Find Idaho Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Idaho Health Insurance Marketplace Guide

This Idaho health insurance guide, including the FAQs below, is designed to help you understand the health coverage options and possible financial assistance available to you and your family in Idaho.

Idaho created its own state-based health insurance exchange (Marketplace), which is called Your Health Idaho. This is Idaho’s platform where residents can shop for individual and family health plans offered by eight private health insurance carriers1 (coverage areas vary from one insurer to another). At least one of these insurers will not offer coverage in 2027 (details below about premium changes for 2026, and insurer participation changes for 2027).

When you enroll in a plan through Your Health Idaho, you may find that you’re eligible for financial assistance that reduces the monthly cost of your coverage (premium subsidies), and possibly also your out-of-pocket expenses (cost-sharing reductions, or CSR). These are federal subsidy programs created by the Affordable Care Act, and eligibility depends on your income and circumstances.

Your Health Idaho applicants who appear to be eligible for Medicaid will be referred to Idaho Medicaid where they can complete an application for coverage.

Idaho ACA Marketplace quick facts

Frequently asked questions about health insurance in Idaho

Who can buy Marketplace health insurance in Idaho?

In order to sign up for private health coverage through Your Health Idaho, you must:4

- Be an Idaho resident and lawfully present in the United States

- Not be incarcerated

- Not be enrolled in Medicare5

So most Idaho residents are eligible to enroll in coverage through the exchange. But eligibility for financial assistance is a bigger question for most people, and there are a few additional eligibility rules to qualify for subsidies through Your Health Idaho.

To qualify for income-based Advance Premium Tax Credits (APTC) or cost-sharing reductions (CSR), you must:

- Not be eligible to enroll in an affordable employer-sponsored health plan. If you have access to an employer’s health plan and aren’t sure if it’s considered affordable, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies to offset the cost of a Your Health Idaho plan.

- Not be eligible for Idaho Medicaid or CHIP.

- Not be eligible for premium-free Medicare Part A.6

- If married, file a joint tax return.7

- Not be able to be claimed by someone else as a tax dependent.7

Beyond those basic parameters, qualifying for Your Health Idaho’s subsidies will depend on your household’s income. Here’s how that’s calculated under the ACA.

When can I enroll in an ACA-compliant plan in Idaho?

Your Health Idaho’s open enrollment runs from October 15 to December 15.8 (Idaho and Georgia are the only states where open enrollment starts before November 1.)

Starting in the fall of 2026, for coverage effective in 2027 and future years, open enrollment will end on December 15 in the majority of the states. But although many state-run exchanges will continue their enrollment periods until the end of December, Idaho will not.

Idaho will be able to continue to use the October 15 to December 15 schedule, as that fits with the new federal rules that require open enrollment to start no later than November 1 and end no later than December 31, starting in the fall of 2026.9

After open enrollment ends, you may still be eligible to enroll or make a plan change, but only if you qualify for a special enrollment period.

Most special enrollment periods are triggered by qualifying life events, such as giving birth or losing other health coverage. However, Native Americans are eligible for a special enrollment period without a specific qualifying life event.

Enrollment in Idaho Medicaid and CHIP is available year-round for eligible residents.

How do I enroll in an Idaho Marketplace plan?

To enroll in an ACA Marketplace/exchange plan in Idaho, you can:

- Visit Your Health Idaho, which is Idaho’s health insurance exchange (Marketplace). The Your Health Idaho website will allow you to compare available health plans, determine whether you’re eligible for financial assistance, and enroll in a health plan.

- Enroll in a Your Health Idaho plan with the help of an insurance broker or certified enrollment counselor.

You can reach Your Health Idaho’s call center at 855-944-3246.

How can I find affordable health insurance in Idaho?

Income-based subsidies (APTC, created by the Affordable Care Act) are available to lower the amount you pay for your health coverage each month. These subsidies are available to enrollees who meet the eligibility requirements and select a metal-level health plan through Your Health Idaho.

