previously only funded through the end of 2026),9 and added some additional funding options for the subsidy program.10 But proposed regulations from the Colorado Division of Insurance include a slight reduction in the subsidy amount for the 2027 plan year: $70/month for the primary applicant, plus an additional $25/month for other applicants on a family policy.11

- During a special legislative session in August 2025, Colorado enacted legislation to allocate additional funding for the state subsidy program in 2026 due to the impending expiration of federal subsidy enhancements at the end of 2025.12

- Colorado’s state subsidy program debuted for 2023. Through 2025, it provided additional cost-sharing reductions to eligible applicants, reducing their out-of-pocket costs.13 Enrollees with income up to 200% FPL receive Silver plans with 94% actuarial value (under the ACA, the federal government provides this benefit only to applicants with income up to 150% FPL).

- For 2025 and 2026, Colorado’s state-funded subsidy program is also paying the $1/month premium fee that is charged (after federal subsidies are applied) for all Marketplace plans in Colorado. This fee is required because Colorado plans must cover abortion, and federal rules require a separate $1/month premium for that coverage. Federal rules also prohibit federal subsidies from covering that cost, so state funds are being used instead (people who don’t qualify for any federal premium subsidies must pay this $1/month fee themselves).14

- Colorado also established a new platform (OmniSalud, through Colorado Connect) that undocumented immigrants can use to enroll in coverage, with state-funded premium subsidies for a limited number of enrollees.15 Due to reduced funding, the number of subsidy-eligible spots in this program was reduced to 6,700 for 2026.16

- Via the Covered Connecticut Program, additional premium subsidies and cost-sharing reductions are available to adults with income up to 175% of FPL, as long as they select a Silver plan through the exchange. The state subsidies then pay all of the remaining premiums and cost-sharing that are left after the federal subsidies are applied.17

- In addition to the ongoing Covered Connecticut Program, Connecticut’s governor announced that the state will spend $70 million to offset some of the reduction in federal subsidies for 2026, which was announced after the U.S. Senate failed to pass a measure that would have extended the federal subsidy enhancements that are expiring at the end of 2025.18

- In early January 2026, Connecticut’s health insurance Marketplace announced the details of the new state subsidy program, and also announced an open enrollment extension to January 31, 2026, to give people more time to sign up. State funds are being used to fully offset the reduced federal subsidies for enrollees with household income between 100% and 200% of FPL (who aren’t enrolled in Covered Connecticut). State funds are also being used to offset 50% of the reduction in federal subsidies for enrollees with household income between 400% and 500% of the FPL.19

- Legislation introduced in February 2026 would have added state-funded subsidies for Access Health CT enrollees with income between 500% and 600% of FPL, but the bill did not advance.20

- Covered Connecticut is an ongoing program. But Connecticut’s insurers filed their proposed rates for 2027 based on the assumption that the additional state-funded subsidy program will not continue to be available in 2027.21

- For 2027, Connecticut Marketplace enrollees who are early childhood educators will qualify for a new state-funded health insurance subsidy that’s expected to help about 7,200 to 8,800 early childhood educators in the state. The total annual benefit will be $1,000, $1,100, or $1,200, depending on the person’s income,22 and will be in addition to federal subsidies and regular Covered Connecticut subsidies.

- Maryland previously offered a state subsidy program only for young adults, but broadened that for 2026. The Maryland Premium Assistance program is partially mitigating the impacts of the termination of the federal subsidy enhancements, for enrollees of all ages.23,24 Maryland’s exchange notes that young adults aged 18-37 are still eligible for additional state subsidies.25

- In September 2025, the Maryland Insurance Administration clarified the details about how the state-funded subsidy program would work in 2026 to partially offset the reduction in federal subsidies:26

- It applies to Maryland Health Connection enrollees of all ages (as opposed to the previous Maryland subsidy program, which was only available to adults up to age 37;27 these young adults still qualify for some additional subsidies on top of the broad subsidy program).25

- It fully covers the reduction in federal subsidies for enrollees with household income under 200% of FPL.

- For those with income between 200% and 250% FPL, the benefit phases down from replacing all of the lost federal subsidy amounts to replacing half of it. From 250% to 400% FPL, the state program covers half of the lost federal subsidies.

- Above 400% of FPL, there are no state or federal premium subsidies available.

