Consumer Operated and Oriented Plan (CO-OP)

What is a Consumer Operated and Oriented Plan (CO-OP)?

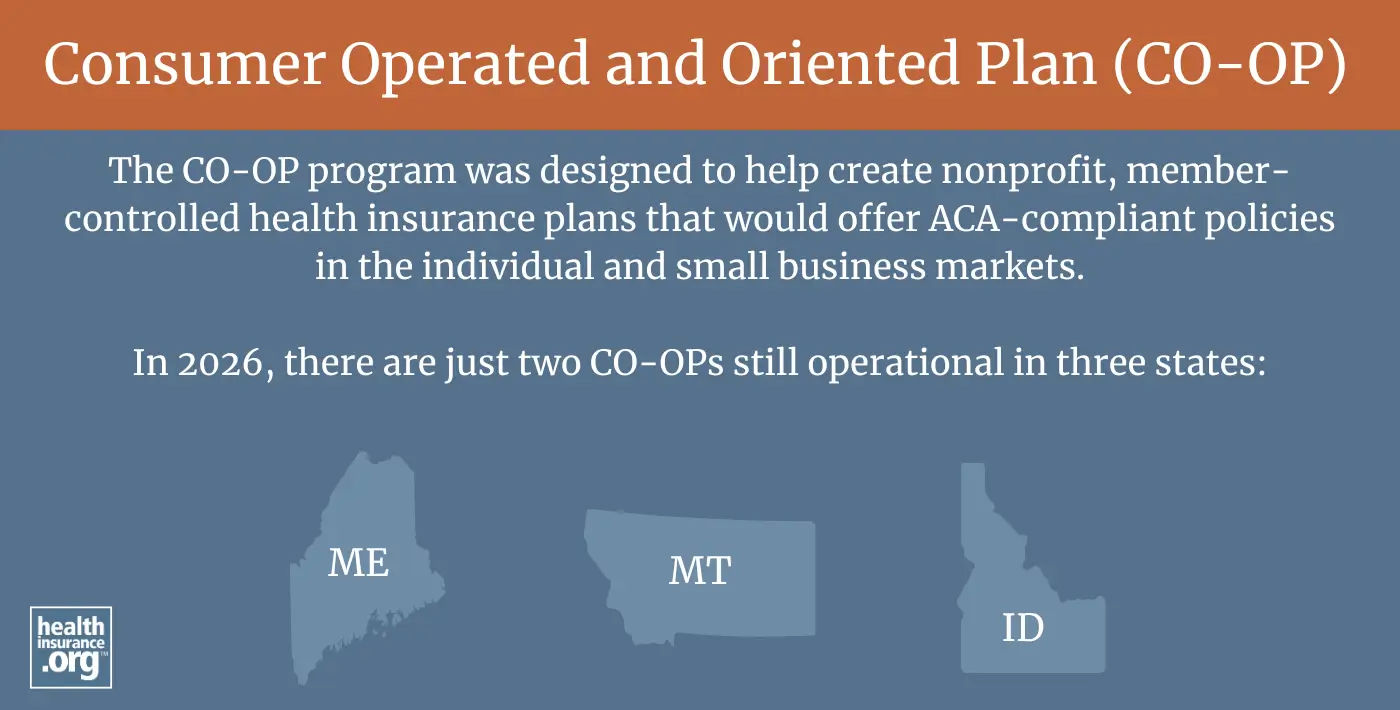

Created by the Affordable Care Act, the CO-OP (Consumer Operated and Oriented Plan) program was designed to help create nonprofit, member-controlled health insurance plans that would offer ACA-compliant policies in the individual and small business markets.

How many states still have ACA CO-OPs?

Twenty-four states had CO-OP plans available in their exchanges starting in October 2013. But nearly all of them have since closed. As of 2026, there are just two CO-OPs still operational in three states:

- Community Health Options in Maine

- Mountain Health CO-OP (Montana Health CO-OP) in Montana and Idaho

CO-OP coverage was available in four states in 2025, but Mountain Health CO-OP exited the Wyoming market at the end of 2025.1 So Mountain Health CO-OP plans are only available in Montana and Idaho for 2026.2

Common Ground Healthcare, which offers Marketplace plans in eastern Wisconsin in 2026,3 used to be an ACA-created CO-OP. But Common Ground became affiliated with CareSource in 2025,4 and CareSource now has “exclusive authority to appoint all members of the board of directors” of Common Ground,5 meaning it is no longer a member-controlled CO-OP.

CO-OPs were initially supposed to get $10 billion in federal grant money, but that was ultimately changed to $6 billion in loans, with fairly short repayment timelines. CO-OPs also fell victim to the risk corridors fiasco in far greater numbers than long-established health insurance companies. And the ACA’s risk adjustment program was also challenging for CO-OPs.

When can I enroll in a CO-OP?

CO-OPs are just like any other ACA-compliant individual market health plan, which means you can enroll during the annual open enrollment period or during a special enrollment period. This is true regardless of whether you’re enrolling through the Marketplace/exchange or directly through the CO-OP.

- Montana uses HealthCare.gov as their Marketplace, with open enrollment that runs from Nov. 1 to Dec. 15.

- Maine and Idaho run their own health insurance Marketplaces (CoverME and Your Health Idaho). CoverME has not yet announced open enrollment dates for 2027 coverage as of mid-2026, but the enrollment window will not be allowed to extend past December 31, 2026, under new federal rules. Your Health Idaho has a different schedule – Oct. 15 to Dec. 15.6

Special enrollment periods usually require a qualifying life event, although Native Americans can enroll in Marketplace coverage year-round in every state.

Note that if you work for a small business in a state where one of the remaining CO-OPs offers small-group health insurance, your employer might purchase group coverage from the CO-OP. They can do this at any time of the year, but your ability to enroll in the plan will be limited to your initial eligibility window, the annual open enrollment period designated by your employer, or a special enrollment period triggered by a qualifying life event.

Read more about CO-OP health insurance plans.

Footnotes

- “Your Health Coverage with us in Wyoming is ending on December 31, 2025” Mountain Health CO-OP. Accessed Aug. 18, 2025 ⤶

- “Mountain Health Co-Op insurance provider to cease coverage for Wyoming residents" Insurance News Net. Aug. 15, 2025 ⤶

- “CareSource Marketplace brochure, Wisconsin" CareSource. Accessed June 2, 2026 ⤶

- “CareSource, Common Ground Healthcare Cooperative affiliation approved” CareSource. Jan. 2, 2025 ⤶

- “In the Matter of the Acquisition of Control of Common Ground Healthcare Cooperative (NAIC #15061) by CareSource” CareSource Counsel. May 20, 2024 ⤶

- “Apply and Enroll” YourHealthIdaho. Accessed Aug. 18, 2025 ⤶