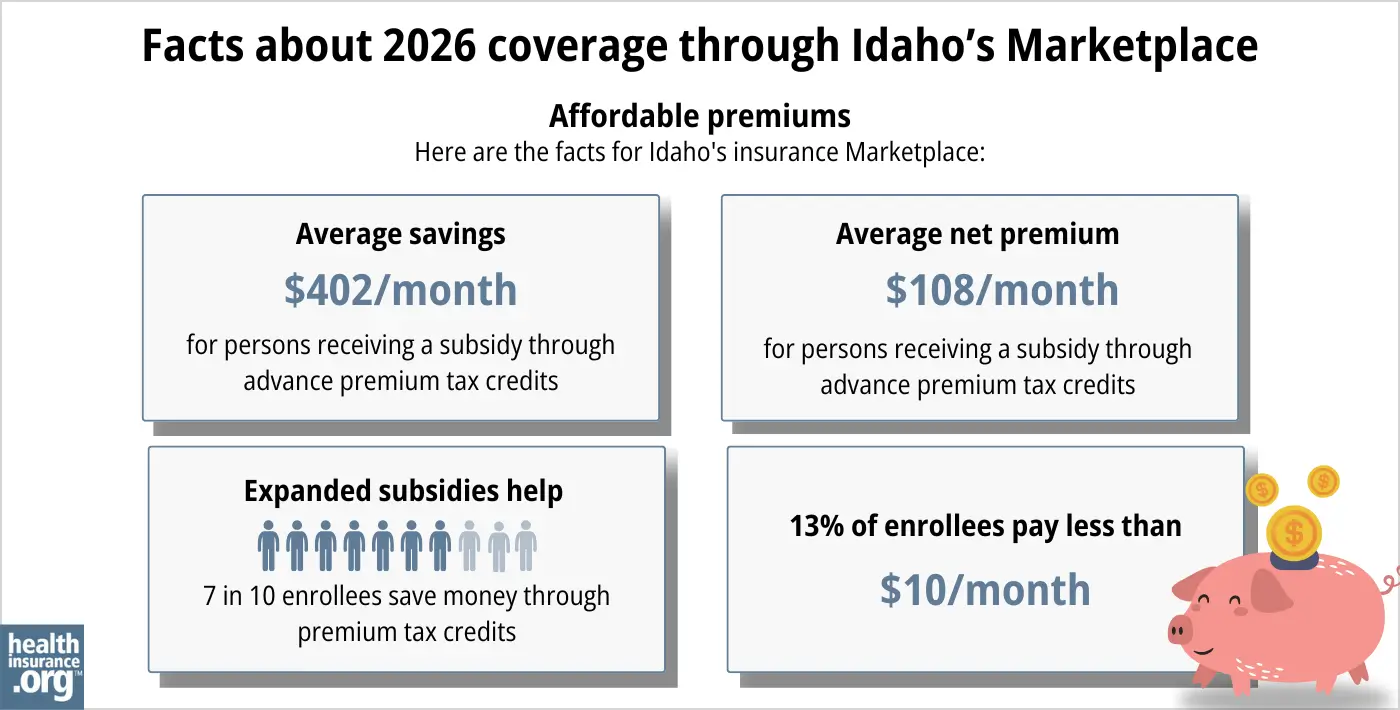

Seventy-six percent of the people who enrolled through Your Health Idaho during open enrollment for 2026 coverage were eligible for premium subsidies. These subsidies paid an average of $402/month. For Idaho enrollees who receive subsidies, the average after-subsidy premium in 2026 is about $108/month.10

Source: CMS.gov10

Although most Your Health Idaho enrollees qualify for premium subsidies, the state’s reinsurance program helps to keep full-price premiums lower than they would otherwise be, making coverage more affordable for people who have to pay full price.11

If your household doesn’t earn more than 250% of the federal poverty level, you’ll also be eligible for federal cost-sharing reductions (CSR) as long as you select a Silver-level plan through Your Health Idaho. These subsidies will reduce your deductible and other out-of-pocket expenses, making health care more affordable. More than a quarter of Your Health Idaho enrollees were receiving CSR benefits as of early 2026.12

If you’re eligible for APTC and CSR, you can use them both if you enroll in a Silver-level plan through Your Health Idaho (APTC can be used with any metal-level plan, but you can only get CSR benefits if you enroll in a Silver plan).

Depending on your income and circumstances, you may be able to enroll in free or low-cost health coverage through Idaho Medicaid or CHIP. Learn more about whether you might be eligible for Medicaid and CHIP in Idaho.

How many insurers offer Marketplace coverage in Idaho?

For 2026 coverage, eight insurers offer exchange plans in Idaho, with varying coverage areas.13 These are the same eight insurers that offered coverage for 2025.14

But for 2027, PacificSource will no longer offer plans in Idaho’s Marketplace.15 Enrollees with PacificSource coverage will need to select new plans for 2027, during the open enrollment period that begins October 15, 2026 in Idaho.

Are Marketplace health insurance premiums increasing in Idaho?

For 2026, the following average rate changes were approved for Idaho’s Marketplace insurers, amounting to an overall average rate increase of 10%, before any subsidies are applied.13 (This is less than half the nationwide percentage rate increase for 2026,16 but after-subsidy premiums are increasing by a significantly larger percentage for 2026 due to the expiration of federal subsidy enhancements.)

