Find Utah Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Utah Marketplace quick facts

Utah health insurance Marketplace guide

If you need health insurance in Utah, this guide, including the FAQs below, is for you. You may find that an Affordable Care Act (ACA) Marketplace plan – commonly referred to as an Obamacare plan or an exchange plan – may be an affordable choice.

In Utah, the exchange (Marketplace) is operated at the federal level, meaning individuals and families enroll in health plans through HealthCare.gov or authorized enhanced direct enrollment entities.4

For 2026, six insurers offer Marketplace coverage in Utah, with varying coverage areas:5 This is down from seven in 2025; see below for details about insurer participation and premium changes for 2026.

The Marketplace serves individuals and families who need to purchase their own health insurance. This includes self-employed individuals, people who have retired early and are not yet eligible for Medicare, and employees of small businesses that do not provide health benefits. Enrolling in a plan on the exchange is the only way Utah residents can access financial assistance for their individual market plan coverage.

Frequently asked questions about health insurance in Utah

Who can buy Marketplace health insurance in Utah?

Most people in Utah can buy health insurance through the exchange. Marketplace health coverage is available if you meet the following criteria:6

- You must be a resident of Utah.

- You must be lawfully present in the U.S.

- You can’t be incarcerated.

- You must not be enrolled in Medicare.

Whether or not you qualify for financial assistance with your premium, deductible, or out-of-pocket costs depends on your income and how it compares with the cost of the second-lowest-cost Silver plan in your area.

Additionally, to qualify for financial assistance, you must:

- Not have access to affordable health coverage through an employer. If you think your employer-sponsored health plan is too expensive, use our Employer Health Plan Affordability Calculator to check if you qualify for premium subsidies in the Marketplace.

- Not be eligible for Medicaid or CHIP in Utah, or for premium-free Medicare Part A.7

- If married, file a joint tax return.8

- Not be able to be claimed by someone else as a tax dependent.8

When can I enroll in an ACA-compliant plan in Utah?

In Utah, the open enrollment window to sign up for ACA Marketplace individual and family health plans runs from November 1 to January 15.9

For coverage to start on January 1, enroll by December 15. Enrolling between December 16 and January 15 will push your coverage start date to February 1.

But starting in the fall of 2026, due to a federal regulation finalized in 2025, the open enrollment period will be shorter. In Utah, the open enrollment window will run from November 1 to December 15, and all plans selected during open enrollment will take effect January 1.

Outside of open enrollment, you can only sign up for coverage (through the exchange or directly through an insurance company) if you have a special enrollment period (SEP). In most cases, this means you need to have a qualifying life event. But American Indians and Alaska Natives can enroll at any time.

How do I enroll in a Marketplace plan in Utah?

You have a few ways to enroll in a Marketplace health plan in Utah:

- Online: Go to HealthCare.gov. This is the federal Marketplace website that also lets you shop around for plans. You can also enroll in a Utah Marketplace plan via an EDE entity approved to offer coverage in Utah.10

- By Phone: Call 1-800-318-2596 (TTY: 1-855-889-4325) to talk to a representative over the phone. The call center is available 24 hours a day, seven days a week, except holidays.

- In-person: Get help from a licensed insurance agent, navigator, or certified application counselor in your area. Look for assistance at localhelp.HealthCare.gov. Call 2-1-1 or visit takecareutah.org.

No matter which of the above methods you use, you’ll still purchase your health plan through HealthCare.gov (or an approved EDE) since Utah uses the federally-facilitated Marketplace. The website will walk you through the application process and determine your eligibility for financial assistance.

How can I find affordable health insurance in Utah?

People in Utah who enroll in a Marketplace plan (accessed at HealthCare.gov) can be eligible for two different types of financial assistance, depending on their household income:

