Find New York Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

New York Health Insurance Marketplace Guide

We’ve created this guide, including the FAQs below, to help you understand the health coverage options and financial assistance available to you and your family in New York. The options found in New York’s Marketplace may be a good choice for many consumers who don’t have access to employer-sponsored health insurance, Medicare, or Medicaid.

New York residents use a fully state-based health insurance Marketplace known as NY State of Health, where a dozen private insurers offer health plans.1 All of them will continue to offer coverage in the Marketplace for 2027 (see below for details about premium changes for 2027).

The Marketplace also provides residents access to apply for coverage under the Essential Plan (BHP),2 which offers premium-free coverage to residents whose income is too high to qualify for Medicaid or Child Health Plus, but not more than 200% of the federal poverty level.

This income limit was increased to 250% of FPL from April 2024 through June 2026, but reverted to 200% FPL in July 2026 due to reductions in federal funding stemming from the One Big Beautiful Bill that was enacted in 2025.3 Nearly half a million people were disenrolled from the Essential Plan in July 2026 due to the reduction in the income limit for eligibility.4

In the same 1332 waiver that New York used to increase the Essential Plan’s income limit to 250% of FPL (no longer applicable after June 2026), the state also received federal approval to use 1332 waiver pass-through funding to provide additional cost-sharing reductions for some Marketplace enrollees starting in 20255 (more details below). This benefit continues to be available through the end of 2026,67

New York State of Health also offers a small business portal where employers with up to 100 employees can compare group health plans. In most states, “small group” means up to 50 employees, but New York is one of three states where small group plans are available to groups of up to 100 employees.8

New York ACA Marketplace quick facts

Frequently asked questions about health insurance in New York

Who can buy Marketplace health insurance in New York?

To purchase health coverage through the New York Health Insurance Marketplace, you must:11

- Live in New York

- Be lawfully present in the United States

- Not be incarcerated

- Not be enrolled in Medicare12

Eligibility for financial assistance (premium subsidies and cost-sharing reductions) depends on your household income. In addition, to qualify for financial assistance with your New York Marketplace plan you must:

- Not have access to affordable employer-sponsored health coverage. If your employer offers coverage but you feel it’s too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies in the Marketplace.

- Not be eligible for Medicaid, Child Health Plus, or The Essential Plan.

- Not be eligible for premium-free Medicare Part A.13

- If married, file a joint tax return.14

- Not be able to be claimed by someone else as a tax dependent.15

When can I enroll in an ACA-compliant plan in New York?

In New York, the open enrollment period for 2026 coverage ended on January 31, 2026.16

A federal rule change had called for a shorter open enrollment period starting in the fall of 2026, but that was vacated by a judge in June 2026.17 So it’s expected that New York will continue to end open enrollment on January 31 for coverage effective in 2027.

Enrollment in New York Medicaid, Child Health Plus, and the Essential Plan continues year-round for eligible people.

For qualified health plans (ie, not Medicaid, CHP, or the Essential Plan), enrollment outside of the annual open enrollment window is only possible if you’re eligible for a special enrollment period, which is typically triggered by a specific qualifying life event. (American Indians and Alaska Natives can enroll year-round without a qualifying life event.)

New York is one of several states where pregnancy counts as a qualifying event. In most states, it’s the birth that triggers a special enrollment period, but New York allows the expectant mother to sign up for health insurance due to the pregnancy.18

If you have questions about open enrollment, you can learn more in our comprehensive guide to open enrollment. We also have a comprehensive guide to special enrollment periods.

How do I enroll in a New York Marketplace plan?

To enroll in an ACA Marketplace plan in New York, you can:

- Visit NY State of Health to access New York’s Marketplace, an online platform where you can compare plans, determine whether you’re eligible for financial assistance, and enroll in the plan that best meets your needs.

- Purchase NY State of Health Marketplace health coverage with the help of an insurance agent or broker, a Navigator, or a certified application counselor.19

You can contact NY State of Health by phone at 1-855-355-5777 (TTY: 1-800-662-1220)

How can I find affordable health insurance in New York?

New York residents use NY State of Health to enroll in health coverage and obtain income-based subsidies.