Idaho’s ACA Marketplace Plan 2026 APPROVED Rate Changes by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Blue Cross of Idaho Health Service, Inc. | 12% |

| Molina Healthcare of Utah | 16% |

| Mountain Health CO-OP (an ACA-created CO-OP): | 13% |

| PacificSource Health Plans | 16% |

| Regence Blue Shield of Idaho | 8% |

| SelectHealth | 8% |

| St. Luke’s Health Plan | 9% |

| Moda Health | 12% |

Source: Idaho Department of Insurance13

Average rate changes apply to full-price rates, and most enrollees do not pay full price. Subsidy amounts vary from one enrollee to another and change annually depending on the cost of the second-lowest-cost Silver plan relative to the enrollee’s household income. The American Rescue Plan and the Inflation Reduction Act resulted in larger, more widely available subsidies through 2025.

But Congress did not extend the subsidy enhancements, and allowed them to expire at the end of 2025. As a result, subsidies don’t cover as much of enrollees’ total premiums in 2026, and some people lost their subsidies altogether. The resulting net premium increases are likely the reason 8,850 people cancelled their Your Health Idaho coverage during the open enrollment period for 2026, instead of renewing or selecting a new plan.17

Here’s an overview of how average pre-subsidy premiums have changed over the years in Idaho’s individual/family market:

- 2016: Average increase of 20%18

- 2017: Average increase of 24%19

- 2018: Average increase of 27%20

- 2019: Average increase of 5%21

- 2020: Average increase of 6.3%22

- 2021: Average increase of 1%23

- 2022: Average decrease of 2%24

- 2023: Average decrease of 3.6%25 (reinsurance program took effect)

- 2024: Average decrease of 1%26

- 2025: Average increase of 5%14

How many people are insured through Idaho’s Marketplace?

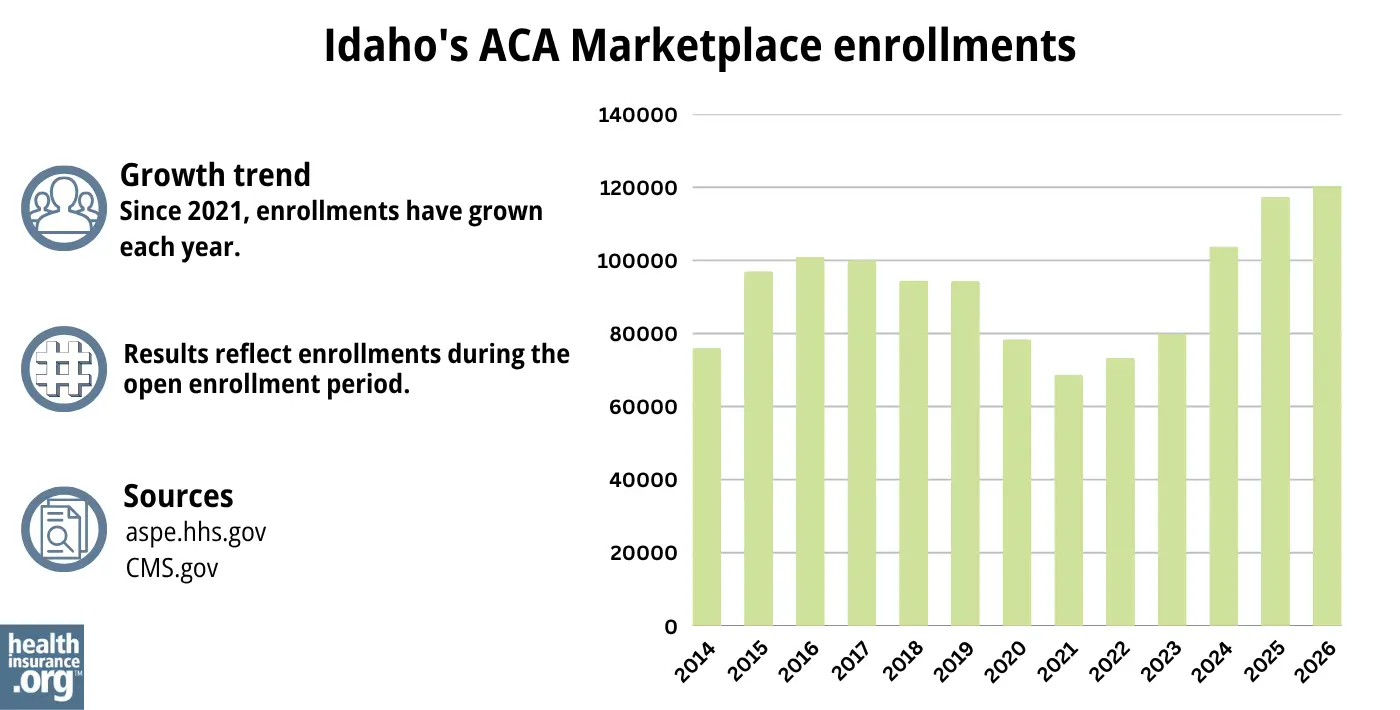

More than 120,000 Idaho residents enrolled in 2026 coverage through Your Health Idaho during the open enrollment period that ended December 15, 2025. This was a record-high, slightly above the previous high of 117,373 people who enrolled the year before.10

