flexible spending account (FSA)

What is a flexible spending account (FSA)?

A flexible spending account (FSA) is a tax-advantaged account maintained by employers where employees can set aside a portion of each paycheck to pay for out-of-pocket medical expenses. No payroll taxes are due on funds allocated to an FSA, and the employee can use the money, tax-free, to pay for qualified medical expenses throughout the year.

FSAs can be used in conjunction with any type of health plan (unlike HSAs, which can only be contributed to if the person has coverage under an HSA-qualified high-deductible health plan).

Learn about how an FSA differs from an HSA.

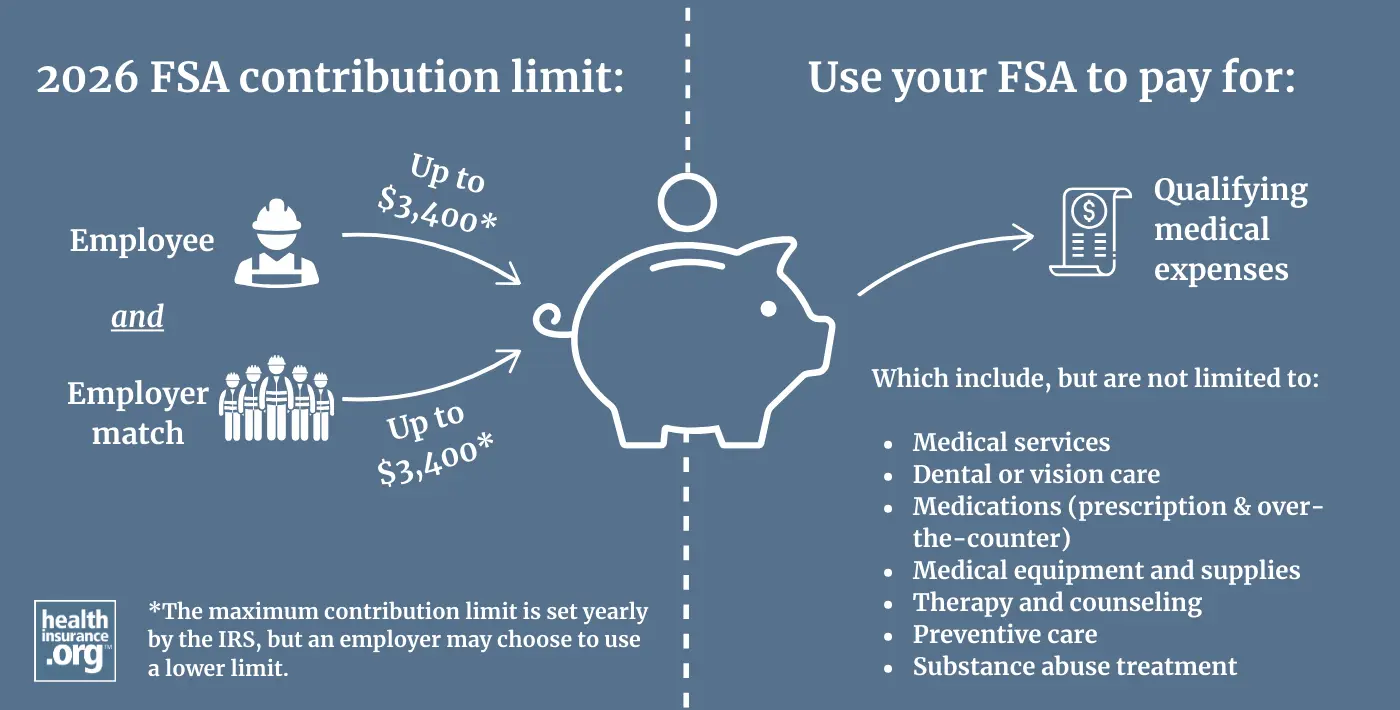

How much can you contribute to an FSA?

Starting in 2013, the Affordable Care Act capped the amount that workers can set aside in their FSAs. In 2026, the cap is $3,400,1 up from $3,300 in 2025.2 Employers have the option of setting lower (but not higher) limits than the IRS allows.