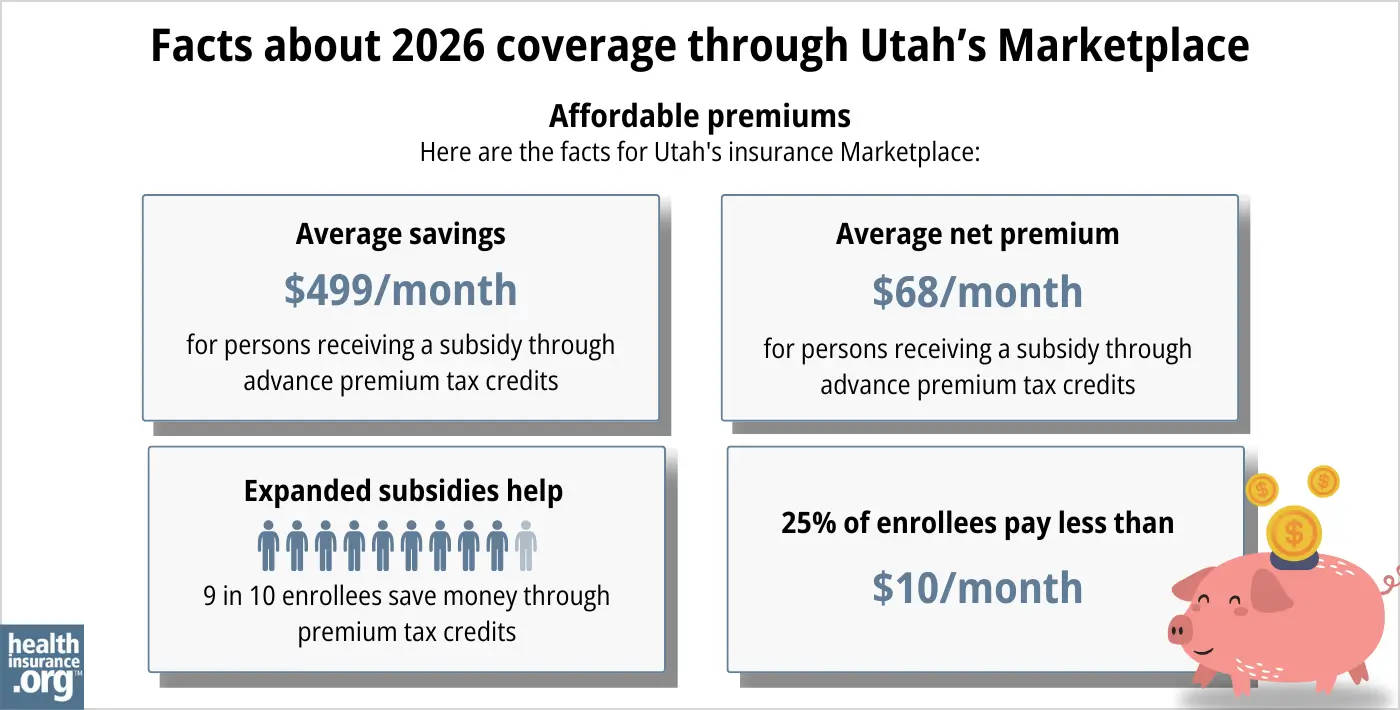

- Premium tax credits (premium subsidies): If you sign up on HealthCare.gov, you may qualify for financial assistance called Advance Premium Tax Credits (APTC) to lower your monthly premiums. Of the people who enrolled through the Utah Marketplace during the open enrollment period for 2026 coverage, nearly 90% qualified for APTC. The average APTC amount was $499/month. For subsidy-eligible enrollees, this reduced the average net premium to just $68/month.1

- Cost-sharing reductions (CSR): If your household income is no more than 250% of the federal poverty level, you can also receive cost-sharing reductions (CSR) assistance, as long as you select a Silver-level plan. CSRs reduce your deductible and out-of-pocket expenses, which means you can get the care you need at an affordable cost.

Source: CMS.gov1

Medicaid: Check if you’re eligible for Medicaid by going online to HealthCare.gov or through medicaid.utah.gov.11

How many insurers offer Marketplace coverage in Utah?

For 2026, six insurers offer Marketplace coverage in Utah, with varying coverage areas:5

- BridgeSpan Health Company

- Regence BlueCross BlueShield of Utah

- SelectHealth

- University of Utah Health Plans

- Imperial Health Plan of the Southwest

- Molina Healthcare of Utah

This is down from seven in 2025,12 as Aetna is exiting the individual market (nationwide) at the end of 2025. In addition, Molina is exiting most of the counties where it offers coverage in Utah in 2025, and will only continue to offer coverage in two southwest Utah counties.13

Utah Marketplace enrollees whose carrier is exiting the market in their area will need to select a plan from a different insurer during the open enrollment period for 2026 coverage.

Are Marketplace health insurance premiums increasing in Utah?

The following average rate changes were approved for 2026 for Utah’s Marketplace insurers,14 amounting to a weighted average premium increase of 14.2%15 (calculated before subsidies are applied).

