Medicare in Maryland

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Maryland

Medicare enrollment in Maryland

The number of Maryland residents with Medicare stood at 1,185,182 as of February 2026.1

About 8% of Maryland’s Medicare beneficiaries are under 65 and eligible due to a disability that has lasted at least 24 months (people with end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS) do not have to wait 24 months for their Medicare coverage to take effect).1 The rest of the state’s Medicare beneficiaries – nearly 92% – are 65 or older and qualify for Medicare due to their age.1

Nationwide, about 91% of Medicare beneficiaries are at least 65 years old, while 9% are under 65 and eligible due to disability.2

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Maryland’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

Medicare Advantage plan availability and enrollment in Maryland

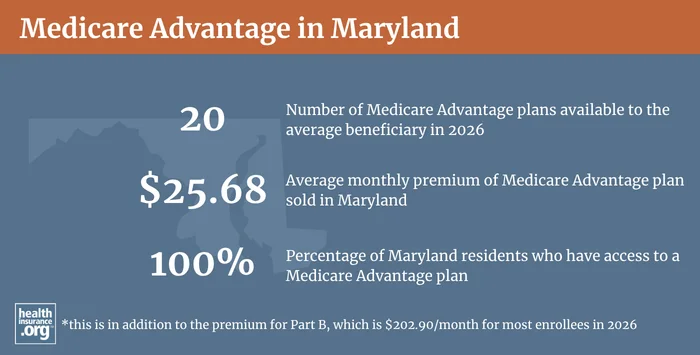

As of February 2026, about 25% of people with Medicare in Maryland were enrolled in private Medicare Advantage plans, while the other 75% were enrolled in Original Medicare.1 At that point, about 51% of all Medicare beneficiaries nationwide were enrolled in Medicare Advantage plans,3 but Medicare Advantage enrollment continues to be less popular in Maryland.

Medicare Advantage plans are available in all areas of Maryland in 2026. The average Medicare beneficiary in Maryland can choose from among 20 Medicare Advantage plans in 2026, but plan availability varies by county.4

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Maryland by contacting a licensed agent.

Medicare supplement (Medigap) plan availability in Maryland

According to an AHIP analysis, 265,989 people had Medigap coverage in Maryland as of late 2023.5

In Maryland in 2026, there are 29 insurers offering Medigap plans, although some only offer a few of the ten plan designs.6

Under federal rules, Medicare beneficiaries have a six-month window, when they are at least 65 and first enrolled in Medicare Part B, during which coverage is guaranteed issue for Medigap plans. Maryland has gone a step further than that and joined several other states that offer “birthday rules” that allow Medigap enrollees to switch to a different plan, without medical underwriting, during an annual window around their birthday. In Maryland, the birthday rule took effect in mid-2023.6 It allows a person with Medigap to switch to a different Medigap plan – with equal or lesser benefits – during a 30-day window that starts on their birthday each year (see page 3 of this guide for a list of which policies are available depending on which policy a person has).

Federal rules do guarantee access to a Medigap plan if you’re under 65 and eligible for Medicare as a result of a disability.

But Maryland is among the majority of the states that ensure at least some access to Medigap plans for enrollees under the age of 65. In Maryland, Medigap insurers are required to offer Plan A to enrollees who are under 65, on a guaranteed-issue basis if the person applies for the Medigap plan within six months of enrolling in Medicare Part B.

Medigap insurers in Maryland are also required to offer Medigap Plan D to beneficiaries, but only if the insurer offers that plan to other enrollees.7 Insurers that offer Medigap Plan C must also offer it to disabled Medigap enrollees who were already eligible for Medicare prior to 2020. (Under federal rules, Medigap plans C and F cannot be sold to anyone who is newly eligible for Medicare in 2020 or later.) But as of 2026, only two Medigap insurers in Maryland offer Plans C and D.6

The requirement that Medigap insurers offer coverage to disabled beneficiaries is a result of Maryland S.B.48, which took effect in 2017.

The premiums are higher for enrollees under age 65,6 although they are given another enrollment window when they turn 65, so they can then change to lower-cost Medigap coverage at that point. And at age 65, these enrollees have access to any available Medigap plan, as opposed to being limited to only Plan A (or Plan C or D if their insurer offered it), which was the case before they turned 65. And Maryland does limit the pricing on Medigap Plan A for disabled enrollees: It cannot exceed the average of the premiums paid for that Plan A by enrollees who are 65 and older.7

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

Medicare Part D plan availability and enrollment in Maryland

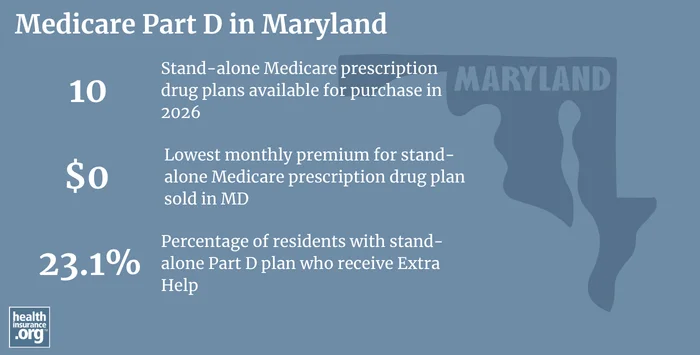

For 2026 coverage, insurers are offering 10 stand-alone Part D plans available in Maryland, with premiums starting at $0 per month.8

As of February 2026, 612,350 Maryland Medicare beneficiaries were enrolled in stand-alone Part D prescription drug plans (PDPs) in Maryland.1 Enrollment in Original Medicare in Maryland is higher than average, which is why stand-alone Medicare Part D enrollment in Maryland is also higher than average. In addition to the people with stand-alone Part D coverage, 245,421 Medicare beneficiaries in Maryland have Part D benefits as part of their Medicare Advantage coverage.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Maryland

If you need help with your Medicare application in Maryland or have general questions about Medicare eligibility in Maryland, try one of these resources for assistance.

- Maryland Senior Health Insurance Program: Visit the website or call your county office.

- The Maryland Insurance Administration has a comprehensive overview of Medigap in Maryland, and a detailed comparison of how Medigap premiums vary by age and insurer in Maryland.

- The Medicare Rights Center provides information geared to Medicare beneficiaries, caregivers, and professionals.

Looking for more information about other options in your state?

Need help navigating health insurance options in Maryland?

Explore more resources for options in MD including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Maryland” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data, May 2026. ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data, May 2026. ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org. Dec. 9, 2025 ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Monthly Premiums for Medicare Supplement Policies as of January 1, 2026” Maryland Insurance Administration. Accessed May 30, 2026 ⤶ ⤶ ⤶ ⤶

- “Medicare Supplement in Maryland” Maryland Insurance Administration. Accessed May 30, 2026 ⤶ ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