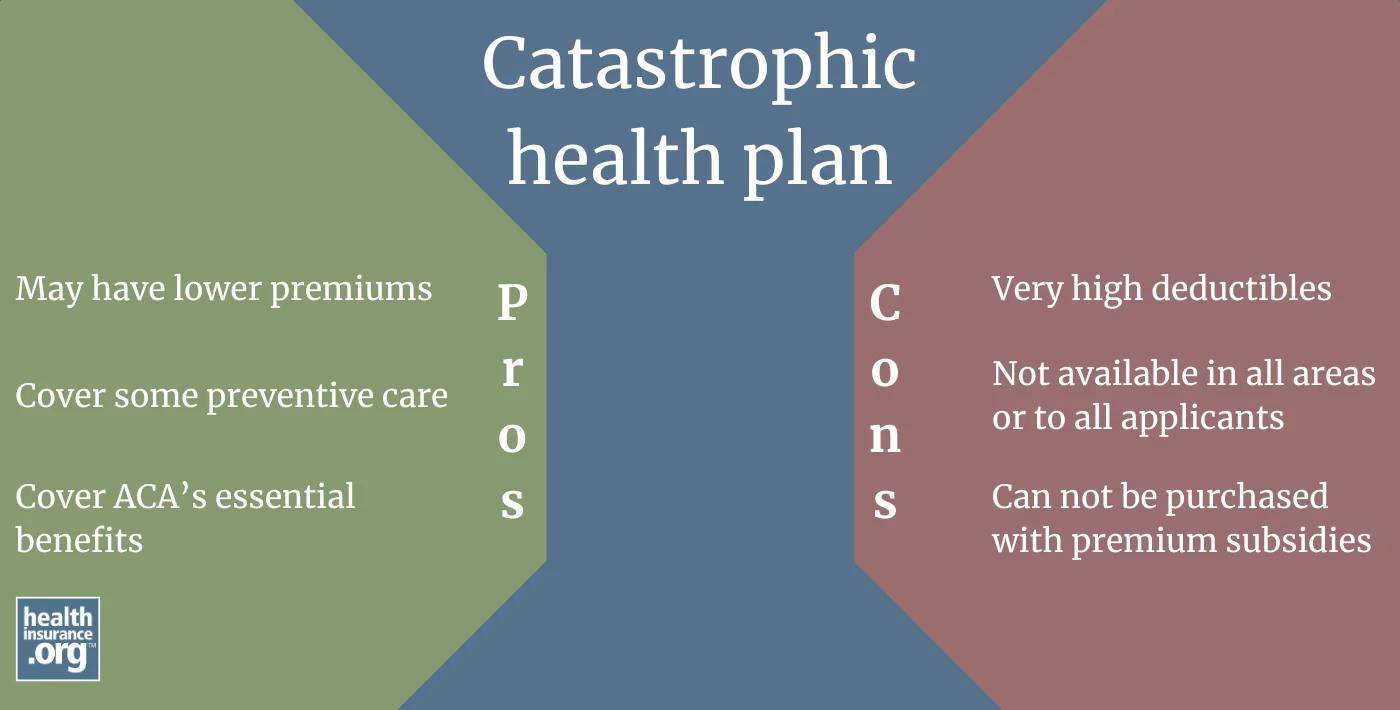

Catastrophic plan

What is a Catastrophic health insurance plan?

Although the term “Catastrophic plan” has long been used as a generic catch-all phrase to describe health insurance plans with high deductibles and little coverage for routine care, the Affordable Care Act assigned strict parameters to the term:

Catastrophic plans:

- are only available to certain applicants. (As detailed below, eligibility for these plans was expanded as of 2026.)