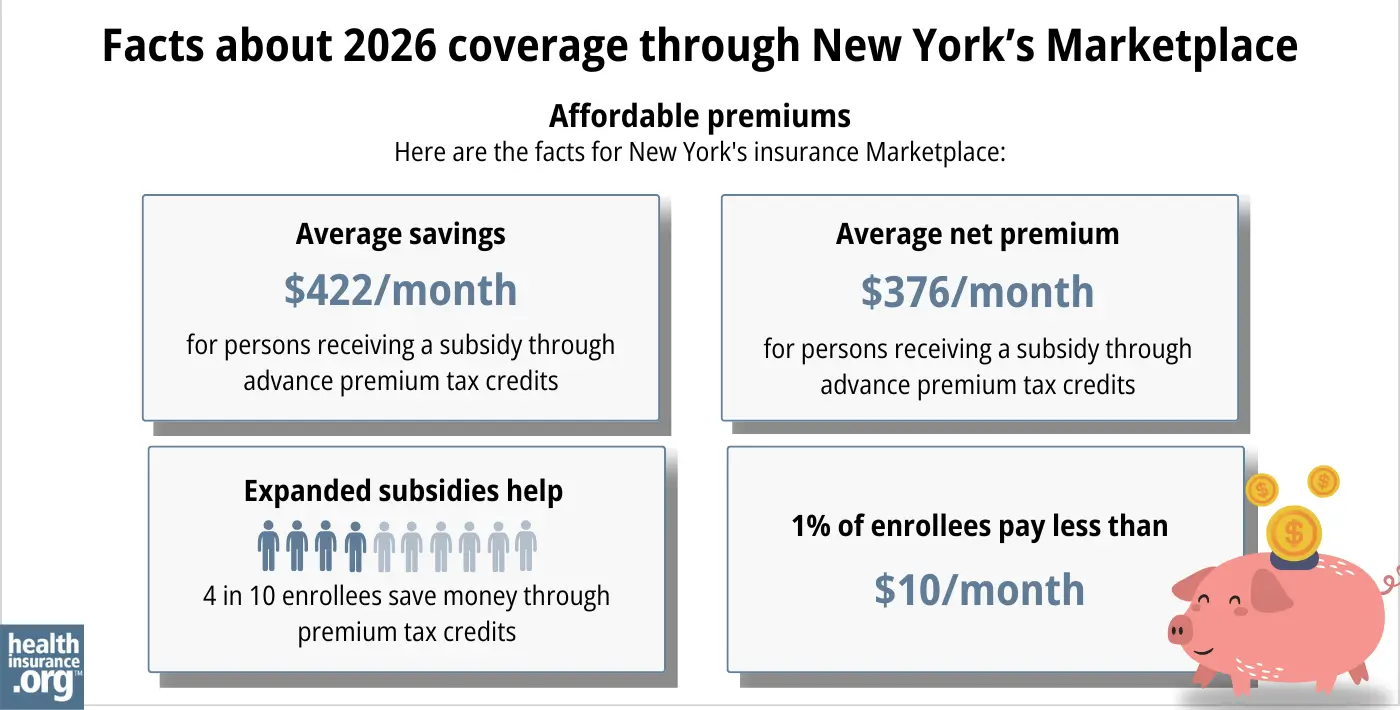

In the New York exchange, during the open enrollment period for 2026 coverage, 43% of the people who enrolled in private health plans qualified for federal premium subsidies. The average subsidy amount was $422/month. After the subsidies were applied, subsidy-eligible enrollees’ net premiums averaged $376/month.20

However, federal subsidy enhancements expired at the end of 2025, after Congress failed to extend them. This means fewer people are subsidy-eligible in 2026, and the subsidies don’t cover as much of enrollees’ premiums as they did in 2025. The overall average net premium (including people who pay full price) was $532/month in 2025,21 and grew to $636/month in 2026.20

Source: CMS.gov20

In addition to the private qualified health plans available through the state exchange, nearly 1.7 million people were enrolled in New York’s zero-premium Essential Plan coverage as of May 2026.22 Essential Plan enrollment is completed via NY State of Health, just like qualified health plan enrollment. But as many as 500,000 people lost Essential Plan coverage on July 1, 2026, when the income limit reverted to 200% FPL, after being set at 250% FPL for more than two years.4

The Essential Plan has zero premiums and low cost-sharing. It’s available to adults with household incomes up to 200% of the poverty level. As of July 2026, this amounts to $31,920 for a single adult.23

(NY obtained federal permission to extend the eligibility limit to 250% of FPL, starting in April 2024.24 But starting in July 2026, New York reduced the Essential Plan eligibility limit back to 200% of FPL, due to federal funding cuts that were part of the “One Big Beautiful Bill.”3 So starting in July 2026, people with income between 200% and 250% of FPL transitioned to qualified health plan coverage in the Marketplace instead.)

