Find Pennsylvania Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Pennsylvania Health Insurance Marketplace Guide

This guide, including the FAQs below, was developed to help you choose the right Pennsylvania health insurance plan for you and your family. The options found in Pennsylvania’s ACA Health Insurance Marketplace can be a good choice for individuals and families who don’t have access to employer-sponsored health insurance or government-run coverage like Medicare or Medicaid.

Pennsylvania uses a fully state-based health insurance Marketplace known as Pennie to enroll its residents in ACA Marketplace plans. The Marketplace provides access to health insurance products from private insurers.

The Pennsylvania Health Insurance Marketplace is robust, with 14 insurers offering coverage for 2026, all of which plan to continue to offer coverage in 2027 1 (with potential consolidation among multiple entities of one parent company; see below for details and 2027 premium change information).

Depending on income and other circumstances, most Pennsylvania Marketplace enrollees get help to lower their monthly insurance premium (the amount you pay to enroll in the coverage). And many also receive financial assistance with their out-of-pocket expenses. But because Congress allowed federal subsidy enhancements to expire at the end of 2025, after-subsidy premiums increased significantly in 2026, and the “subsidy cliff” returned.2

As described below, Pennsylvania has been considering a state-funded subsidy program that would stack on top of the federal ACA subsidies to make coverage more affordable for lower-income Pennie enrollees, but that program is not yet available because state funding has not been allocated.3 Several other states offer state-funded subsidies, in addition to the ACA’s federal subsidies.

Pennsylvania has an “easy enrollment” program that allows uninsured residents to access Pennsylvania health insurance via their state tax returns.4 The state also established a reinsurance program that took effect in 2021, helping to keep unsubsidized individual/family health insurance premiums lower than they would otherwise be.5

Frequently asked questions about health insurance in Pennsylvania

Who can buy Marketplace health insurance in Pennsylvania?

To be eligible to enroll in Pennsylvania Health Insurance Marketplace coverage, you must:

- Live in Pennsylvania

- Be lawfully present in the United States

- Not be incarcerated

- Not be enrolled in Medicare

Eligibility for financial assistance in the form of premium subsidies and cost-sharing reductions depends on your income and how it compares with the cost of the second-lowest-cost Silver plan in your area – which depends on your age and location. In addition, to qualify for financial assistance with your Marketplace plan you must:

- Not have access to affordable health coverage through your employer. If your employer offers coverage but you feel it’s too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies in the Marketplace.

- Not be eligible for Medicaid or CHIP, or premium-free Medicare Part A.8

- File a joint tax return, if married.9 (with very limited exceptions)10

- Not be able to be claimed by someone else as a tax dependent.9

When can I enroll in an ACA-compliant plan in Pennsylvania?

In Pennsylvania, the open enrollment period for 2027 individual and family coverage runs from October 15, 2026 to December 15, 2026.11

Note: A few days after it was published by Pennie, a judge vacated the federal rule change that had required a shorter open enrollment period.12 So it’s possible that Pennie’s enrollment schedule could change in response to that court ruling.

Outside of open enrollment, you’ll need a special enrollment period (SEP) to enroll or make changes to your coverage. In most cases, a SEP requires a qualifying life event, but Native Americans can enroll year-round without a qualifying live event.

Pennsylvania also has an “easy enrollment” program that allows uninsured residents to begin the process of accessing health insurance via their state tax returns.4 Pennie confirmed by phone that about 900 people used Path to Pennie to obtain coverage in 2023, including Medicaid and private plans.

How do I enroll in a Pennsylvania Marketplace plan?

To enroll in an ACA Marketplace plan in Pennsylvania, you can:

- Visit Pennie to enroll in Pennsylvania’s Marketplace. Here you will find an online platform to shop, compare plans and determine your subsidy eligibility.

- Purchase individual and family health coverage with the help of an insurance agent or broker, a Navigator or certified application counselor.

How can I find affordable health insurance in Pennsylvania?

You may find affordable health insurance options in Pennsylvania by utilizing the state’s health insurance exchange – Pennie. Here, residents can enroll in health coverage as well as determine their eligibility for financial assistance.