- have deductibles equal to the maximum annual out-of-pocket limit (see below about proposed changes for 2027 and future years),

- pay at least part of the cost of up to three primary care visits before the deductible is met,

- cannot be used with premium subsidies,

- are not offered by all carriers and are not available in all areas (in 2026, they're available in at least some parts of 36 states and DC)1

The specific requirements for Catastrophic plans are in the text of the ACA, section 1303(e).2

Are Catastrophic plans less expensive than Bronze plans?

This depends on the location and the specific plans in question. The short answer: Historically, Catastrophic plans were often less expensive than Bronze plans, although not always. And since not all carriers offer Catastrophic plans, the lowest-cost carrier in a given area doesn't always offer Catastrophic plans. And for 2026, changes in the availability of Catastrophic plans resulted in some insurers significantly increasing the premiums of these plans.

Here are the details, including some example premiums for 2026:

One of the reasons Catastrophic plans have tended to be less expensive is that for the ACA’s risk adjustment program, Catastrophic plans are in a separate risk pool from the metal-level plans,3 even though they’re in the same general shared risk pool.4 (The risk adjustment program transfers funds from carriers that insure healthier enrollees to carriers that insure sicker enrollees. This helps to stabilize the overall market, and removes the incentive for carriers to design plans that appeal more to healthy enrollees.)5

This means that within a state, Catastrophic plans transfer risk adjustment funds with other Catastrophic plans, but not with metal-level plans. This is one of the reasons Catastrophic plans have tended to have lower prices than Bronze plans. (The coverage they offer is quite similar to Bronze plans: Bronze plans cover an average of 56% - 62% of costs for a standard population,6 while Catastrophic plans must cover less than 60% of average costs,7 with the same maximum out-of-pocket limit that applies to other plans.

So because of the way the plans are grouped for risk adjustment, and because most Catastrophic plan enrollees have historically been under age 30 and fairly affluent – since income-based subsidies cannot be used with Catastrophic plans – these plans have generally had lower premiums than Bronze plans.8

However, that changed somewhat for 2026, as Catastrophic plans access was expanded (details below). As a result, insurers were allowed to refile premiums for 2026 coverage during a short window in late September 2025, to account for the fact that Catastrophic plans would be more widely available to older enrollees.9 As an example of the impact, North Dakota’s insurance department clarified that the expanded access to Catastrophic plans “resulted in much higher rate increases for 2026 than was originally anticipated for those plans."10

But there is considerable variation from one area to another. For example:

- A 50-year-old in Orlando, Florida, who doesn’t qualify for a 2026 Marketplace subsidy can get a Catastrophic plan for as little as $462/month, whereas the cheapest Bronze plan is $700/month.

- On the other hand, if this same person is in Houston, Texas, they can get a Bronze plan for as little as $523/month, but would have to pay $628/month to get the cheapest Catastrophic plan.11

The takeaway point: Don’t assume Catastrophic plans will be the cheapest option, even if you’re not eligible for a Marketplace subsidy. It will depend on where you live and the plans that are available to you.

Catastrophic plans: High deductibles, plus primary care and preventive care

- Catastrophic plans cover all of the essential benefits defined by the ACA, but with very high deductibles, equal to the annual limit on out-of-pocket costs under the ACA. For 2026, this is $10,600 for a single individual.12 For 2027, it will be $12,000 for a single individual.13

- However, CMS has proposed a rule change starting with the 2027 plan year, which would allow Catastrophic plans to have deductibles (and out-of-pocket maximums) equal to 130% of the out-of-pocket maximum that applies to other plans. If finalized for 2027, this would mean Catastrophic plans would have deductibles of $15,600, although CMS noted that a different amount could be finalized based on feedback they receive.14 (Note that the CMS proposal indicates that 130% of $12,000 is $15,400, but it's actually $15,600.)

- They must still limit members’ out-of-pocket costs for in-network services to no more than the annual out-of-pocket maximum that applies to all plans. This cap is $10,600 for an individual in 2026, and will be $12,000 for an individual in 2027. (This would change if the proposal for 2027 coverage is finalized to allow higher out-of-pocket maximums.)