Marketplace enrollees with household incomes up to 250% of the federal poverty level also qualify for the ACA’s cost-sharing reductions (CSR) that reduce the out-of-pocket costs on Silver plans. As of July 2026, this again includes enrollees with income between 200% and 250% of FPL, as they are no longer eligible for the Essential Plan.

New York also offers state-funded cost-sharing reductions that extend to 400% of FPL, as well as cost-sharing reductions for diabetes treatment and pregnancy and postpartum services.25 But this is only expected to continue through the end of 2026.7

A note about standardization of qualified health plans in New York: Insurers that offer plans through NY State of Health must offer one standard plan design in each metal level in every county where the insurer offers plans (here are the 2026 standardized plan details).

Carriers can also offer up to two non-standard plan designs at each metal level, and nine of New York’s 12 Marketplace insurers choose to offer non-standardized plans in addition to their standardized plans. The non-standardized plans include additional benefits such as adult dental and vision, or acupuncture. Unlike standardized plans, cost-sharing varies from one insurer to another for non-standardized plans.26

Starting in 2021, New York required state-regulated (non-self-insured) health plans, including Marketplace plans, to cap out-of-pocket costs for insulin at no more than $100 per month. But starting in 2025 (on a plan’s first renewal on or after January 1, 2025), state-regulated plans in New York can no longer charge any cost-sharing for insulin, meaning enrollees no longer have out-of-pocket costs for insulin.27

New York’s ban on out-of-pocket costs for insulin applies to HSA-eligible high-deductible health plans, just like any other plan. This is possible because in 2019, the IRS expanded the scope of preventive care that HDHPs can pay before the deductible is met, including insulin.28

How many insurers offer Marketplace coverage in New York?

Twelve insurers offer qualified health plans through New York’s Marketplace for 2026,1 all of which plan to continue to offer coverage in 2027:29

- Capital District Physicians’ Health Plan (CDPHP)

- Health Insurance Plan of Greater New York (Emblem)

- Anthem HP (formerly Empire HealthPlus)

- Excellus Health Plan

- Fidelis (New York Quality Health Care Corp)

- Healthfirst PHSP

- Highmark Western and Northeastern New York (formerly HealthNow)

- Independent Health Benefits Corporation (IHBC)

- Metro Plus Health Plan

- MVP Health Plan

- Oscar

- UnitedHealthcare of New York

Each insurer sets its own coverage area. The number of participating insurers in each county varies from two to seven, but the average enrollee can choose from among at least four insurers’ plans for 2026.16

See the next FAQ for details about proposed premium changes for 2027 for each insurer.

Are Marketplace health insurance premiums increasing in New York?

For 2027, the insurers that offer Marketplace health plans in New York have proposed the following average rate increases, amounting to an overall average rate increase of 20.7%, before subsidies are applied.29

New York’s ACA Marketplace Plan 2027 PROPOSED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Capital District Physicians’ Health Plan (CDPHP) | 1.4% |

| Health Insurance Plan of Greater New York (Emblem) | 26.8% |

| Anthem HP (formerly Empire HealthPlus) | 11.3% |

| Excellus Health Plan | 17.2% |

| Fidelis (New York Quality Health Care Corp) | 28.4% |

| Healthfirst PHSP | 14.9% |

| Highmark Western and Northeastern New York (formerly HealthNow) | 23.8% |

| Independent Health Benefits Corporation (IHBC) | 14.2% |

| Metro Plus Health Plan | 17% |

| MVP Health Plan | 10.7% |

| Oscar | 23.8% |

| UnitedHealthcare of New York | 52.1% |

Source: New York State Department of Financial Services29

It’s important to understand that net rate changes for people who receive premium subsidies can be quite different from the overall rate changes for that person’s plan, since it also depends on how the benchmark plan (second-lowest-cost silver plan) premium changes.

Because Congress did not extend the federal subsidy enhancements that had been in effect since 2021, subsidies don’t cover as much of enrollees’ total premiums in 2026, and are available to fewer people, and this will continue to be the case in 2027 and future years. New York Governor Kathy Hochul signed a joint letter from 18 states, urging Congress to take immediate action to extend the subsidy enhancements in the fall of 2025, to prevent health coverage from becoming much less affordable in 2026.30 But Congress did not extend the subsidy enhancements, so coverage did become significantly less affordable in 2026.

