Medicare in Michigan

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Michigan

Medicare enrollment in Michigan

As of January 2026, there were 2,306,545 people enrolled in Medicare in Michigan.1 For most people, signing up for Medicare benefits is part of turning age 65. But after receiving Social Security disability benefits for two years, a person will become eligible for Medicare, and Medicare eligibility is also triggered if a person is diagnosed with end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS).

Nationwide, almost 90% of Medicare beneficiaries are eligible due to their age, and the remaining 10% are eligible due to a disability.2 In Michigan, about 11% of Medicare beneficiaries are eligible due to disability rather than age.3

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Michigan’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

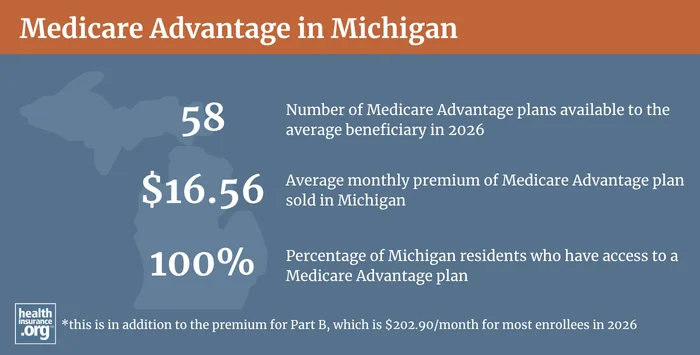

Medicare Advantage plan availability and enrollment in Michigan

Medicare Advantage plans are provided by private insurers, and plan availability varies considerably across the country. Michigan’s Medicare Advantage market is robust, with an average of 50 plans available to residents in 2026. (Plan availability varies by area.)4

As of early 2026, over 63% of Michigan Medicare beneficiaries were enrolled in Medicare Advantage plans,3 versus just over 51% nationwide.2

Learn more about Medicare Advantage and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Michigan by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in Michigan

According to an AHIP analysis, 382,269 Michigan Medicare beneficiaries had Medigap coverage as of 2023.5

Learn more about how Medigap plans are standardized and what they cover.

Twenty-four insurers were actively selling Medigap plans in Michigan as of 2026.6

People who aren’t yet 65 can enroll in Medicare if they’re disabled and have been receiving disability benefits for at least two years, and about 11% of Michigan Medicare enrollees are under age 65.7 Federal rules do not guarantee access to Medigap plans for people who are under 65, but the majority of the states, including Michigan, have implemented rules to ensure that disabled Medicare beneficiaries have at least some access to Medigap plans.

For at least twenty years, Michigan has had rules in place to ensure access to at least some Medigap plans for people under age 65. Current rules in Michigan (see MCL 500.3831, updated as of March 2019, to MCL 500.3831.amended) require Medigap insurers that also sell major medical health insurance to make Medigap Plans A and G (prior to 2020 this was Plan C) continuously guaranteed-issue for Medicare beneficiaries under age 65, although they can charge these enrollees higher premiums. And if the applicant did not already have major medical coverage under a plan offered by that insurer, the insurer can impose a pre-existing condition waiting period of up to six months (see MCL 500.3831(2)).

As of 2026, four insurers in Michigan offered Medigap policies (at least A and G) to people under age 65.6 The other 20 Medigap insurers in the state did not offer coverage to Medicare beneficiaries under age 65.

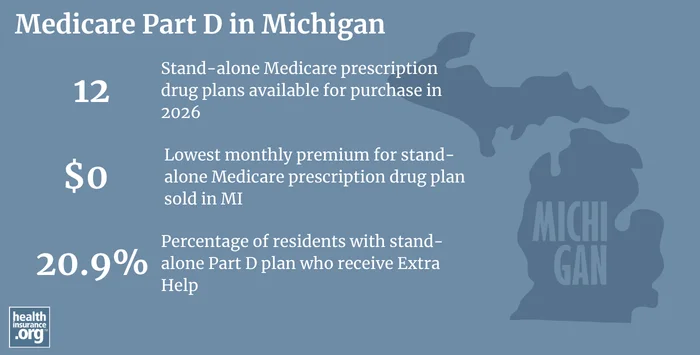

Medicare Part D plan availability and enrollment in Michigan

There are 12 stand-alone Medicare Part D prescription drug plans for sale in Michigan for 2026, with premiums starting as low as $0.8 As of January 2026, 1,975,688Medicare beneficiaries in Michigan had Medicare Part D prescription drug coverage. There were 1,040,053 beneficiaries with Part D coverage under Medicare Advantage plans, and 935,635 had stand-alone Medicare Part D prescription drug coverage.3

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Michigan

- To learn more about Medicare in Michigan, you can contact MMAP, the Michigan Medicare/Medicaid Assistance Program, with questions related to Medicare coverage in Michigan.

- The Michigan Department of Insurance and Financial Services is a state resource that can provide information, assistance, and customer service for a variety of issues related to health insurance. The Department oversees and licenses the insurers that offer health plans in the state, as well as the brokers/agents who sell the policies.

- The Medicare Rights Center is a nationwide service, with a website and call center, that can provide information and answer questions related to Medicare eligibility, enrollment, and benefits.

- Learn about programs offered via Michigan Medicaid that can help Medicare beneficiaries who have limited income and assets.

Looking for more information about other options in your state?

Need help navigating health insurance options in Michigan?

Explore more resources for options in MI including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Michigan” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶

- “Medicare Monthly Enrollment – U.S” Centers for Medicare & Medicaid Services Data, Accessed April 2026 ⤶ ⤶

- “Medicare Monthly Enrollment – Michigan” Centers for Medicare & Medicaid Services Data. Accessed April 2026 ⤶ ⤶ ⤶

- “Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings” KFF.org. December 9, 2025 ⤶

- “The State of Medicare Supplement Coverage” Page 12. AHIP.org, May 2025 ⤶

- “Authorized Medicare Supplement Companies” Michigan Department of Insurance and Financial Services. Updated Jan. 15, 2026 ⤶ ⤶

- “Medicare Monthly Enrollment – Michigan, January 2026” Centers for Medicare & Medicaid Services Data. Accessed Apr. 29, 2026 ⤶

- “Fact Sheet: Medicare Open Enrollment 2026” Centers for Medicare & Medicaid Services. September 26, 2025. ⤶