- Catastrophic plans pay at least some of the cost of up to three primary care visits per year before the deductible is met. (Copays can apply for these visits, but at least part of the cost will be paid by the insurance company, even if you haven’t met your deductible.)

- Like all ACA-compliant plans, Catastrophic plans cover certain preventive care with no cost-sharing.

- Other services beyond preventive care and some primary care will be paid by the insured until the deductible is met. There is no coinsurance for Catastrophic plans, as the deductible is equal to the maximum allowable out-of-pocket limit.

Can I use premium subsidies to buy a Catastrophic plan?

No. An enrollee in a Catastrophic plan is not eligible for premium subsidies15 (and cost-sharing subsidies are also not available for Catastrophic plans, since those can only be obtained if you choose a Silver plan).

Depending on your income, you may be eligible for a premium subsidy that you could apply towards a metal-level plan. This may make a metal-level plan more affordable than a Catastrophic plan.16

Who can enroll in a Catastrophic plan?

Catastrophic plans are only available to people under age 30, or people 30 and older who qualify for a hardship/affordability exemption.17

Starting with the 2026 plan year, CMS made changes to allow more people to qualify for an automatic hardship exemption and thus be eligible to enroll in a Catastrophic plan.18 In most states, consumers whose projected household income makes them ineligible for premium tax credits are automatically eligible for a hardship exemption and thus allowed to enroll in Catastrophic coverage.

Because the federal subsidy enhancements were allowed to expire at the end of 2025, this includes anyone with a household income above 400% of the federal poverty level. It also includes people with household income below 100% of FPL, but these individuals only need Marketplace plans in nine states, as they're eligible for Medicaid expansion in the rest of the country. But Catastrophic plans are not available in all areas, so access also depends on where a person lives.1

The new hardship exemption provision also applies to people whose household income is above 250% of FPL (and thus ineligible for cost-sharing reductions). But if these individuals select a Catastrophic plan, they will be forfeiting their premium tax credits, as premium tax credits cannot be used with Catastrophic plans. So people with household income between 250% and 400% of the poverty level should compare the full-price cost of a Catastrophic plan (if any are available in their area) with the subsidized cost of metal-level plans, and determine what plan will best fit their needs and budget.

The expanded hardship exemption is available in all states that use the federally-run HealthCare.gov exchange platform, as well as all states that run their own exchange platforms except California, Connecticut, Maryland, and the District of Columbia (those four states have their own hardship exemption processes, whereas the rest of the state-run exchanges use HealthCare.gov’s exemption process).19

But CMS has proposed a rule change to amend 45 §155.605(d)(1) and make consumers in all states (including CA, CT, MD, and DC) eligible for a hardship exemption based on projected household income below 100% of FPL or above 250% of FPL.20

Starting in November 2025, HealthCare.gov began automatically displaying Catastrophic plans (where available) for applicants 30 and older if they entered an income above 400% of the 2025 poverty level. However, Catastrophic plans were not being automatically displayed when a person age 30+ projected an income above 250% of the poverty level but not above 400%. This was still the case as of February 2026.21

The first Trump administration previously expanded access to hardship exemptions in April 2018,22 allowing exemptions for people in areas where all plans cover abortions, areas where only one insurer (or zero insurers) offers plans in the exchange, or where a personal hardship is created due to the plan options available in the exchange.

In particular, the provision for people in areas where just one insurer offers plans in the exchange made a hardship exemption available to far more people, allowing them to potentially purchase a Catastrophic plan (albeit without premium subsidies, making this a realistic alternative only for people who aren’t otherwise eligible for subsidies). But insurer participation in the exchanges has increased significantly since 2018, with very few enrollees currently having access to just one insurer’s plans.23

Can I contribute to an HSA if I have a Catastrophic plan?