- The Maryland state premium assistance program is only available for enrollments completed before April 1, 2026. Anyone enrolling in 2026 coverage after that date (via a special enrollment period) will not receive Maryland Premium Assistance.28 Federal subsidies continue to be available regardless of when an enrollment is completed.

- Maryland’s state subsidy program will continue in 2027, but might be scaled back. One of the proposals the state is considering would replace 25% (instead of 50%) of the lost federal subsidy amounts for those with household income above 250% of FPL (and phase the benefit down from fully replacing the lost subsidies to replacing 25%, for those with income between 200% and 250% of FPL).29

- For 2026, to address the reduction in federal subsidies, Massachusetts allocated an additional $250 million to make its existing ConnectorCare state subsidy program more robust. As a result, the state noted that approximately 270,000 ConnectorCare enrollees with income below 400% of FPL would “see little to no premium increases because of the expiring federal credits, while also lowering other out-of-pocket costs like co-pays and deductibles.”30

- Enrollees with incomes up to 400% of FPL are eligible for state premium subsidies and cost-sharing reductions.31

- For 2027, the governor’s budget proposal called for ongoing funding to continue the additional Connector Care subsidies.32

- Before 2024, the income limit for ConnectorCare was 300% of the poverty level. This was increased to 500% in 2024 and 2025.33,34

- The income limit was scheduled to revert to 300% of FPL in 2026, but the Massachusetts 2026 Fiscal Year budget extended the pilot program through 2027, meaning ConnectorCare would continue to extend to 500% FPL.35 However, underlying ConnectorCare rules require the enrollee to also be receiving federal premium subsidies. Since those federal subsidies are not available in 2026 due to the return of the “subsidy cliff,” ConnectorCare subsidies are also not available above 400% of FPL.36

- Enrollees with incomes up to 600% of FPL are eligible for state-based premium subsidies.37 For 2026 coverage, 600% of FPL amounts to a single person earning up to $93,900 or a family of four earning up to $192,900.

- For 2027 coverage, 600% of FPL will amount to $95,760 for a single person, and $198,000 for a family of four.38

- This program is called New Jersey Health Plan Savings.

- New Mexico expanded its existing state-funded subsidy program for 2026, to fully offset the reduction in federal subsidies for 2026.39 This includes assistance for enrollees with household income above 400% of FPL40 and for recent immigrants with income below FPL.41 Both populations lost federal subsidies in 2026 (due to the expiration of federal premium subsidy enhancements and the One Big Beautiful Bill, respectively), so New Mexico’s program was expanded in an effort to ensure these populations can still obtain affordable coverage.

- Plans with cost-sharing reductions in New Mexico are labeled “turquoise.” The state subsidy program is funded by the Health Care Affordability Fund (HCAF).42 Most New Mexico exchange enrollees select Turquoise plans.43

- New Mexico residents are fully insulated from the reduction in federal subsidies, as New Mexico backfilled the entire difference using state funds.44 Although several states offer state-funded subsidies and some have expanded them for 2026, New Mexico is unique in being able to cover the full amount of the federal subsidy reductions for all enrollees.

- New Mexico’s HCAF had indicated in 2025 that it had enough surplus funding to provide additional assistance to enrollees if the federal subsidy enhancements were allowed to expire.42 The state enacted legislation in 2025 to codify the use of the state premium funds to offset the reduction in federal subsidies.45

- Enrollees with household income up to 400% of FPL were already eligible for state-funded premium subsidies, as well as additional cost-sharing reductions (SOPA, or state out-of-pocket assistance). The SOPA benefits expanded in 2025, so that plans with 90% actuarial value (platinum-level coverage) are available to applicants with household income up to 400% of the poverty level (this limit was previously 300%).46

- In March 2026, New Mexico enacted legislation to ensure ongoing funding for the HCAF by increasing the percentage of revenue from the state’s health insurance premium tax that gets sent to the HCAF.47 Currently, 55% of the revenue goes to the affordability fund (the rest goes to the state general fund), and the new legislation will gradually raise that to 95% by 2028.48

- Starting with the 2025 plan year, New York began offering state-funded cost-sharing reductions for Marketplace enrollees with income up to 400% of the federal poverty level, as well as additional cost-sharing reductions for diabetes management and for people who are pregnant or postpartum.49

- New York is continuing the state-funded cost-sharing reduction program in 2026.50,51 New York had clarified that ongoing access to those subsidies in the second half of 2026 would depend on the availability of state funds,52 but an analysis of the plans available via New York State of Health in late July 2026 indicated that the plans with state-funded cost-sharing reductions were still available.53

- Enrollees with incomes up to 300% of FPL are eligible for state-funded premium subsidies and cost-sharing reductions.54 Both stack on top of federal subsidies, and the state-funded cost-sharing reductions extend to a higher income level than federal cost-sharing reductions, which are only available up to 250% of FPL.