Utah’s ACA Marketplace Plan 2026 APPROVED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| BridgeSpan Health Company | 15% |

| Molina Healthcare of Utah | 32.1% |

| Regence BlueCross BlueShield of Utah | 15.4% |

| SelectHealth | 12.8% |

| University of Utah Health Plans | 17.6% |

| Imperial Health Plan of the Southwest | 14.2% |

| Aetna Health of Utah | Exiting market |

Source: Federal Rate Review Database16 and Utah Insurance Department17

Although the weighted average premium increase is about 14% for 2026,15 it’s important to understand that this only applies to full-price premiums. Most enrollees qualify for premium subsidies, and thus don’t pay full price. But if Congress doesn’t extend the federal subsidy enhancements that have been in effect since 2021, they will expire at the end of 2025. If that happens, after-subsidy premiums will increase significantly in 2026, and some people will lose their subsidies altogether. (As of mid-December 2025, Congress had not extended these subsidy enhancements and it appeared very likely they would expire at the end of 2025.)

For perspective, here’s how average full-price premiums have changed in Utah’s individual/family market in previous years:

- 2015: Average increase of 5%18

- 2016: Average increase of 25%19

- 2017: Average increase of 31.7%20

- 2018: Average increase of 39.5%21

- 2019: Average increase of 0.5%22

- 2020: Average decrease of 2.3%%23

- 2021: Average rate changes ranged from -7% to +3%24

- 2022: Average increase of 1%25

- 2023: Average increase of 6%26

- 2024: Average increase of 11.4%27

- 2025: Average increase of 10.4%28

How many people are insured through Utah’s Marketplace?

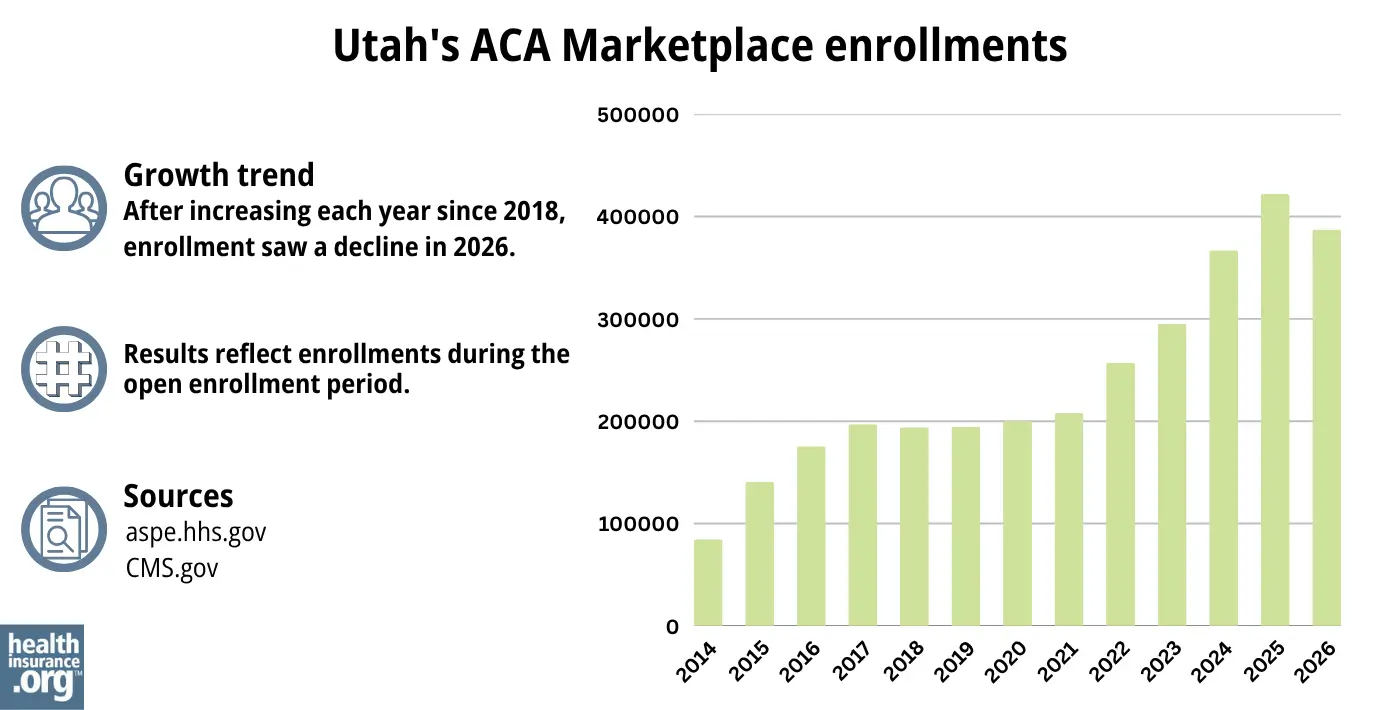

During the open enrollment period for 2026 coverage, 387,336 people enrolled in private plans through Utah’s health insurance Marketplace.1

This was a new record high, on the heels of several consecutive years of record high enrollment. The graph below shows enrollment over time in Utah’s exchange. The sharp increase in enrollment in recent years has been driven in large part by the subsidy enhancements under the American Rescue Plan and Inflation Reduction Act, which made Marketplace plans more affordable. The enrollment increases for 2024 and 2025 were also partially driven by Medicaid disenrollments, which resumed in 2023. Some people who are no longer eligible for Medicaid have obtained coverage in the Marketplace instead.

