Expert analysis of health reform issues

HMO vs PPO vs POS vs EPO: What’s the difference?

March 24, 2026 – The type of managed care your health plan falls under affects your healthcare costs and plan benefits – including access to medical…

I can’t afford health insurance and don’t qualify for Medicaid. What can I do?

March 16, 2026 – What can you do if health insurance feels unaffordable and you don’t qualify for Medicaid? Explore coverage options, subsidies, and…

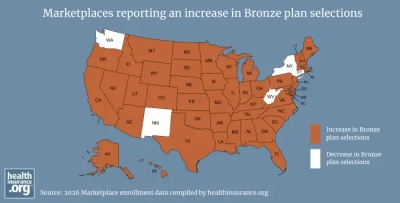

Bronze health plan popularity surges in Marketplaces

March 9, 2026 – Higher premiums and reduced subsidies are pushing Marketplace shoppers toward Bronze plans in 2026. Learn why enrollment is shifting and…

Your guide to early retirement health insurance options

March 2, 2026 – Health insurance for early retirees: how to bridge the gap to Medicare with Marketplace plans, Medicaid, COBRA, or spouse…

Marketplace enrollees face return of the ‘subsidy cliff’ in 2026

February 11, 2026 – Congress did not extend enhanced Marketplace subsidies at the end of 2025. Now, hundreds of thousands of Marketplace enrollees are…

How sunsetting ARP’s subsidy enhancements is affecting ACA subsidy amounts

January 30, 2026 – We look what's happening to Marketplace health insurance subsidy availability and size now that the subsidy enhancements instituted under…

8 big changes reshaping Marketplace health coverage in 2026

January 28, 2026 – On January 1, eight major changes took effect that are impacting ACA Marketplace coverage in 2026, affecting subsidies, premiums, HSAs,…

What can you do if you’re feeling Marketplace sticker shock?

January 9, 2026 – The expiration of ACA subsidy enhancements is driving higher 2026 Marketplace premiums. See who’s affected and what consumers can still…

50 populations whose lives are better thanks to the ACA

January 8, 2026 – Millions of Americans would have worse health insurance – or none at all – without Obamacare's provisions. But the law's protections…

How much do dental cleanings cost without insurance?

October 30, 2025 – Learn how much a dental cleaning costs without insurance, the factors that can impact the cost of dental cleaning, and whether you need…

2026 ACA open enrollment period preview

October 28, 2025 – Higher premiums and the expiration of enhanced premium subsidies top the list of 10 major changes that will affect Marketplace open…

Health insurance for the unemployed

September 29, 2025 – When it comes to obtaining health insurance for the self employed, consumers have several coverage options to consider, including ACA…