Starting in 2026, you can contribute to a health savings account (HSA) if you have a Catastrophic plan purchased through the health insurance Marketplace, and no additional health coverage. This is due to Section 71307 of H.R.124 (formerly called the "One Big Beautiful Bill Act," and now referred to as the "Working Family Tax Cut Legislation"),25 enacted in July 2025. But before 2026, enrollment in a Catastrophic plan did not allow a person to contribute to an HSA.

How many people enroll in Catastrophic plans?

During the open enrollment period for 2026 coverage, 67,489 people enrolled in Catastrophic plans through the Marketplaces nationwide, out of more than 23.1 million total enrollees.26 This was about 0.3% of total enrollment, which was up only slightly from the 0.2% the year before, when 54,109 people enrolled in Catastrophic plans, out of more than 24 million exchange enrollees nationwide.27

(People can enroll in Catastrophic plans outside the exchange, but off-exchange enrollment is quite low across all types of plans, and the same eligibility rules apply to Catastrophic plans on-exchange or off-exchange.)

So although the Trump administration took steps to expand access to Catastrophic plans for 2026 (and had projected that 3 million people would select these plans as a result),28 Catastrophic plans continued to account for only a tiny fraction of total Marketplace enrollment in 2026, with only a minuscule increase from 2025.

Why is Catastrophic plan enrollment so low?

There are various reasons that so few people enroll in Catastrophic plans, including:

- Most Marketplace enrollees are subsidy-eligible. In 2026, more than 20 million of the 23.1 million Marketplace enrollees were eligible for income-based premium subsidies.29 These enrollees would have had to forfeit their subsidy in order to select a Catastrophic plan.

- Catastrophic plans aren’t always the lowest-cost option for people who don’t get premium subsidies. This was already true in some areas before 2026, but it’s even more widespread in 2026, due to the fact that carriers were allowed to refile rates for Catastrophic plans after CMS announced the expanded eligibility rules (details above). For example, in Houston, Texas, a 45-year-old who isn’t eligible for Marketplace subsidies has access to two Catastrophic plans, with monthly premiums for $507 and $647. But they have access to numerous Bronze plans with premiums starting as low as $423/month.30 So although Catastrophic plan availability has been expanded for 2026, enrollment might not increase significantly.

- In some areas, there are no Catastrophic plans available. There are 14 states where no carriers offer Catastrophic plans in the Marketplace anywhere in the state for 2026.1 In the rest of the states, some carriers (but usually not all) offer Catastrophic plans, but might not have coverage areas that include the whole state. And in some areas, the lowest-cost insurer doesn’t offer Catastrophic plans, so even if other insurers do, the Bronze plan from the lowest-cost insurer might be less expensive than another insurer’s Catastrophic plan.

- Eligibility it limited. Although Catastrophic plans are now available to people age 30 and older who aren't eligible for ACA subsidies, these plans (even in areas where they're available) are not automatically displayed by plan comparison tools in state-run Marketplaces. And the process for obtaining an exemption is still cumbersome in state-run Marketplaces.31

Footnotes

- "Policy Changes Bring Renewed Focus on High-Deductible Health Plans" KFF.org. Jan. 5, 2026 ⤶ ⤶ ⤶

- “Compilation of Patient Protection and Affordable Care Act”111th Congress, Legislative Counsel. May 2010. ⤶

- “Summary Report on Individual and Small Group Market Risk Adjustment Transfers for the 2024 Benefit Year” Centers for Medicare & Medicaid Services. June 30, 2025 ⤶

- “HHS-Operated Risk Adjustment Methodology Meeting.” Centers for Medicare & Medicaid Services. March 2016. ⤶

- “Explaining Health Care Reform: Risk Adjustment, Reinsurance, and Risk Corridors” KFF.org. Aug. 17, 2016 ⤶

- “Patient Protection and Affordable Care Act; Marketplace Integrity and Affordability” (Levels of Coverage/Actuarial Value). Centers for Medicare & Medicaid Services. June 25, 2025 ⤶

