Find Colorado Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Colorado Health Insurance Marketplace Guide

This guide, including the FAQs below, is designed to help you understand your Colorado health insurance options and possible financial assistance available to you and your family — including federal subsidies and Colorado’s state-funded subsidies.

Colorado created its own state-based health insurance exchange (Marketplace), called Connect for Health Colorado. This platform allows residents to shop for individual and family health plans offered by six private health insurance carriers.1 There will be some changes in carrier participation for 2027, with one insurer exiting Colorado’s Marketplace and another joining (details below).

The Colorado Option debuted in 2023, bringing standardized plans and lower-cost coverage options to the state’s market. During the open enrollment period for 2026 coverage, half of Colorado Marketplace enrollees selected Colorado Option plans.2

Colorado is also among the states where state-funded subsidies are available, in addition to federal health insurance subsidies. As described below, Colorado’s state-funded subsidies changed from a cost-sharing reduction to a premium subsidy for plan year 2026, with additional funding added to offset some of the subsidy losses stemming from the expiration of the federal subsidy enhancements at the end of 2025.

Undocumented immigrants can access state-funded subsidies in Colorado by enrolling in OmniSalud via the Colorado Connect platform, although the number of spots available in this program is limited and was significantly reduced for 2026, due to funding cuts.3 OmniSalud’s financial assistance was only available to 6,700 people for 2026, and eligibility was determined on a lottery basis.4

Colorado has a reinsurance program that keeps full-price premiums lower than they would otherwise be,5 although funding for this program was reduced starting in 2026, due to the sunsetting of the federal premium subsidy enhancements.1

Colorado also has an easy enrollment program that allows people to access health coverage via the state tax return.6

Colorado ACA Marketplace quick facts

Frequently asked questions about health insurance in Colorado

Who can buy Marketplace health insurance in Colorado?

To sign up for private health insurance through Connect for Health Colorado, you must:9

- Be a resident of Colorado

- Not be incarcerated

- Not be enrolled in Medicare

- Be lawfully present in the United States. (Colorado has created a separate platform that undocumented residents can use to enroll in state-subsidized health coverage,10 but funding for this program declined for 2026, making fewer people eligible for the state-funded subsidies.)3

So most Colorado residents are eligible to enroll in coverage through the exchange. But a bigger question for most people is financial assistance, and a few additional parameters must be met to qualify for subsidies through Connect for Health Colorado.

To qualify for income-based Advance Premium Tax Credits (APTC), federal cost-sharing reductions (CSR), or Colorado’s state-funded subsidies,11 you must:

- Not have access to affordable employer-sponsored health coverage. If you have access to an employer’s plan and aren’t sure whether it’s considered affordable, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies via Connect for Health Colorado.

- Not be eligible for Health First Colorado (Colorado Medicaid) or Child Health Plan Plus (CHP+), or premium-free Medicare Part A.12

- File a joint tax return if you’re married.13

- Not be able to be claimed by someone else as a tax dependent.13

Beyond those basic parameters, qualifying for subsidies through Connect for Health Colorado depends on how much your household earns and how that compares with the cost of the second-lowest-cost Silver plan in your area – which will depend on your age and location.

As described below, Colorado also offers additional state-funded subsidies for households with income up to 400% of the federal poverty level.11

When can I enroll in an ACA-compliant plan in Colorado?

For 2026 coverage in the individual/family market, Colorado’s open enrollment period ended on January 15, 2026.

For 2027 coverage, open enrollment will run from November 1, 2026 to December 31, 2026.14 All policies selected during open enrollment will take effect January 1, and there will no longer be an option for a February 1 effective date without a qualifying life event.

The shorter open enrollment period and January 1 effective date for all plans are due to a federal rule change that was finalized in 2025.

Outside of the annual open enrollment period, you may be eligible to enroll or make a plan change if you experience a qualifying life event, such as giving birth or losing other health coverage.