Virginia: (new for 2027)

- In the budget that Virginia enacted in 2026, the state allocated $150 million to fund additional health insurance subsidies for Marketplace enrollees with income up to 250% of FPL.5556

- State-based premium subsidies (Cascade Care Savings) are available for enrollees with income up to 250% of FPL, as long as they select a standardized (Cascade Care) Silver or Gold plan through the exchange. Since 2024, undocumented immigrants have been eligible to enroll in coverage through Washington Healthplanfinder and qualify for Cascade Care Savings based on household income.

- Cascade Care Savings are larger for enrollees who aren’t eligible for federal premium subsidies, which includes undocumented immigrants.57

- For 2026, Cascade Care Savings subsidy amounts for those who do qualify for federal subsidies are smaller than they were in 2025 ($55 per member per month, down from $155 per member per month in 2025). But due to the state’s new premium alignment approach (silver loading),58 very affordable Gold plans should be available to enrollees who qualify for federal premium subsidies, even with the smaller Cascade Care Savings and the expiration of the federal subsidy enhancements.57

- For those who don’t qualify for federal premium subsidies in 2026 (but whose income is no more than 250% of FPL) Cascade Care Savings remain at $250 per member per month, the same as they were in 2025.57

- For 2027, the Cascade Care Savings subsidy will depend on household income: For those who are eligible for federal subsidies, there will be one fixed amount for enrollees with household income up to 200% of FPL, and a separate fixed dollar amount for those with household income between 201% and 250% of FPL.59

Will more states start to offer state-funded health insurance subsidies?

Rhode Island is expected to start offering state-funded subsidies for the 2027 plan year. The state enacted a FY 2027 budget bill that includes $19 million to provide supplemental premium subsidies to Marketplace enrollees who earn up to 200% of the federal poverty level.60 But the details of the program had not yet been announced as of June 2026.

A few other states are considering legislation in 2026 that would create a state-funded premium subsidy:

- Illinois lawmakers are considering legislation that calls for the state to allocate $75,000,000 to a state subsidy program that would offset some of the reduction in federal subsidies due to the expiration of the federal subsidy enhancements.61 A separate bill introduced in 2025 and still under consideration in 2026 would add a state tax deduction for individual health insurance premiums, which can be thought of as an indirect subsidy.62

- Pennsylvania is working on a state subsidy program authorized by legislation that the state enacted in 2024.63 But this won’t be available until state funding is allocated,64 which had not yet happened as of 2026.65

Several other states, including Georgia,66 Minnesota,67 Maine,68 Nebraska,69 Iowa,70 Wisconsin,71 Mississippi,72 and Hawaii,73 considered legislation to create state-funded subsidy programs in 2026, but the measures did not advance.

Note: Nebraska, Iowa, Hawaii, and Wisconsin use HealthCare.gov. If any of these states had enacted legislation to create a state-funded subsidy program, the subsidy could only have to be obtained indirectly, either via the state tax return or a separate state-facilitated application program. This is because HealthCare.gov is only set up to provide federal subsidies, and doesn’t have a means of incorporating additional state-funded subsidies.

Which states provide other types of non-subsidy assistance with health coverage?

In addition to the state-funded premium subsidy and cost-sharing subsidy programs described above, some states use other approaches to make affordable health coverage more accessible for their residents.

For example, Minnesota, New York, Oregon, and Washington, DC have Basic Health Programs (BHPs). BHPs are not the same as additional state-funded subsidies, but they provide very comprehensive health coverage, with free or very low premiums, to residents with income up to 200% of FPL.

How can I tell if I’m eligible for state-funded health insurance subsidies?