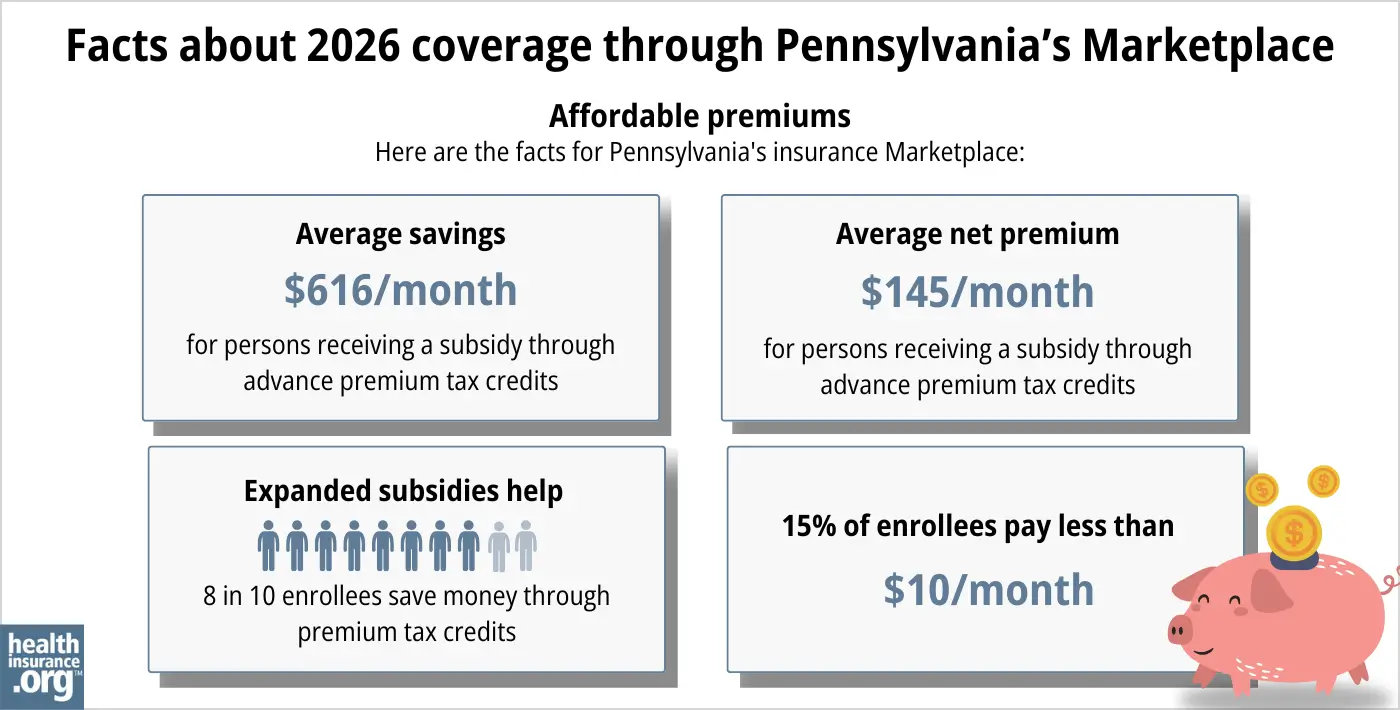

During the open enrollment period for 2026 coverage, about 80% of Pennie enrollees qualified for premium tax credits (premium subsidies). These tax credits amounted to an average savings of $616/month. Subsidy-eligible enrollees paid an average of $145 per month for health coverage, after their subsidies were applied.13

In addition to premium tax credits, Marketplace enrollees with household incomes up to 250% of the federal poverty level also qualify for cost-sharing reductions (CSR) that result in lower out-of-pocket costs (deductible, coinsurance, copays) on Silver plans. During the open enrollment period for 2026 coverage, about 23% of Pennie enrollees selected plans with CSR benefits.13

Source: CMS.gov13

Between the premium subsidies and cost-sharing reductions, you’ll likely find that a plan obtained via Pennie provides you with the best overall value.

At some point, if state funding is allocated, Pennsylvania may start to offer additional subsidies, beyond the federal subsidies that are already available.14 But as of mid-2026, state funding had not yet been allocated for this purpose, so Pennsylvania is not among the states that offer additional state-funded subsidies.