As of 2024, Colorado joined several other states that consider pregnancy to be a qualifying event.15 This allows uninsured pregnant women the opportunity to enroll in health coverage without having to wait until the baby is born.

Enrollment in Health First Colorado (Medicaid) and Child Health Plan Plus (CHP+) is available year-round.16

How do I enroll in a Colorado Marketplace plan?

To enroll in an ACA Marketplace/exchange plan in Colorado, you can:

- Visit Connect for Health Colorado, which is Colorado’s health insurance Marketplace. This online platform will allow you to compare available health plans, determine whether you’re eligible for financial assistance, and enroll in coverage, either during open enrollment or during a special enrollment period.

- Enroll in a Connect for Health Colorado plan with the help of an insurance broker or certified enrollment assister.17

You can reach Connect for Health Colorado’s call center at 855-752-6749 (TTY line: 855-346-3432)

How can I find affordable health insurance in Colorado?

Under the Affordable Care Act (ACA), income-based federal subsidies (APTC) are available to lower the amount you pay for your health coverage each month. These subsidies are available to enrollees who meet the eligibility requirements and select a health plan through Connect for Health Colorado.

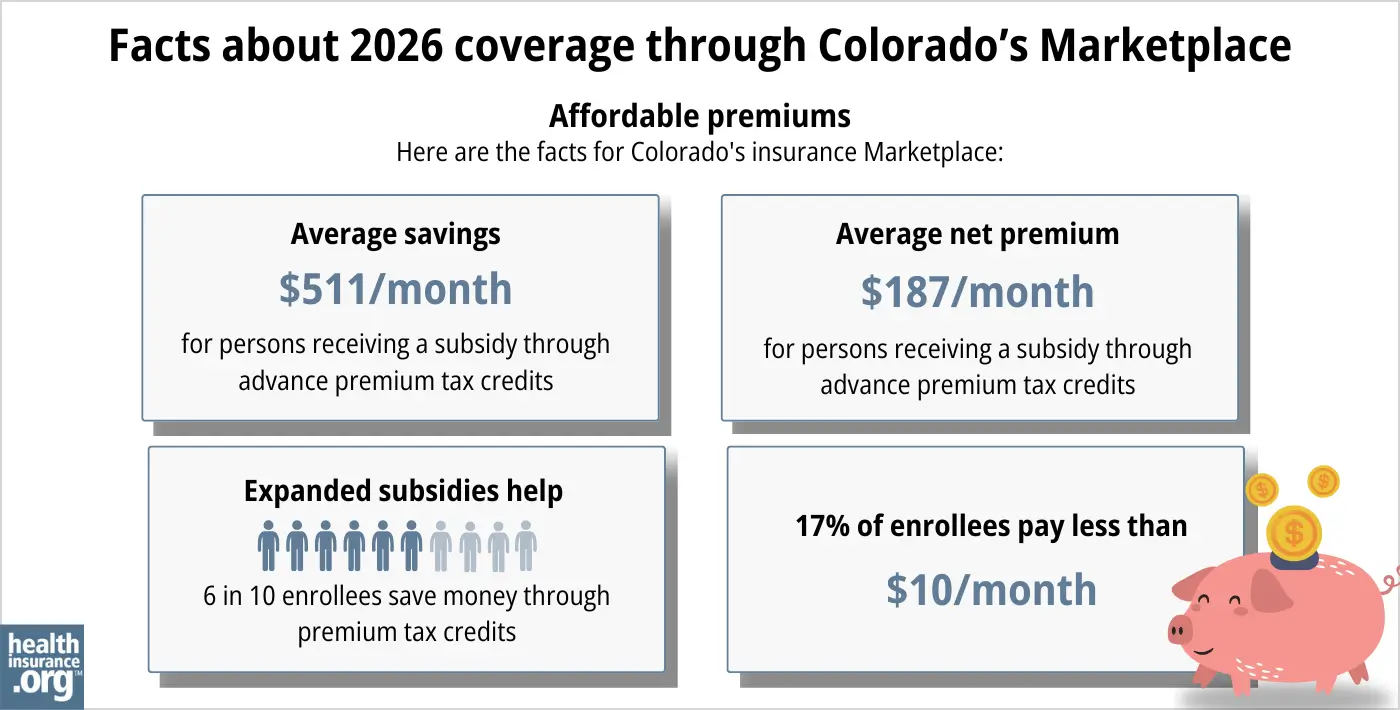

Almost seventy percent of Connect for Health Colorado enrollees were receiving APTC as of early 2026. For these consumers, the average after-subsidy premium (before accounting for Colorado’s additional state-funded subsidies, described below) was about $187/month.18 When we include Colorado’s state-funded subsidies, the average enrollee who receives both state and federal subsidies is paying about $131/month for their coverage.2

Source: CMS.gov 18

Federal premium subsidies don’t cover as much of enrollees’ total premiums in 2026 as they did in 2025, and they are no longer available to households with income above 400% of the federal poverty level. This is because Congress did not extend the federal subsidy enhancements that had been making coverage more affordable since 2021.

To mitigate some of the impact of the expiration of the federal subsidy enhancements, Colorado’s additional state-funded subsidy switched from an extra cost-sharing reduction to an extra premium subsidy for 2026. For enrollees with household income up to 400% of the federal poverty level, the state is providing an additional $80/month for the primary applicant (on top of their federal premium subsidies), plus an additional $29/month for other applicants on a family policy.11