Just like federal subsidies, eligibility for state-funded subsidies is typically based on how your household income compares with the federal poverty level (FPL). For 2026 coverage, states use 2025 FPL numbers. As noted above, the eligibility limits differ from one state to another, but this chart is a good reference that shows the incomes that correlate with various percentages of the 2025 FPL, depending on family size.

To get federal cost-sharing reductions, you have to select a Silver plan, and that’s also typically true of the state-funded cost-sharing reductions (as noted above, these plans are labeled “turquoise” in New Mexico). In most cases, state-funded premium subsidies can be used for plans at any metal level, although that’s not always the case. (For example, the Covered Connecticut program only applies to Silver-level plans, and it subsidizes both premiums and cost-sharing; Washington’s state-funded subsidies are only available on certain Silver and Gold plans)

If my state offers state-funded health insurance subsidies, can I also get federal ACA subsidies?

Yes, if you’re eligible for federal subsidies, you’ll receive them in addition to the state-funded subsidies. The state-based subsidies described above are designed to work in conjunction with the ACA’s federal subsidies. They provide additional benefits, resulting in lower premiums and/or lower cost-sharing amounts than you would have with just the federal subsidies.

But states can design their subsidy programs so they can be used even by people who aren’t eligible for federal subsidies. Examples are the Colorado and Washington programs that provide state-funded premium subsidies to undocumented immigrants, who are not eligible for federal subsidies.

Where can I get state-funded health insurance subsidies?

As of mid-2026, the states that provide state-funded subsidies all run their own exchange/marketplace platforms. If you’re in a state that offers state-funded health insurance subsidies, you’ll need to obtain your health coverage through the exchange to take advantage of the subsidies.

This is true for both state and federal subsidies, as subsidies are not available for off-exchange plans. (One caveat: Colorado uses a separate platform to provide state-subsidized coverage to a limited number of people who are undocumented immigrants and are thus not eligible to use the exchange.)

How much could I save on health insurance with state subsidies?

The savings from state-funded health insurance subsidies vary considerably from one state to another. In most cases, the exact amount of the savings will vary depending on your income, age, and location. In each of the states that have their own subsidy programs, you can use the state-run exchange’s plan comparison tool to get an anonymous price quote that will include any available state-funded subsidies as well as federal subsidies.

Can I use a state subsidy to pay for Marketplace coverage?

Yes, if you’re in a state that offers state-funded subsidies and you meet the eligibility guidelines. As described above, each state that offers these subsidies has its own rules in terms of income limits and whether the subsidies apply to all Marketplace/exchange plans or only certain plans. (For example, Washington’s state-funded subsidies are only available to offset costs for people who select standardized Silver or Gold plans).

Footnotes

- “Covered California’s Open Enrollment 2026: Here to Help Connect Californians to Care Despite Uncertainty Around Federal Tax Credits” Covered California. Oct. 30, 2025 ⤶

- “California AB109” BillTrack50. Enacted June 29, 2026 ⤶

- “Health and Human Services” California Budget. May 2026 revisions. And “2027 State Premium Subsidy Program Design” Covered California. Accessed June 22, 2026 ⤶

- “Covered California to Launch State-Enhanced Cost-Sharing Reduction Program in 2024 to Improve Health Care Affordability for Enrollees. CoveredCA. July 2023. ⤶

- “Covered California Policy and Action Items” Covered California Board Meeting. May 16, 2024 ⤶

- “Covered California’s Rates and Plans for 2025: The Most Financial Support Ever to Help More Californians Pay for Health Insurance” Covered California. July 24, 2024 ⤶

- “Amended Regulation 4-2-78” Colorado Division of Insurance. Adopted Sep. 29, 2025 ⤶

- “Amended Regulation 4-2-78” Colorado Division of Insurance. Accessed Oct. 7, 2025 ⤶

- “Polis signs bill extending subsidies for Colorado health insurance premiums for another year” Summit Daily. June 3, 2026 ⤶

- “Colorado SB178” BillTrack50. Enacted June 2, 2026 ⤶

- “DRAFT Proposed Amended Regulation 4-2-78” Colorado Division of Insurance. Accessed June 14, 2026 ⤶

- “Colorado HB1006” BillTrack50. Enacted Aug. 28, 2025 ⤶

- “Colorado Health Insurance Affordability Board Meeting Minutes” Colorado Health Insurance Affordability Enterprise. April 19, 2024 ⤶

