self-insured health plan

A self-insured health plan (also known as a self-funded health plan) is coverage offered by an employer or association in which the employer (or association) takes on the risk involved with providing coverage, instead of purchasing coverage from an insurance company.What is a self-insured health plan?

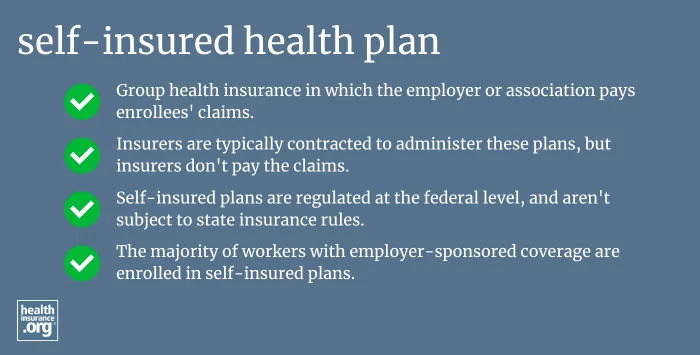

Self-insured coverage means that the employer or association pays for enrollees’ medical care directly. Fully insured coverage means that health insurance is being purchased from an insurance company (either by an employer or by an individual) and the insurance company will be the entity responsible for paying for medical care. Self-insured health plans can be administered by the employer or association, but it’s common for a third-party administrator (TPA) to be used. The TPA is often a commercial insurance carrier, so the employees’ ID cards might have the name of an insurance carrier on them, and the plan might use that insurer’s provider network. But a TPA is only administering the plan; the employer is still taking on all of the financial risk and covering the cost of employees’ claims.What is the difference between self-insured coverage and fully insured coverage?

According to a 2025 KFF analysis, 67% of workers with employer-sponsored health insurance are in plans that are self-funded, including 80% of covered workers at large companies.1 So if you have employer-sponsored health insurance, and particularly if you work for a large employer, it’s likely that your coverage is self-insured.How common is self-insured coverage?

Self-insured health plans are not subject to state insurance regulations. Instead, they’re regulated at the federal level, under ERISA. So for example, if a state requires health plans to cover services like bariatric surgery or infertility treatment, those requirements would not apply to self-funded health plans. Self-insured plans are, however, subject to various aspects of several federal laws, including the ACA, COBRA, HIPAA, and the No Surprises Act. Part of the reason the No Surprises Act was needed was that self-insured plans were not subject to state laws designed to protect consumers from “surprise” balance billing, so federal legislation was needed even though numerous states had addressed that issue for state-regulated health plans. Surprise balance billing occurs when a person receives out-of-network care during an emergency, or receives care from an out-of-network provider while at an in-network hospital. The No Surprises Act applies nationwide, to both self-insured and fully-insured health plans.How are self-insured health plans regulated?

Footnotes

- “Employer Health Benefits, 2025 Annual Survey” KFF. Oct. 22, 2025 ⤶