Connect for Health Colorado reported that 176,410 enrollees were receiving the additional Colorado-funded subsidies in 2026.2

Cost-sharing reductions

If your household’s income doesn’t exceed 250% of the federal poverty level, you’ll also be eligible for federal cost-sharing reductions (CSR). This subsidy will reduce your deductible and other out-of-pocket expenses as long as you select a Silver-level plan through the exchange. In 2026, almost 27% of Connect for Health Colorado enrollees were receiving CSR benefits.19

In 2025, Colorado also offered additional cost-sharing subsidies to silver-plan enrollees with household income up to 200% of the federal poverty level.20). As noted above, these extra cost-sharing reductions are no longer available as of 2026, as the state switched to an additional premium subsidy instead.

If you’re eligible for both APTC and CSR, you can use them both if you enroll in a Silver-level plan through Connect for Health Colorado. (APTC and Colorado’s 2026 state-funded premium assistance can be used with any metal-level plan, but CSR benefits are only available if you enroll in a Silver plan.)

Colorado Option (public option) plans provide value

Many Connect for Health Colorado enrollees find that Colorado Option plans present the best overall value. These public option plans accounted for half of the state’s Marketplace enrollments in 2026.2 They come with lower premiums than many other plans, as well as lower out-of-pocket costs for various services.21

Health First Colorado (Medicaid) or CHP+

Depending on your income and circumstances, you may be able to enroll in free or low-cost health coverage through Health First Colorado (Medicaid) or CHP+. Learn more about whether you might be eligible for these programs in Colorado.

OmniSalud: Health insurance access for undocumented immigrants

Starting in 2023, Colorado began providing state-funded premium and cost-sharing assistance to undocumented immigrants who enroll through a new public benefit corporation (Colorado Connect/OmniSalud) that the state has created.22 This is separate from Colorado’s health insurance exchange, as undocumented immigrants are not eligible to use an ACA-created health insurance exchange.

In 2023, OmniSalud provided coverage to 10,000 enrollees, and the state announced that the program would be available to 11,000 people for 2024.23

But that 11,000 cap was reached in just the first two days of open enrollment for 2024 coverage.24 After the cap was reached, additional OmniSalud enrollments for 2024 were at full price.