- “Revised Bulletin No. B-4.148 — Concerning Payments to Carriers Related to Abortion Coverage for On-Exchange Individual Health Plan Enrollees Receiving Subsidies” Colorado Division of Insurance. Oct. 22, 2025 ⤶

- “OmniSalud” Connect for Health Colorado. Accessed Aug. 26, 2025 ⤶

- “SilverEnhanced Savings” Connect for Health Colorado. Accessed Jan. 5, 2026 ⤶

- “Covered Connecticut Program” Connecticut Social Services. Accessed Jan. 5, 2026 ⤶

- “Lamont pledges $70M for health care after US Senate deadlocks” CT Mirror. Dec. 11, 2025 ⤶

- “Deadline to Enroll in Health and Dental Coverage Through Access Health CT Has Been Extended to Jan. 31” Access Health CT. Jan. 2, 2026 ⤶

- “Connecticut SB3” BillTrack50. Legislation died May 2026 ⤶

- “Health Insurance Rates for 2027” Connecticut Insurance Department. Accessed June 22, 2026 ⤶

- “New Health Insurance Subsidy, New Laws, and Summer Food Assistance” State Rep. Kate Farrar, Connecticut House Democrats. June 29, 2026 ⤶

- “Maryland HB1082” BillTrack50. Enacted May 13, 2025 ⤶

- “2026 State-Based Subsidy: Program Parameters Discussion and Proposed and Emergency Regulations” Maryland Health Benefit Exchange. May 19, 2025. And “Standing Advisory Committee Meeting” MHBE Policy Department, Maryland Health Benefit Exchange, July 17, 2025 ⤶

- “Maryland Premium Assistance” Maryland Health Connection. Accessed Jan. 5, 2026 ⤶ ⤶

- “Maryland Insurance Administration Approves 2026 Affordable Care Act Premium Rates” Maryland Insurance Administration. Sep. 19, 2025 ⤶

- “Report on the Young Adult Subsidy Program” Maryland Health Benefit Exchange. Dec. 18, 2024. And Maryland SB601, Maryland HB814, and Maryland HB297. BillTrack50. Accessed Jan. 5, 2026 ⤶

- “Changes Coming to Health Care in Maryland” Maryland Health Connection. Accessed May 3, 2026 ⤶

- “2027 Proposed State Subsidy and Estimated Reinsurance Parameters” Maryland Health Benefit Exchange. Apr. 20, 2026 ⤶

- “Governor Healey Details Strongest Plan in the Country to Protect Against President Trump’s ACA Cost Hikes” Massachusetts Health Connector. Jan. 8, 2026 ⤶

- “ConnectorCare Overview” Massachusetts Health Connector. Accessed Jan. 8, 2026 ⤶

- “Governor Healey Files Fiscal Year 2027 Budget That Controls Spending, Prioritizes Affordability and Continues Transformative Investments in Education, Transportation” Mass.gov. Jan. 28, 2026 ⤶

- “Massachusetts Expands Access to Affordable Health Care” Massachusetts Health Connector. Accessed January 2024. ⤶

- “ConnectorCare Health Plans” Massachusetts Health Connector. Accessed Apr. 11, 2025 ⤶

- “Governor Healey Signs $60.9 Billion Fiscal Year 2026 Budget” Mass.gov. July 4, 2025. And “Health Connector 500% FPL Connector Care Pilot Extension 3” Governor’s Budget FY2026 Recommendation. Accessed June 22, 2026 ⤶

- “Preliminary Eligibility: What does it mean and what do you need to do?” Massachusetts Health Connector. Sep. 2025 ⤶

- “Lower Your Monthly Premiums with the NJ Health Plan Savings” GetCoveredNJ. Accessed Apr. 11, 2025 ⤶

- “2026 Poverty Guidelines” United States Department of Health & Human Services. Accessed June 22, 2026 ⤶

- “New Mexico’s amazing emergency ACA policies take it ANOTHER step further...” ACA Signups. Dec. 2, 2025 ⤶

- “Addendum #1 to the New Mexico Health Insurance Marketplace Affordability Program Policy and Procedures Manual for the 2026 Plan Year” New Mexico Health Care Authority. Accessed Dec. 12, 2025 ⤶

- “Addendum #2 to the New Mexico Health Insurance Marketplace Affordability Program Policy and Procedure Manual for the 2026 Plan Year” New Mexico Health Care Authority. Accessed Dec. 12, 2025 ⤶