Governor Shapiro’s proposed 2024-25 budget calls for the state to create “an additional subsidy wrap” to make Pennie coverage more affordable for low-income and middle-income applicants.15

Legislation to create an “affordability assistance program” passed the Pennsylvania House in June 2024 and was sent to the Senate for consideration, but ultimately did not advance during the 2024 session.16 As a result, Pennie’s board of directors noted that funding for the state subsidy program was not available for plan year 2025.17 Funding was also not secured for 2026, and had still not been made available as of mid-2026, making it unlikely that state subsidies will be available for 2027.

The 2024 legislation did not contain any specific parameters for how the subsidies would have worked (premium subsidies or cost-sharing reductions) or who would have been eligible for them. It only noted that the program should be designed “to incentivize enrollment in on-exchange policies based on income or other eligibility criteria.”18

As of May 2024, the Pennie Board of Directors was recommending a sliding scale premium subsidy for gold and silver plans, for households earning between 151% and 300% of the federal poverty level.19

The state will only be able to proceed with the subsidy program if the state can secure alternate funding for its reinsurance program, so that some of the funds currently being used for reinsurance can be diverted to the affordability assistance program.20

How many insurers offer Marketplace coverage in Pennsylvania?

There are 14 Marketplace insurers in Pennsylvania in 2026,21 although several of them share parent companies.

For 2027, there will be at least 13 Marketplace insurers, but one of the three Highmark entities doesn’t have a rate filing available. So it’s possible that Highmark Coverage Advantage (no filing for 2027) enrollees will be consolidated with Highmark Inc. or Highmark Benefits Group, both of which have filed rates and plans for 2027.1 Carriers have unique coverage areas, so plan availability for 2027 varies by location.22

There were also 14 Pennsylvania Marketplace insurers in 2025, although Pennsylvania Health & Wellness became Ambetter in 2026, and UPMC became UPMC Health Plan.23 Enrollees in the 2025 versions of those plans were transitioned to the new plans unless they selected different coverage during open enrollment.

Are Marketplace health insurance premiums increasing in Pennsylvania?

The following average rate changes have been proposed for 2027 by the insurers that offer Marketplace coverage in Pennsylvania, amounting to a weighted average increase of 17.1% (calculated before subsidies are applied).1

Pennsylvania’s ACA Marketplace Plan 2027 PROPOSED Rate Changes by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Capital Advantage Assurance | 18.3% |

| Geisinger Health Plan | 10.5% |

| Geisinger Quality Options | 13% |

| Highmark, Inc. (EPO and PPO) | 16.2% |

| Highmark Benefits Group | 21.4% |

| Highmark Coverage Advantage | No filing |

| Keystone Health Plan East (Independence Blue Cross HMO) | 14.7% |

| QCC Insurance Company (Independence Blue Cross PPO) | 19.9% |

| UPMC Health Plan (previously UPMC Health Coverage) | 15.8% |

| UPMC Health Network (previously UPMC Health Options) | 12% |

| Ambetter (previously PA Health and Wellness) | 40.9% |

| Oscar Health | 15.4% |

| Jefferson Health Plans HMO (Health Partners Plans, Inc.) | 15.9% |

| Jefferson Health Plans PPO (Partners Insurance Company) | 20.5% |

Source: Commonwealth of Pennsylvania1

Average rate changes apply to full-price health plans, but the majority of Pennsylvania health insurance marketplace enrollees receive premium subsidies, and thus do not pay full price.13

Because federal subsidy enhancements expired at the end of 2025, net premiums increased significantly in 2026. Here are some examples of the sort of net premium increases that people saw in Philadelphia for 2026:24

- 40-year-old earning $40,000:

- Lowest-cost plan in 2025 was $41/month

- Lowest-cost plan in 2026 is $116/month

- 60-year-old earning $63,000:

- Lowest-cost plan in 2025 was $205/month

- Lowest-cost plan in 2026 is $631/month

For perspective, here’s a summary of how average full-price premiums for Pennsylvania health insurance have changed over time:

- 2015: Average increase of 12%25

- 2016: Average increase of 12%26

- 2017: Average increase of 32.5%27

- 2018: Average increase of 30.6%

- 2019: Average decrease of 2.3%28

- 2020: Average increase of 3.8%29

- 2021: Average decrease of 3.3%30

- 2022: Average increase of 0.2%31

- 2023: Average increase of 5.5%32

- 2024: Average increase of 3.9%33

- 2025: Average increase of 6%34

- 2026: Average increase of 21.5%21

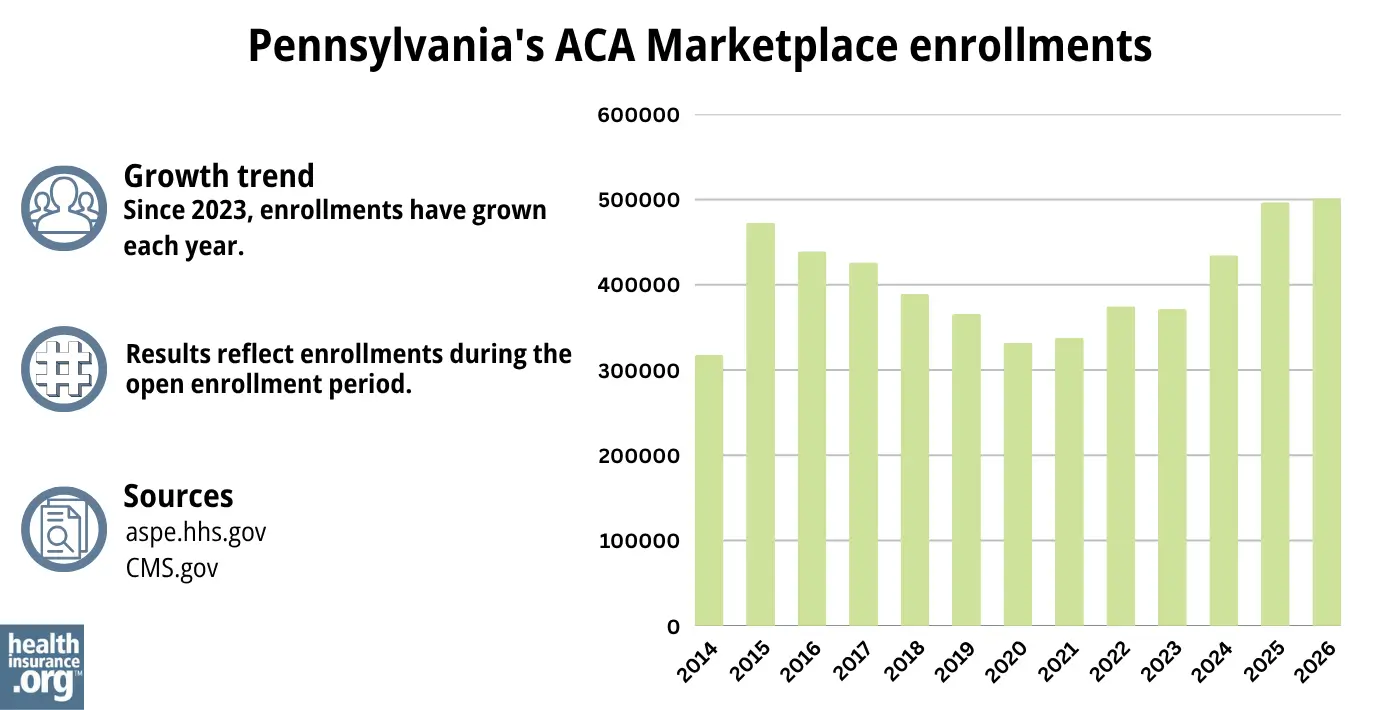

How many people are insured through Pennsylvania’s Marketplace?

What health insurance resources are available to Pennsylvania residents?

Pennie

The official Pennsylvania health coverage Marketplace.

State Exchange Profile: Pennsylvania

The Henry J. Kaiser Family Foundation overview of Pennsylvania’s progress toward creating a state health insurance exchange.

Health Care Matters, Pennsylvania Office of the Attorney General

Serves Pennsylvania consumers with health-related problems.

(717) 705-6938 / Toll-free: 1-877-888-4877 (only in Pennsylvania)

Pennsylvania Consumer Assistance Program

Assists people with private insurance, Medicaid, or other insurance with resolving problems pertaining to their health coverage; assists uninsured residents with access to care.

(877) 881-6388 / [email protected]

Looking for more information about other options in your state?

Need help navigating health insurance options in Pennsylvania?