There was no automatic re-enrollment, so people with coverage through OmniSalud in 2023 had to re-enroll during the open enrollment period for 2024 coverage. For 2025, however, Colorado officials said that people with existing OmniSalud coverage would have their spaces saved for 2025, giving them time to renew their coverage before new applicants were given access (if available) to the program.25

For 2025, Colorado officials announced that nearly 14,000 people enrolled in plans via Colorado Connect (the separate platform that Colorado established to facilitate OmniSalud enrollment), most of whom were OmniSalud enrollees.26

For 2026, due to funding cuts, the state only has enough money to subsidize OmniSalud enrollment for about 6,700 people. A lottery system was used to select the enrollees from among the people who were enrolled in subsidized OmniSalud plans in 2025.4

Colorado’s benchmark plan updates

Colorado updated its Essential Health Benefits Benchmark health plan as of 2023 (EHB benchmark plans dictate what must be covered under essential health benefit rules on individual and small group health plans).

Colorado’s changes to the benchmark plan for 2023 and future years include additional mental health coverage, expanded access to drugs that can be prescribed as alternatives to opioids, and up to six acupuncture treatments per year. And Colorado became the first state to explicitly include gender-affirming care in its benchmark plan.27 In addition, Colorado enacted legislation in 2025 that prevents health plans from “limiting or denying gender-affirming care that a doctor identifies as medically necessary.”28

But HHS finalized a rule change in 2025 that prohibits health plans from covering gender affirming care as an essential health benefit (EHB), starting in 2026.29 Federal premium subsidies can only be used to pay for coverage of EHBs, so this rule could result in either enrollees or the state having to pay the portion of the premiums that are associated with gender-affirming care.30

How many insurers offer Marketplace coverage in Colorado?

Six insurers offer 2026 coverage in Colorado’s health insurance Marketplace, with coverage areas that vary by insurer:1

- Cigna Health and Life Insurance (plans will not be available after 2026)

- Denver Health Medical Plan, Inc

- SelectHealth

- Kaiser Foundation Health Plan of Colo.

- Anthem (HMO Colorado)

- Rocky Mountain HMO

For 2027, there will be some changes in carrier participation in Colorado’s Marketplace:

- Cigna will no longer offer coverage.

- Colorado Access is joining the Marketplace, offering plans in 14 counties.31

Although there will be some changes for 2027, Colorado’s Marketplace carrier participation in 2026 is the same as it was in 2025 and 2024.32

For 2024, SelectHealth joined the health insurance exchange in Colorado, with plans available mostly along the Front Range.33 SelectHealth already offered plans in the exchange in Utah, Idaho, and Nevada. Their expansion into Colorado was due to a merger between Intermountain Health (SelectHealth is Intermountain’s insurance arm) and Colorado-based UCHealth.34

Friday Health Plans offered coverage in early 2023, but stopped accepting new enrollees in May and all FHP policies in Colorado terminated on August 31, 2023.35

Are Marketplace health insurance premiums increasing in Colorado?

For 2027, the following average rate changes have been proposed by Colorado’s individual/family insurance carriers, amounting to a weighted average increase of about 11%, before subsidies.36

Colorado’s ACA Marketplace PROPOSED 2027 Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Cigna Health and Life Insurance | Exiting market |

| Colorado Access | New for 2027 |

| Denver Health Medical Plan, Inc | 18.3% |

| SelectHealth | 15% |

| Kaiser Foundation Health Plan of Colo. | 10.2% |

| Anthem (HMO Colorado) | 10.3% |

| Rocky Mountain HMO | 23.9% |

It’s important to keep in mind that average rate changes apply to full-price rates, and most enrollees do not pay full price: Almost 70% of the people enrolled through Connect for Health Colorado were receiving federal premium subsidies in 2026, 19 and most of those enrollees were also receiving Colorado’s state-funded premium subsidies.2