Source: 2014,29 2015,30 2016,31 2017,32 2018,33 2019,34 2020,35 2021,36 2022,37 2023,38 2024,39 202540 20261

What health insurance resources are available to Utah residents?

HealthCare.gov

The official federal website where you can sign up for health insurance plans through the ACA Marketplace.

Utah Insurance Department

Oversees and licenses health insurance companies, brokers, and agents, offering information and help for various health insurance concerns.

Utah Health Insurance Transparency; Latest Rate Changes

Shows rate and plan filings that insurers have submitted for review by state regulators.

Utah Senior Services

Supports Medicare beneficiaries by providing assistance, information, and valuable resources.

Take Care Utah

An initiative aimed at helping Utah residents understand and access health insurance options, including the ACA Marketplace and Medicaid.

Looking for more information about other options in your state?

Need help navigating health insurance options in Utah?

Explore more resources for options in UT including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶ ⤶

- ”Latest Rate Changes” Utah Health Insurance Transparency. Accessed Sep. 22, 2025 *The above is based on the most current data available. ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” and “Marketplace 2025 Open Enrollment Period Report: National Snapshot” Centers for Medicare & Medicaid Services, April 2026 ⤶

- “Entities Approved to be Used Enhanced Direct Enrollment” Centers for Medicare and Medicaid Services. Aug. 9, 2024 ⤶

- ”Latest Rate Changes” Utah Health Insurance Transparency. Accessed Sep. 22, 2025 ⤶ ⤶

- “A quick guide to the Health Insurance Marketplace” HealthCare.gov, Accessed September 2023 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Dec. 16, 2025 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Dec. 16, 2025 ⤶ ⤶

- “When can you get health insurance?” HealthCare.gov, 2023 ⤶

- ”Entities Approved to Use Enhanced Direct Enrollment” Centers for Medicare & Medicaid Services. Aug. 9, 2024 ⤶

- “Utah Medicaid” Utah Department of Health and Human Services, medicaid.utah.gov, Accessed September 2023 ⤶

- ”2025 Insurers” Utah Insurance Department. Accessed Dec. 4, 2024 ⤶

- ”Breaking News – Molina Healthcare Announces Significant Changes to 2026 ACA Marketplace Service Area” Agility Insurance Services. Sep. 19, 2025 ⤶

- ”Utah Rate Review Submissions” RateReview.HealthCare.gov. Accessed Sep. 22, 2025 ⤶

- ”2026 FINAL Gross Rate Changes – Utah: +14.2% (updated)” ACA Signups. Aug. 4, 2025 ⤶ ⤶

- ”Utah Rate Review Submissions” RateReview.HealthCare.gov. Accessed Dec. 1, 2025 ⤶

- ”Latest Rate Changes” Utah Health Insurance Transparency (Utah Insurance Department). Accessed Dec. 1, 2025 ⤶

- “Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums” Commonwealth Fund. December 2014 ⤶

- “FINAL PROJECTION: 2016 Weighted Avg. Rate Increases: 12-13% Nationally*” ACA Signups. October 2015 ⤶

- “Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC)” ACA Signups. August 2016 ⤶

- “2018 Rate Hikes” ACA Signups. October 2017 ⤶

- “2019 Rate Hikes” ACA Signups. October 2018 ⤶

- “2020 Rate Changes” ACA Signups. October 2019 ⤶

- “2021 Premium Changes on ACA Exchanges and the Impact of COVID-19 on Rates” KFF. October 2020 ⤶

- “2022 Rate Changes” ACA Signups. October 2021 ⤶

- “Utah: (Updated) Final Avg. Unsubsidized 2023 #ACA Premiums: +6.0%” ACA Signups. August 2022 ⤶

- Utah: *Final* Avg. Unsubsidized 2024 #ACA Rate Changes: +11.4%; Aetna & Imperial Joining Indy Market. ACA Signups. October 2023. ⤶

- ”Utah: Preliminary avg. unsubsidized 2025 #ACA rate changes: +10.4%; Cigna dropping out” ACA Signups. Sep. 18, 2025 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “2023 Marketplace Open Enrollment Period Public Use Files” CMS.gov, March 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