Medicare in Minnesota

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Minnesota

In this article

- Medicare enrollment in Minnesota

- Medicare Advantage plan availability and enrollment in Minnesota

- Are Medicare Cost Plans available in Minnesota?

- Medicare supplement (Medigap) plan availability in Minnesota

- Medicare Part D availability and enrollment in Minnesota

- Resources for Medicare beneficiaries in Minnesota

Medicare enrollment in Minnesota

As of January 2026, 1,193,633 Minnesota residents were enrolled in Medicare coverage.1

Most individuals become eligible for Medicare when they turn 65. But people may become eligible for Medicare if they have been receiving certain disability benefits for 24 months or have amyotrophic lateral sclerosis (ALS) or end-stage renal disease (ESRD). In the United States, about 9% of all Medicare beneficiaries – about 6.5 million people – are under age 65.2 It’s a little lower in Minnesota, where only about 8% of Medicare beneficiaries are under age 65 and eligible due to a disability.1

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Minnesota’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

Medicare Advantage plan availability and enrollment in Minnesota

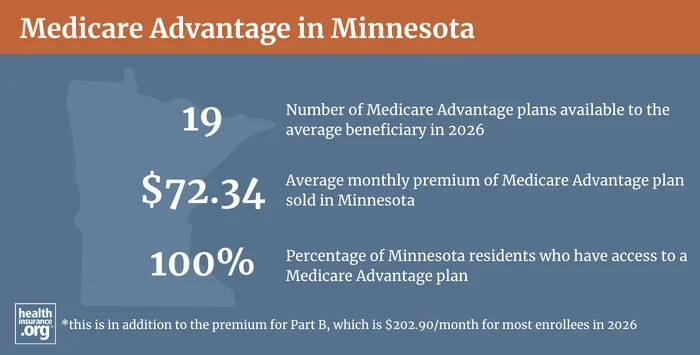

Plan availability varies by county, but Minnesota’s Medicare Advantage market is strong: Residents throughout the state can select from on average 19 Medicare Advantage plans for 2026.3

About 56% of all Minnesota Medicare enrollees were enrolled in private Medicare Advantage or Medicare Cost plans (described below) as of January 2026,1 as opposed to a national average of about 51%.4

Minnesota was the first to participate in a demonstration program to pilot Medicare Cost plans in the 1970s, and the plans remained popular over the decades. These plans are discussed in more detail below. Minnesota is one of only a handful ofstates where Medicare Cost plans are available in 2026.5

Learn more about Medicare Advantage and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Minnesota by contacting a licensed agent.

Are Medicare Cost Plans available in Minnesota?

The legislation that introduced Medicare Advantage also created a competition clause that banned Medicare Cost plans from operating in areas where they faced substantial competition from Medicare Advantage plans, but the implementation of the competition clause was delayed for many years. In 2015, legislation (MACRA) called for the competition clause to be implemented in 2019.

As a result, Medicare Cost Plans, which covered more than 40% of Minnesota Medicare beneficiaries in 2018,6 were discontinued in 66 Minnesota counties at the end of 2018.7 These Medicare Cost Plans include Medicare Part A and Part B coverage, but with the flexibility to see non-network providers. A Medicare Cost Plan may also include the option of obtaining separate Medicare Part D prescription drug coverage.8 In 2018, more than 40% of Minnesotans were enrolled in Medicare Cost Plans. By 2019, that had dropped to about 6%, and it has hovered at that level since then.9

One of the reasons Medicare Cost has been so popular in Minnesota is that the state has a large population of “snowbirds” – retirees who live in Minnesota during the summer, but head south to warmer climes in the winter. With Medicare Cost plans, the enrollee still has Original Medicare – including the large nationwide network of providers who work with Medicare – in addition to the Medicare Cost coverage.

Medicare Advantage plans, in contrast, tend to have localized networks that might not be suitable for a senior who lives in two different states during the year. A Medigap plan plus Original Medicare will allow a person in that situation to have access to health providers in both locations, although Medigap tends to be more expensive than Medicare Advantage. There are pros and cons to both options, and no one-size-fits-all solution.

As of 2026, there were still Medicare Cost plans available in 21 counties in Minnesota.10 Medicare Cost plans in the state are offered by Blue Cross Blue Shield of Minnesota and Medica.

Medicare supplement (Medigap) enrollment and regulations in Minnesota

Thirteen insurers offered Medigap policies in Minnesota as of 2025.11

According to AHIP, 206,932 Minnesota Medicare beneficiaries were enrolled in Medigap plans (also known as Medicare Supplement insurance) in 2023,12 to supplement their Original Medicare coverage.

Learn how Medigap plans are regulated and standardized.