However, the expiration of the subsidy enhancements has had a chilling effect on Marketplace enrollment in 2026, with fewer people signing up for coverage.37 Insurers know that healthy people are the most likely to drop their coverage when net (after-subsidy) premiums increase, so the overall risk pool was projected to be smaller and sicker, leading to higher gross (pre-subsidy) premiums across the board. Colorado regulators noted that the average net premium increase in Colorado was projected be 101% as a result of the expiration of the subsidy enhancements.38

The 2026 rate increases were the largest since 2018 (details below), and state regulators noted that the rate increases were due in large part to Congressional Republicans’ failure to extend the subsidy enhancements that had driven record-high enrollment in recent years.1

This was mitigated somewhat by Colorado’s supplemental state-funded premium subsidies, and also because some people downgraded to Bronze plans in order to lower their monthly premiums.

The impact of the expiration of the subsidy enhancements was more significant for older enrollees, for people in areas of the state where health insurance is more expensive, and for people earning more than 400% of the poverty level (who lost their federal subsidies and also aren’t eligible for Colorado’s new state-funded premium subsidies). For example, consider a 60-year-old who lives in Crested Butte, Colorado and earns $63,000 per year. Here’s a summary of the lowest-cost plans available to this person through the Colorado Marketplace in 2025 and 2026:39

- Lowest-cost plan in 2025: $36/month

- Lowest-cost plan in 2026: $1,282/month

Here’s a summary of how Colorado health insurance plans’ average full-price premiums have changed over the years in the individual/family market:

- 2015: Average increase of 0.71%40

- 2016: Average increase of 9.84%41

- 2017: Average increase of 20.4%42

- 2018: Average increase of 34.3%43 (including loss of federal CSR funding)

- 2019: Average increase of 5.6%44

- 2020: Average decrease of 20%45 (reinsurance program took effect)

- 2021: Average decrease of 1.4%46

- 2022: Average increase of 1.1%47

- 2023: Average increase of 10.4%48

- 2024: Average increase of 9.7%49

- 2025: Average increase of 5.6%50

- 2026: Average increase of 21.2%51

How many people are insured through Colorado’s Marketplace?