Explore more resources for options in PA including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”Shapiro Administration Receives Proposed 2027 Health Insurance Rates; Plans to Carefully Examine Companies’ Proposals and Reject Excessive, Inadequate, or Unfairly Discriminatory Increases” PA.gov. July 23, 2026 ⤶ ⤶ ⤶ ⤶

- ”Pennie Board of Directors Meeting” Pennie. Oct. 2025 ⤶

- ”Establishing a State Health Insurance Affordability Program” Pennie. Accessed Dec. 14, 2025 ⤶

- ”Path to Pennie” Pennie.com. Accessed July 28, 2026 ⤶ ⤶

- ”Act 42 & Pennsylvania’s Section 1332 Waiver Reinsurance Program” Pennsylvania Insurance Department. Accessed July 28, 2026 ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- “Shapiro Administration Announces Proposed 2026 Health Insurance Rate Updates” Pennsylvania Insurance Department. Aug. 1, 2025 *The above is based on the most current data available. ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed July 28, 2026 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed July 28, 2026 ⤶ ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- “Pennsylvanians dropping health coverage through Pennie citing higher plan costs as the number one reason” Pennie.com. June 9, 2026 ⤶

- ”City of Columbus et al. v. Kennedy et al. (Columbus I)” O’Neill Institute, Health Care Litigation Tracker. Vacatur order June 12, 2026 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- ”Pennie Board of Directors Strategic Planning Session” (pages 27-30). Pennie Board of Directors. February 22, 2024, AND “Pennie Board Meeting Recording” and Pennie Board Meeting Deck” Aug. 8, 2024 ⤶

- ”Governor Josh Shapiro Executive Budget 2024-2025” Budget.pa.gov. February 6, 2024 ⤶

- ”Pennsylvania HB2234” BillTrack50. Legislation dead Dec. 31, 2024 ⤶

- ”Pennie Board Meeting Recording” and Pennie Board Meeting Deck” Pennie Board of Directors. Aug. 8, 2024 ⤶

- ”Pennsylvania HB2234” BillTrack50. Accessed Aug. 16, 2024 ⤶

- ”Pennie Board of Directors Meeting” Pennie.com. May 16, 2024 ⤶

- ”Fiscal Note, HB2234” Pennsylvania House Committee on Appropriations. June 5, 2024 ⤶

- ”2026 Final Gross Rate Changes – Pennsylvania: +21.5% (updated)” ACA Signups. Oct. 15, 2025 ⤶ ⤶

- ”Coverage Areas for 2027 Individual Market Plans” PA.gov. Accessed July 29, 2026 ⤶

- “Shapiro Administration Announces Proposed 2026 Health Insurance Rate Updates” Pennsylvania Insurance Department. Aug. 1, 2025 ⤶

- ”Estimated monthly premium for 2026 and 2025” (zip 19132) Pennie. Accessed Nov. 1, 2025 ⤶

- ”Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums” The Commonwealth Fund. December 2014. ⤶

- ”Pennsylvania: APPROVED 2016 Avg. Rate Hike: 12.0% (Reduced From 15.6%)” ACA Signups. October 2015. ⤶

- ”ACA Rates Q&A” Pennsylvania Insurance Department. Accessed October 2023. ⤶

- ”Rate Change Request Summary – 2019” Pennsylvania Insurance Department. Accessed October 2023. ⤶

- ”Pennsylvania: *Final* 2020 Avg. #ACA Exchange Rate Changes: 3.8% Increase” ACA Signups. October 2019. ⤶

- ”PA’s ACA Marketplace Rates to Decrease by an Average of 3.3% in 2021“ACA Signups. October 2020. ⤶

- ”Pennsylvania: Approved 2022 #ACA Rate Changes: +0.2% Individual Market, +4.8% Sm. Group Market” ACA Signups. October 2021. ⤶

- ”Pennsylvania: Final 2023 Unsubsidized #ACA Rate Changes: +5.5% (Down From +7.1%)” ACA Signups. October 2022. ⤶

- ”Shapiro Administration Announces 2024 Health Insurance Rates” Pennsylvania Pressroom. September 28, 2023. ⤶

- ”Affordable Care Act Health Rate Filings” Pennsylvania Insurance Department. Accessed Dec. 18, 2024 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “2023 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