- “The Health Care Affordability Fund” New Mexico Legislative Finance Committee. June 25, 2025 ⤶ ⤶

- “New Mexico Open Enrollment 2026 Level of Coverage Summary” BeWellnm. Accessed Mar. 10, 2026 ⤶

- “New Federal Changes” BeWell New Mexico’s Health Insurance Marketplace. Accessed Dec. 12, 2025 ⤶

- “New Mexico HB2” BillTrack50. Enacted Oct. 3, 2025 ⤶

- “2025 Plan Year Health Insurance Marketplace Affordability Program, Policy and Procedures Manual” New Mexico Office of the Superintendent of Insurance. April 26, 2024 ⤶

- “Affordable health coverage bill headed to Governor’s desk” New Mexico Health Care Authority. Feb. 16, 2026 ⤶

- “New Mexico HB4” BillTrack50. Enacted Mar. 6, 2026 ⤶

- “Section 1332: State Innovation Waivers, New York” and “Letter from New York to CMS” CMS.gov. June 28, 2024. And “State Health Department’s NY State of Health Announces Approval of State’s Innovation Waiver Amendment In Time for 2025 Enrollment Period” New York State Department of Health. Oct. 2, 2024 ⤶

- “Attachment U: 2026 Cost Sharing Reduction Initiatives” New York State of Health. Accessed July 28, 2026 ⤶

- “Extra Cost-Savings Through NY State of Health” NY State of Health. Accessed Jan. 5, 2026 ⤶

- “2026 Qualified Health Plan and Essential Plan Line Up” New York State of Health. Oct. 29, 2025 ⤶

- "NY State of Health, Get an Estimate" NY State of Health. Accessed July 28, 2026 ⤶

- “33 V.S.A. § 1812” Vermont General Assembly. Accessed Nov. 15, 2025 ⤶

- "Dropped your ACA insurance due to spiking premiums? You could qualify for a state subsidy this fall" Virginia Mercury. July 8, 2026 ⤶

- “Virginia HB30” BillTrack50. And “Budget Amendments - HB30 (Conference Report)” Virginia.gov. BillTrack50. Passed Mar. 4, 2026 ⤶

- “Final Cascade Care Savings amounts for plan year 2026 released” Washington Health Benefit Exchange. Sep. 30, 2025 ⤶ ⤶ ⤶

- “Washington State also jumps on the Premium Alignment bandwagon to mitigate tax credit expiration” ACA Signups. Sep. 15, 2025 ⤶

- “Cascade Care Savings” and “State Premium Assistance Policy, Effective for Coverage Beginning January 1, 2027” Washington Health Benefit Exchange. Accessed June 22, 2026 ⤶

- “Governor McKee Highlights Affordability for All Proposal to Make HealthSource RI Coverage More Affordable” State of Rhode Island, Governor Dan McKee. June 12, 2026 ⤶

- “Illinois SB2794” BillTrack50. In committee Feb. 3, 2026 ⤶

- “Illinois HB3737” BillTrack50. In committee Mar. 21, 2025 ⤶

- “Pennie Board of Directors Strategic Planning Session” (pages 27-30). Pennie Board of Directors. February 22, 2024, AND “Pennie Board of Directors Meeting” Pennie.com. May 16, 2024 ⤶

- “Pennie Board of Directors Meeting, March 2025” Pennie. Mar. 12, 2025 ⤶

- “Pennie Board of Director Meeting” Pennie. Feb. 2026 ⤶

- “Georgia SB379” BillTrack50. Died Apr. 2, 2026 ⤶

- “Minnesota HF2506” and “Minnesota SB1024” and “Minnesota SB722” BillTrack50. Died May 18, 2026 ⤶

- “Maine LD2208” BillTrack50. Died Apr. 29, 2026 ⤶

- “Nebraska LB931” BillTrack50. Died Apr. 17, 2026 ⤶

- “Iowa HF2738” BillTrack50. Died May 3, 2026 ⤶

- “Wisconsin SB1091” BillTrack50. Died Mar. 23, 2026 ⤶

- “Mississippi HB590” BillTrack50. Died Feb. 3, 2026 ⤶

- “Hawaii SB2087” and “Hawaii HB1546” BillTrack50. Died May 8, 2026 ⤶