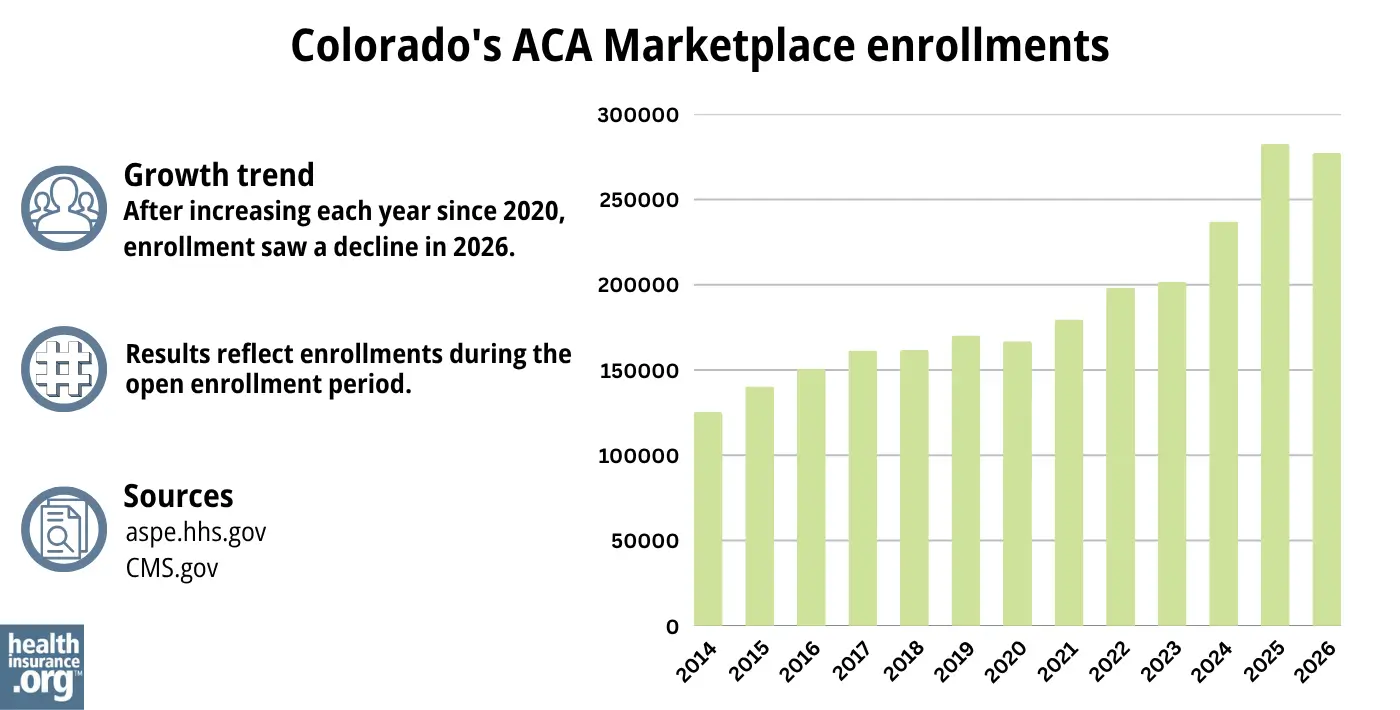

277,238 people enrolled in private plans through Connect for Health Colorado during the open enrollment period for 2026 coverage.18

Connect for Health Colorado had record-high enrollment in 2025, but enrollment declined in 2026 due to the expiration of federal subsidy enhancements. But Colorado’s state-funded subsidies helped to offset some of the reduction in federal subsidies, preventing a more significant decline in enrollment.52

Source: 2014,53 2015,54 2016,55 2017,56 2018,57 2019,58 2020,59 2021,60 2022,61 2023,62 2024,63 202564 202618

The increase in enrollment from 2021 through 2025 was largely due to the enhancements of federal subsidies under the American Rescue Plan and Inflation Reduction Act, as well as Colorado’s investment in additional state-funded subsidies.

In addition, enrollment growth in 2024 and 2025 was partly due to the “unwinding” of the pandemic-era continuous coverage rule for Medicaid. People were not disenrolled from Medicaid for three years, but disenrollments resumed in mid-2023. CMS reported that 20,815 Colorado residents transitioned from Medicaid to a Connect for Health Colorado plan during the unwinding process65

What health insurance resources are available to Colorado residents?

Connect for Health Colorado: This is the Marketplace/exchange in Colorado. Residents can use Connect for Health Colorado to enroll in individual/family health plans and receive income-based subsidies, and also to enroll in Health First Colorado. You can contact Connect for Health Colorado at 855-752-6749

OmniSalud/Colorado Connect: This state-based platform allows undocumented immigrants to sign up for health coverage. Depending on an applicant’s income and the number of people who have already enrolled, state-funded premium and cost-sharing subsidies may be available.

Colorado Division of Insurance: Regulates the insurance industry in Colorado, and assists consumers and businesses with insurance-related questions and concerns.

Colorado Department of Health Policy and Financing (HCPF): Administers Medicaid (Health First Colorado), Child Health Plan Plus (CHP+) and other health care programs.

Colorado Senior Health Care and Medicare Assistance: A service for Colorado Medicare beneficiaries and their caregivers, providing information and assistance with questions related to Medicare eligibility, enrollment, and claims.

Looking for more information about other options in your state?

Need help navigating health insurance options in Colorado?