But Your Health Idaho officials noted that 8,850 people actively cancelled their coverage during open enrollment, and they expected another 20,000 to either cancel their policies or have them lapse due to nonpayment in the first few months of 2026, due to the failure of Congress to extend the federal subsidy enhancements that expired at the end of 2025.17

This was a record high for Idaho’s Marketplace.

Source: 2014,27 2015,28 2016,29 2017,30 2018,31 2019,32 2020,33 2021,34 2022,35 2023,36 2024,37 202538 202610

What health insurance resources are available to Idaho residents?

Your Health Idaho – This is the state-based exchange/Marketplace in Idaho, where you can compare plans, determine financial assistance eligibility, and select a health plan. You can reach Your Health Idaho at 855-YHIdaho (855-944-3246)

State Exchange Profile: Idaho – The Henry J. Kaiser Family Foundation overview of Idaho’s progress toward creating a state health insurance exchange.

Idaho Department of Insurance – Regulates the insurance industry in Idaho, and addresses consumers’ questions and complaints related to insurance.

(208) 334-4250 / toll-free (800) 721-3272.

Idaho Senior Health Insurance Benefits Advisors – A service for Idaho Medicare beneficiaries and their caregivers, providing information and assistance with questions related to Medicare eligibility, enrollment, and claims.

Looking for more information about other options in your state?

Need help navigating health insurance options in Idaho?

Explore more resources for options in ID including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”Health insurance rates for 2026 are now available to the public” Idaho Department of Insurance. Oct. 3, 2025 ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Idaho Rate Review Individual” Idaho Department of Insurance. Accessed Aug. 30, 2025 *The above is based on the most current data available. ⤶

- ”Frequently Asked Questions About Your Health Idaho” Your Health Idaho. Accessed Dec. 17, 2025 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Dec. 17, 2025 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Dec. 17, 2025 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Dec. 17, 2025 ⤶ ⤶

- ”Apply and Enroll” Your Health Idaho. Accessed June 10, 2026 ⤶

- ”Patient Protection and Affordable Care Act; Marketplace Integrity and Affordability” Federal Register, U.S. Department of Health & Human Services. June 25, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶

- Reinsurance Innovation Waiver under Section 1332 of ACA. Idaho Department of Insurance. Accessed December 2023. ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov, Mar.27, 2026 ⤶

- ”Idaho Rate Review Individual” Idaho Department of Insurance. Accessed Dec. 17, 2025 ⤶ ⤶ ⤶

- ”Health insurance rates for 2025 now available to the public” Idaho Department of Insurance. Oct. 1, 2024 ⤶ ⤶

- ”PacificSource to exit ACA market, pull out of Montana entirely” Becker’s Payer Issues. May 22, 2026 ⤶

- ”2026 Rate Change Project” ACA Signups. Nov. 2, 2025 ⤶

- ”Thousands of Idahoans cancel health insurance plans on exchange ahead of subsidies ending” Idaho Capital Sun. Dec. 17, 2025 ⤶ ⤶

- FINAL PROJECTION: 2016 Weighted Avg. Rate Increases: 12-13% Nationally* ACA Signups. October 2015. ⤶

- Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC). ACA Signups. October 2016. ⤶

- 2018 Rate Hikes. ACA Signups. October 2017. ⤶

- 2019 Rate Hikes. ACA Signups. October 2018. ⤶

- 2020 Rate Changes. ACA Signups. October 2019. ⤶

- Idaho Rate Review Individual, Summary for 2021 Coverage. Idaho Department of Insurance. Accessed December 2023. ⤶

- Idaho Rate Review Individual, Summary for 2022 Coverage. Idaho Department of Insurance. Accessed December 2023. ⤶

- “Idaho: Final Avg. Unsubsidized 2023 #ACA Rate Changes: -3.6% (Was -2.5%)” ACASignups.net, Oct. 12, 2022 ⤶

- Idaho’s individual health insurance rates decrease for 2024. Idaho Department of Insurance. September 2023. ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