What is the Affordable Care Act (ACA)?

The Patient Protection and Affordable Care Act (PPACA) – also known as the Affordable Care Act or ACA, and often referred to as Obamacare – is the landmark health reform legislation passed by the 111th Congress and signed into law by President Barack Obama in March 2010.

What provisions are included under the ACA legislation?

The legislation includes a long list of health-related provisions that began taking effect in 2010. Key provisions extended coverage to millions of uninsured Americans, implemented measures to lower healthcare costs and improve system efficiency, and eliminated industry practices that include rescission and denial of coverage due to pre-existing conditions.

How did the ACA focus on improving the quality of health insurance?

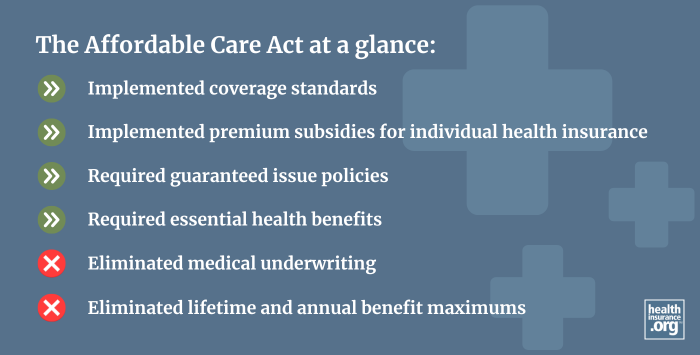

The ACA improved health insurance in numerous ways. Among other things, the ACA:

- implemented coverage standards that prevent insurers from discriminating against applicants – or charging them higher plan premiums – based on pre-existing conditions or gender;

- eliminated waiting periods that employer-sponsored plans could previously impose before covering pre-existing conditions (and imposed a 90-day cap on the allowable waiting period employers could require before offering coverage to new employees1);

- made health policies guaranteed issue – meaning health coverage is issued to applicants regardless of their health status, age or income;

- implemented a requirement that large employers offer affordable, minimum-value health coverage to their full-time employees (30+ hours per week), or potentially face a financial penalty;

- eliminated lifetime and annual benefit maximums for essential health benefits;

- improved plan benefits by requiring ACA-compliant individual/family and small group plans to include essential health benefits;

- required ACA-compliant plans to cover various preventive health care services without any cost-sharing.

How does the ACA make individual health insurance more affordable?

The law includes premium subsidies and cost-sharing reductions designed to reduce the costs of coverage and care for eligible applicants.

Find out if you're eligible for subsidies with our subsidy calculator, and keep in mind that premium subsidies have been enhanced through 2025 under the American Rescue Plan and Inflation Reduction Act, making them more robust than they were under the original ACA rules.

Millions have also gained coverage due to the ACA's expansion of Medicaid, which has been adopted by all but ten states as of 2024.

How do consumers buy ACA health insurance?

Consumers can use Obamacare's health insurance Marketplaces (exchanges) to easily compare the benefits and costs of private ACA-compliant / qualified health plans. These plans are categorized under metal level classifications based on actuarial value – and catastrophic plans are also available to eligible enrollees.

As of early 2024, nearly 21 million Americans were enrolled in private health plans obtained via the Marketplaces nationwide. More than nine out of ten were receiving premium subsidies, and half were also receiving cost-sharing reductions.2

When can people enroll in ACA-compliant health plans?

Millions of people enroll in ACA-compliant health plans during an annual open enrollment period (OEP) that runs from November 1 through January 15 in most states (some states have different schedules). People can also enroll outside of the OEP if they have a qualifying life event that makes them eligible for a special enrollment period.

Footnotes

- "Affordable Care Act Implementation FAQs - Set 16" CMS.gov. Accessed Oct. 9, 2024 ⤶

- "Effectuated Enrollment: Early 2024 Snapshot and Full Year 2023 Average" CMS.gov, July 2, 2024 ⤶