Explore more resources for options in CO including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”Chaos from Congressional Republicans Leads to Average Premium Increases of Over 28% for 2026” Colorado Department of Regulatory Agencies. July 16, 2025 ⤶ ⤶ ⤶ ⤶

- ”Plan Year 2026 Open Enrollment Report” Connect for Health Colorado. Accessed May 27, 2026 ⤶ ⤶ ⤶ ⤶ ⤶

- ”Health Insurance Affordability Board Meeting” (Slide 13). Colorado Health Insurance Affordability Enterprise. June 13, 2025 ⤶ ⤶

- ”SilverEnhanced Savings” Connect for Health Colorado. Accessed Nov. 13, 2025 ⤶ ⤶

- ”Polis-Primavera Administration’s Landmark Reinsurance Program to Save Coloradans $477 Million on Premiums in 2025” Colorado Division of Insurance. July 17, 2024 ⤶

- ”Health Care Coverage Easy Enrollment Program” Colorado General Assembly. Enacted 2020. ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Chaos from Congressional Republicans Leads to Average Premium Increases of Over 28% for 2026” Colorado Department of Regulatory Agencies. July 16, 2025 *The above is based on the most current data available. ⤶

- ”Who can sign up?” Connect for Health Colorado, accessed August 2023 ⤶

- “OmniSalud” Connect for Health Colorado, accessed Mar. 27, 2026 ⤶

- ”New Financial Help Available: Colorado Premium Assistance” Connect for Health Colorado. Accessed Nov. 13, 2025 ⤶ ⤶ ⤶

- “Lower Your Monthly Premiums” Connect for Health Colorado, accessed Nov. 13, 2025 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Nov. 13, 2025 ⤶ ⤶

- Confirmed via email by Connect for Health Colorado, Apr. 28, 2026 ⤶

- “HB22-1289: Health Benefits for Colorado Children and Pregnant Persons” Colorado General Assembly. Enacted June 7, 2022. ⤶

- “Is there an open enrollment period for Health First Colorado?” Health First Colorado, July 17, 2016. Accessed Nov. 13, 2025 ⤶

- “Need Help with Your Health Coverage? Find Enrollment Assistance and More Using Connect for Health Colorado’s Certified Experts” Connect for Health Colorado. Accessed Nov. 13, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” Centers for Medicare & Medicaid Services, Accessed April 2026 ⤶ ⤶ ⤶ ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” Centers for Medicare & Medicaid Services. Accessed May 27, 2026 ⤶ ⤶

- ”Colorado Health Insurance Affordability Board Meeting Minutes” Colorado Health Insurance Affordability Enterprise. April 19, 2024 ⤶

- ”Colorado Option” Colorado Department of Regulatory Agencies. Accessed May 27, 2026 ⤶

- “Colorado Division of Insurance looking for public health AmeriCorps members to join Enroll for Health Colorado” Colorado Division of Insurance, accessed August 2023 ⤶

- ”OmniSalud program will provide $0 premium health plans to 11,000 qualified individuals” Colorado Division of Insurance. October 2023. ⤶

- OmniSalud Financial Help Spots Claimed for 2024. Connect for Health Colorado. November 2, 2023. ⤶

- ”Health Insurance Affordability Board Meeting” (board meeting slides) Colorado Health Insurance Affordability Enterprise. May 17, 2024 ⤶

- ”Connect for Health Colorado Sets a New Record: 282,483 People Enrolled in Health Insurance for Plan Year 2025” Connect for Health Colorado. Jan. 23, 2025 ⤶

- ”Biden Administration Announces Approval of Colorado’s Inclusive Health Care Plan to Set Colorado’s Essential Health Benefits” Colorado Department of Regulatory Agencies. October 12, 2021. ⤶

- ”Gov. Jared Polis signs bill protecting gender-affirming care coverage in Colorado” Colorado Newsline. May 23, 2025 ⤶

- ”Patient Protection and Affordable Care Act; Marketplace Integrity and Affordability, Prohibition on Coverage of Specified Sex-Trait Modification Procedures as an EHB” U.S. Department of Health & Human Services. June 25, 2025 ⤶