- “What is actuarial value?” PeopleKeep. Feb. 4, 2025 ⤶

- “What is a catastrophic health insurance plan?” PeopleKeep. Sep. 19, 2024 ⤶

- “Additional Guidance on Qualified Health Plan Certification and City of Columbus v. Kennedy” Centers for Medicare & Medicaid Services. Sep. 23, 2025 ⤶

- “North Dakotans Could See Significant Health Insurance Premium Increases in 2026 if Federal Subsidies End” North Dakota Insurance & Securities Department. Oct. 15, 2025 ⤶

- “See Plans and Prices” (zip code 32789 and 77001) HealthCare.gov. Accessed Nov. 9, 2025 ⤶

- “Patient Protection and Affordable Care Act; Marketplace Integrity and Affordability” U.S. Department of Health and Human Services. June 25, 2025 ⤶

- "Premium Adjustment Percentage, Maximum Annual Limitation on Cost Sharing, Reduced Maximum Annual Limitation on Cost Sharing, and Required Contribution Percentage for the 2027 Benefit Year" Centers for Medicare & Medicaid Services. Jan. 29, 2026 ⤶

- "Patient Protection and Affordable Care Act, HHS Notice of Benefit and Payment Parameters for 2027; and Basic Health Program" Centers for Medicare & Medicaid Services. Feb. 11, 2026 ⤶

- “Explaining Health Care Reform: Questions About Health Insurance Subsidies” KFF.org. Oct. 25, 2024 ⤶

- “How to pick a health insurance plan — Catastrophic health plans” HealthCare.gov. Accessed Apr. 9, 2026 ⤶

- “Health coverage exemptions: Forms & how to apply” HealthCare.gov. Accessed Feb. 9, 2026 ⤶

- “Expanding Access to Health Insurance: Consumers to Gain Access to “Catastrophic” Health Insurance Plans in 2026 Plan Year” Centers for Medicare & Medicaid Services. Sep. 4, 2025 ⤶

- ”Guidance on Hardship Exemptions for Individuals Ineligible for Advance Payment of the Premium Tax Credit or Cost-sharing Reductions Due to Income, and Streamlining Exemption Pathways to Coverage” Centers for Medicare & Medicaid Services. Sep. 4, 2025 ⤶

- "Patient Protection and Affordable Care Act, HHS Notice of Benefit and Payment Parameters for 2027; and Basic Health Program" (Page 165) Centers for Medicare & Medicaid Services. Feb. 11, 2026 ⤶

- “See Plans & Prices” HealthCare.gov. Accessed Feb. 9, 2026 ⤶

- “Guidance on Hardship Exemptions from the Individual Shared Responsibility Provision for Persons Experiencing Limited Issuer Options or Other Circumstances” Centers for Medicare & Medicaid Services. April 9, 2018. ⤶

- “Plan Year 2025 Qualified Health Plan Choice and Premiums in HealthCare.gov Marketplaces” Centers for Medicare and Medicaid Services. October 25, 2024 ⤶

- “H.R.1" (Section 71307). Congress.gov. Enacted July 4, 2025 ⤶

- "Working Families Tax Cut Legislation" Medicaid.gov. Accessed Feb. 9, 2026 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” (Columns H and BV). Centers for Medicare & Medicaid Services. Mar. 27, 2026 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” (Columns H and BQ). Centers for Medicare & Medicaid Services. May 2025 ⤶

- "Expansion of HSA Eligibility Under OBBB Act to Improve Marketplace Coverage, Affordability, and Access" White House Council of Economic Advisors. Sep. 2025 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” (Columns H and AO). Centers for Medicare & Medicaid Services. Mar. 27, 2026 ⤶

- “See Plans and Prices” (zip code 77001) HealthCare.gov. Accessed Nov. 9, 2025 ⤶

- “Health coverage exemptions: Forms & how to apply” HealthCare.gov. Accessed Apr. 9, 2026 ⤶