If your employer offers a medical FSA, you can choose to contribute any amount up to the limit that your employer sets. And if your spouse is also offered an FSA by their employer, they have the option to contribute as well, potentially increasing your total household FSA contributions to as much as $6,800 in 2026.3

Can an employer contribute to their employees' FSAs?

Yes, an employer can contribute to an employee's FSA. If the employer contributes, they can contribute up to $500 even if the employee contributes nothing at all. But pre-tax employer contributions above $500 are limited to a dollar-for-dollar match. For example, if the employee contributes $1,000, the employer could not contribute more than $1,000. But if the employee only contributes $200, the employer could contribute up to $500.4

So the maximum allowable total contribution would be double the limit that the IRS sets for employee salary reductions, assuming the employer allows the employee to contribute up to the maximum and also provides a dollar-for-dollar match.

When can you make changes to your FSA contribution?

Employees have to decide before the start of the plan year (during their employer's open enrollment period) whether they want to contribute to their FSA, and if so, how much they want to contribute. The amount is then divided out across the employee's paychecks for the whole year, although the full amount is available for withdrawal as of the first day of the plan year.

Employees can only start, stop, or change FSA contributions during the plan year if they have a qualifying life event.

What happens to unused money in an FSA?

There is a "use-it-or-lose-it" requirement with FSAs: Any money left in the account at the end of the plan year (or by March 15th of the following year if the employer offers a grace period) is lost to the employee. So it's important to only allocate for expenses that you know you'll incur.

However, employers also have the option to let enrollees carry over some unused money into the next year. The maximum amount that can be carried over to the coming year is set by the IRS each year. Up to $680 can be carried over from 2026 to 20271 (up from $660 that could be carried over from 2025 to 2026)2

Again, this is optional for employers, and they do not have to allow a grace period or carryover option. And they cannot offer more generous carry-over or grace period provisions than the IRS allows.

What can FSA funds be used for?

FSA funds can be used for qualified medical expenses. But employers can set more restrictive limits on what expenses can be reimbursed, meaning that a given FSA might not allow reimbursements for all expenses that the IRS considered qualified medical expenses.2 In addition, some services may require a letter of medical necessity from a doctor in order to be eligible for reimbursement by an FSA.5

As of 2011, the ACA prohibited the purchase of over-the-counter medications with FSA funds, unless a doctor prescribed them. But Section 4402 of the 2020 Coronavirus Aid, Relief, and Economic Security (CARES) Act changed that. The CARES Act eliminated subsection (f) of Section 106 of the Internal Revenue Code. That section had previously prohibited the purchase of non-prescription over-the-counter medications with FSA money (it used to say "reimbursement for expenses incurred for a medicine or a drug shall be treated as a reimbursement for medical expenses only if such medicine or drug is a prescribed drug (determined without regard to whether such drug is available without a prescription) or is insulin." That provision was eliminated under the CARES Act).

Section 4402 of the CARES Act also changed the rules to allow menstrual products to be purchased with FSA funds. The new rules that allow FSA funds to be used for over-the-counter medications and menstrual products are retroactive to January 1, 2020, and are permanent changes. So they have remained in place even though the COVID-19 emergency period ended in 2023.

In 2024, the IRS issued new guidance clarifying that male condoms are a qualified medical expense and can be purchased with pre-tax FSA, HSA, or HRA funds.6

Footnotes

- "IRS releases tax inflation adjustments for tax year 2026, including amendments from the One, Big, Beautiful Bill" Internal Revenue Service. Oct. 9, 2025 ⤶ ⤶

- "IRS: Healthcare FSA reminder: Employees can contribute up to $3,300 in 2025; must elect every year" Internal Revenue Service. Nov. 7, 2024 ⤶ ⤶ ⤶

- "Can my spouse and I both have an FSA?" FSA Store. Accessed Dec. 7, 2025 ⤶

- "Do Employer Contributions Count Toward the Contribution Limit That Applies to Health FSAs?" Thompson Reuters. Nov. 13, 2024 ⤶

- "Shedding light on the letter of medical necessity" FSA Store. Accessed Dec. 7, 2025 ⤶

- "Notice 2024-71. Expenses Treated as Amounts Paid for Medical Care" Internal Revenue Service. Accessed Nov. 20, 2024 ⤶