For perspective, here’s a summary of how average full-price (pre-subsidy) premiums for qualified health plans in New York’s individual/family market have changed over the years:

- 2015: Average increase of 5.7%.31

- 2016: Average increase of 7.1%.32

- 2017: Average increase of 16.6%.33

- 2018: Average increase of 13.9%.34

- 2019: Average increase of 8.6%.35

- 2020: Average increase of 6.8%.36

- 2021: Average increase of 1.8%.37

- 2022: Average increase of 3.7%.38

- 2023: Average increase of 9.7%.39

- 2024: Average increase of 13.5%.40

- 2025: Average increase of 12.7%.41

- 2026: Average increase of 7.1%.1

How many people are insured through New York’s Marketplace?

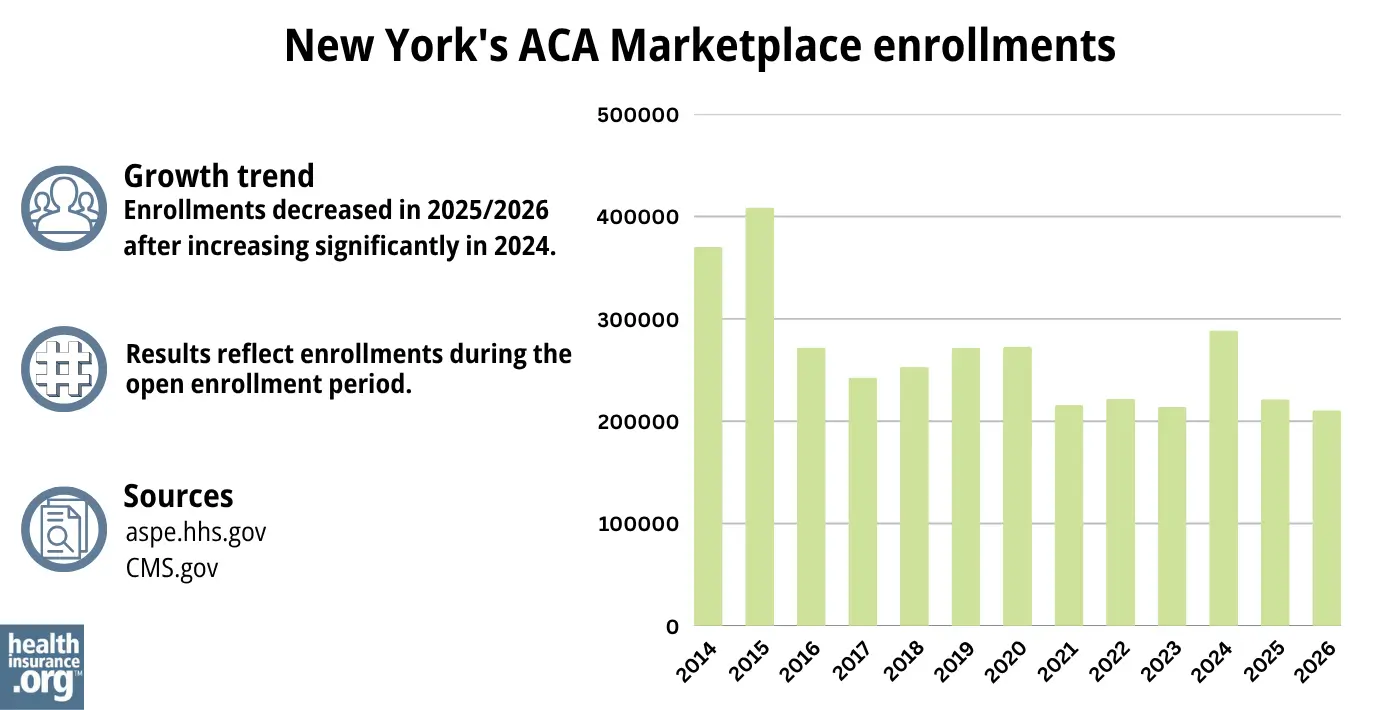

CMS reported that 210,704 people enrolled in private qualified health plans through NY State of Health during the open enrollment period for 2026 coverage.20 It was not surprising that enrollment was lower than it had been in 2025, after federal subsidy enhancements expired at the end of 2025, resulting in significantly higher after-subsidy premiums in 2026.