Medigap plan standardization is different in Minnesota

In all but three states, Medigap policies are standardized under federal rules.13 But Minnesota is one of three states that have federal waivers that allow the state to do its own Medigap standardization.14

So instead of the ten Medigap plans (A through N) that are marketed in most states, Minnesota Medigap plans include: Basic, Basic with riders, Extended Basic, Medicare SELECT (policies that require enrollees to stay within their provider network), and Medigap policies with limited coverage.15

Efforts to create an annual Medigap enrollment window

Under federal rules, there’s no annual guaranteed-issue enrollment opportunity for Medigap. But Minnesota enacted legislation in 2023 to create a Medigap guaranteed issue window each fall, during the October 15 – December enrollment window that applies to other private Medicare plans (Part D and Medicare Advantage). The new law was scheduled to take effect in August 2025, but that has been delayed to August 2026.16

Some stakeholders, including the insurer that holds the majority of the Medigap market share in Minnesota, have asked lawmakers to repeal the new guaranteed-issue open enrollment period before it takes effect.17 The stakeholders have said that premiums will be higher if there’s an annual guaranteed-issue enrollment window for Medigap plans. To address this, additional legislation was enacted in 2025, calling for higher premiums for people utilizing the new guaranteed-issue enrollment window to sign up for Medigap for the first time.18

Medigap for people under age 65

Federal rules do not guarantee access to Medigap plans for people who are under 65, but the majority of the states – including Minnesota – have implemented rules to ensure that disabled Medicare beneficiaries have at least some access to Medigap plans. Minnesota law grants a six-month open enrollment period to anyone who enrolls in Medicare Part B, regardless of age.19 (Federal rules only grant this window to people who enroll in Part B and are also at least 65 years old.)

Other consumer protections

Minnesota prohibits Medigap insurers from basing premiums on an enrollee’s age. Premiums for Medigap plans in Minnesota only vary based on tobacco use and where the enrollee lives.11 (As noted above, the new guaranteed issue annual enrollment window for Medigap will allow higher premiums if a person is enrolling in Medigap for the first time using that window.)

Minnesota law also prevents Medigap insurers from imposing pre-existing condition waiting periods if the beneficiary enrolls during their initial six-month open enrollment window. For those who apply after that, Medigap insurers are not allowed to impose pre-existing condition waiting periods if the enrollee wasn’t diagnosed or treated for the condition in the 90 days before enrolling in the Medigap policies.19

Medicare Part D plan availability and enrollment in Minnesota

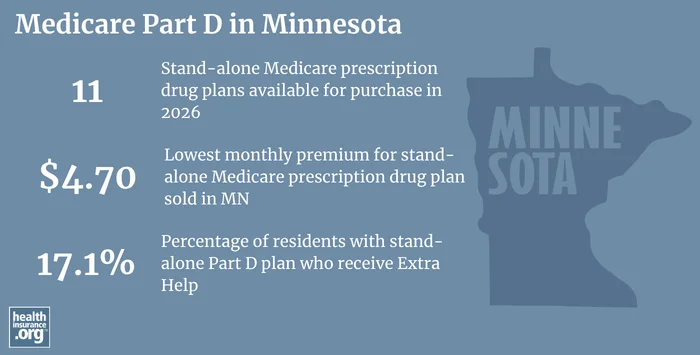

There are 11 stand-alone Medicare Part D prescription drug plans for sale in Minnesota for 2026, with premiums starting at $4.70 per month.20

In Minnesota, as of January 2026, there were 436,232 people with stand-alone Medicare Part D prescription drug coverage. Another 558,195 Medicare beneficiaries in Minnesota had Medicare Part D prescription drug coverage as part of their Medicare Advantage plans.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Minnesota

- You may contact Minnesota Aging Pathways with questions related to Medicare coverage in the state, or for assistance with eligibility or enrollment.

- This overview of how Minnesota’s Medicaid program can help Medicare beneficiaries with limited financial means is a useful resource.

- The Minnesota Commerce Department has a Medicare resource and information page on its website. It also regulates and licenses the health insurance companies that offer policies in the state, as well as the agents and brokers who sell those policies, and can address consumers’ questions and complaints.

- The Medicare Rights Center is a nationwide service that can answer questions and provide information about Medicare.

Looking for more information about other options in your state?

Need help navigating health insurance options in Minnesota?

Explore more resources for options in MN including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Minnesota” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org Dec. 9, 2025 ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶

- “Medicare” Minnesota Commerce Department. Accessed May 11, 2026 ⤶

- “Minnesota Health Care Spending: 2018 and 2019 Estimates and Ten-Year Projections” Minnesota Department of Health. Oct. 2021 ⤶

- “Counties Where Medicare Cost Plans Will Continue Beyond 2020” Minnesota Commerce Department. Accessed May 11, 2026 ⤶

- “Medicare Cost Plans” Centers for Medicare & Medicaid Services. Accessed May 11, 2026 ⤶

- “Public Health Insurance Programs” MN Department of Health, Jan. 9, 2023. ⤶

- “Individual Cost Plan Products, Minnesota Health Plans 2026” Minnesota Commerce Department. Accessed May 11, 2026 ⤶

- “Annual Premium Guide: Medicare Supplement. Basic, Extended Basic, other plans and optional riders currently marketed in Minnesota” Minnesota Commerce Department. Accessed Oct. 3, 2025 ⤶ ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025. Accessed Oct. 3, 2025 ⤶

- “Medigap: Background and Statistics – CRS Reports” Congress.gov. Accessed Oct. 3, 2025 ⤶

- “Medigap in Minnesota” Medicare.gov. Accessed Oct. 3, 2025 ⤶

- “Minnesota Medigap insurance policy options” Minnesota Commerce Department. Accessed Oct. 3, 2025 ⤶

- “Medicare Supplement Open Enrollment Impact Study” Minnesota Commerce Department. Accessed May 11, 2026 ⤶

- “Letters from stakeholders regarding Minnesota’s new Medigap annual enrollment period” Accessed Oct. 1, 2025 ⤶

- “Minnesota HF4” BillTrack50. Enacted June 15, 2025 ⤶

- “Sec. 62A.31 MN Statutes” Office of the Revisor of Statutes. Accessed May 11, 2026 ⤶ ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. September 26, 2025 ⤶