- ”New Federal Rules Affecting Coverage of Treatment for Gender Dysphoria: Considerations for States” State Health & Value Strategies, Princeton University. Aug. 1, 2025 ⤶

- ”Colorado Access to Join Colorado’s Individual Market in Plan Year 2027” Colorado Division of Insurance. Mar. 18, 2026 ⤶

- “Polis Administration’s Landmark Health Insurance Programs Continue to Deliver Millions in Savings for Coloradans” Colorado Division of Insurance, July 20, 2023 ⤶

- “Two Colorado health care giants are forming one big insurance network. But will consumers actually benefit? ” Colorado Sun, Jan. 24, 2023 ⤶

- “Intermountain Healthcare and SCL Health Complete Merger” SCL Health, April 5, 2022 ⤶

- “Frequently Asked Questions (FAQs) for Customers Losing Friday Health Plans Coverage as of August 31, 2023” Colorado Division of Insurance, Aug. 3, 2023 ⤶

- “ACA Health Insurance Premiums for Individuals Expected to Increase by 11% in 2027” Colorado Division of Insurance. July 22, 2026 ⤶

- ”ACA Marketplace Enrollment is Down in 2026—But All of the Data Isn’t in Yet” KFF.org. Feb. 5, 2026 ⤶

- ”Congressional Inaction Leads to An Average Doubling of Health Insurance Costs for 225,000 Hardworking Coloradans” Colorado Department of Regulatory Agencies. Oct. 27, 2025 ⤶

- ”Let’s find a plan for you” (zip code 81224) Connect for Health Colorado. Accessed Nov. 13, 2025 ⤶

- ”2015 Health Insurance Plans & Rates – Division of Insurance Rate Review FAQ” Colorado Division of Insurance. September 22, 2014. ⤶

- ”HB16-1336 Sen Donovan (Prime Sponsor), Sen Roberts (Co-Sponsor), “Study Geographic and Cost Drivers of Individual Health Plans”” Coloradokids.org Accessed October 2023. ⤶

- ”Dramatic Price Increases A Look at Colorado’s 2017 Individual and Small Group Insurance Premiums” Colorado Health Institute. September 2016. ⤶

- ”Colorado 2018 Individual Market Final Rate Changes ‐ No CSR Funding” Colorado Division of Insurance. Accessed October 2023. ⤶

- ”Colorado finalizes 2019 health insurance premium rates; some individuals could see rates fall” Denver 7 ABC News. October 2018. ⤶

- ”2020 Colorado Insurance Rates and the Role of Reinsurance” Colorado Health Institute. January 16, 2020. ⤶

- ”2021 individual health premiums decreasing by 1.4% over 2020 premiums” Colorado Division of Insurance. October 8, 2020. ⤶

- ”2022 Individual Consumer Impact” Colorado Division of Insurance. October 2021. ⤶

- ”Division of Insurance Works to Save Coloradans $326 million on Health Insurance in 2023” Colorado Division of Insurance. October 2022. ⤶

- ”2024 Individual Market – Reinsurance Impact By Carrier” Colorado Division of Insurance. October 2023. ⤶

- “Polis-Primavera Administration’s Landmark Reinsurance Effort Will Save Coloradans $493 Million on Healthcare Premiums in 2025, Putting Money Back in the Pockets of Hardworking Coloradans” Colorado Division of Insurance. Oct. 17, 2024 ⤶

- “2026 Final Gross Rate Changes – Colorado: +21.2% (updated)” ACA Signups. Oct. 23, 2025 ⤶

- ”Plan Year 2026 Open Enrollment Report” Connect for Health Colorado. Accessed Apr. 24, 2026 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, Accessed August 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶

- State-based Marketplace (SBM) Medicaid Unwinding Report. Centers for Medicare and Medicaid Services. Accessed Jan. 23, 2025; Data through September 2024 ⤶