Although nationwide Marketplace enrollment has reached record highs in recent years, that hasn’t been the case in New York (see graph below). This is because of the expansion of Essential Plan eligibility starting in April 2024, when people with household income between 200% and 250% of FPL became eligible for the Essential Plan and were able to transition from QHPs to the Essential Plan (as noted above, eligibility for the Essential Plan is once again capped at 200% of FPL starting in July 2026).3

The chart below shows QHP enrollment by year in New York. But it’s important to note that the Essential Plan covers far more people than the QHPs in the state. As of May 2026, there were 202,757 QHP enrollees through NY State of Health, while Essential Plan enrollment stood at 1,663,063.42

Source: 2014,43 2015,44 2016,45 2017,46 2018,47 2019,48 2020,49 2021,50 2022,51 2023,52 2024,53 202554 202620

Enrollment in QHPs dropped in 2016 when the Essential Plan debuted, because many people previously eligible for subsidized QHPs transitioned to the Essential Plan starting in 2016. The same thing happened in 2024 and 2025, with the expansion of the Essential Plan.

But earlier in 2024, QHP enrollment was higher than it had been in several years. The enrollment growth in 2024 was likely driven by a combination of the continued subsidy enhancements under the American Rescue Plan, as well as the Medicaid unwinding process that began in the spring of 2023. By June 2024, more than 2 million people in New York had been disenrolled from Medicaid.55

Some of them had transitioned to QHPs in the Marketplace, helping to drive 2024 enrollment. CMS reported that by April 2024, nearly 84,000 New York residents had transitioned from Medicaid to a qualified health plan in the Marketplace, and more than 416,000 had transitioned to Essential Plan coverage.56

What health insurance resources are available to New York residents?

NY State of Health 855-355-5777

State Exchange Profile: New York

The Henry J. Kaiser Family Foundation overview of New York’s progress toward creating a state health insurance exchange.

Health Care For All New York (HCFANY)

Looking for more information about other options in your state?

Need help navigating health insurance options in New york?

Explore more resources for options in NY including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”Summary of Requested & Approved 2026 Rate Actions” New York Department of Financial Services. Aug. 29, 2025 ⤶ ⤶ ⤶

- “Essential Plan Fact Sheet” nystateofhealth.ny.gov, March 2022 ⤶

- ”Following Devastating Federal Funding Cuts, New York State Takes New Action to Preserve Health Care for As Many New Yorkers As Possible” New York Department of Health. Sep. 10, 2025 ⤶ ⤶ ⤶

- ”Losing Essential Plan Health Coverage? Here’s Your Guide for Finding Low-Cost Care in New York” Community Service Society. July 16, 2026 ⤶ ⤶

- ”Section 1332: State Innovation Waivers, New York” and “Letter from CMS to New York, approving 1332 waiver amendment” CMS.gov. Sep. 25, 2024 ⤶

- ”Attachment U: 2026 Cost Sharing Reduction Initiatives” New York State of Health. Accessed Sep. 18, 2025 ⤶

- ”Free Insulin Program in New York Remains Amidst State Transition Back to the Basic Health Plan, Cost-sharing programs extended until the end of 2026” Health Care for All New York Blog. May 26, 2026 ⤶ ⤶

- Market Rating Reforms — State Specific Rating Variations. Centers for Medicare and Medicaid Services. Colorado no longer uses the expanded definition of “small group,” as of 2026. Accessed Feb. 9, 2026 ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Summary of Requested & Approved 2026 Rate Actions” New York Department of Financial Services. Aug. 29, 2025 *The above is based on the most current data available. ⤶

- ”Qualified Health Plans Information” New York State of Health. Accessed July 2, 2026 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Feb. 9, 2026 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Feb. 9, 2026 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Feb 9, 2026 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Feb. 9, 2026 ⤶

- ”2026 Qualified Health Plan and Essential Plan Line Up” New York State of Health. Oct. 29, 2025 ⤶ ⤶

- ”City of Columbus et al. v. Kennedy et al. (Columbus I)” O’Neill Institute Health Care Litigation Tracker. Vacatur announced June 12, 2026 ⤶

- Special Enrollment Periods. NY State of Health. Accessed December 2023. ⤶

- Assistors. New York State of Health. Accessed Feb. 9, 2026 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶ ⤶

- ”2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶

- ”EP and QHP Enrollment as of May 3, 2026” New York State of Health. Jan. 4, 2026 ⤶

- ”Essential Plan Information” NY State of Health. Accessed July 2, 2026 ⤶

- ”Governor Hochul Announces Federal Approval to Expand Access to High-Quality, Affordable Health Insurance” New York State Governor Kathy Hochul. March 4, 2024. ⤶

- ”State Health Department’s NY State of Health Announces Approval of State’s Innovation Waiver Amendment In Time for 2025 Enrollment Period” New York State Department of Health. Oct. 2, 2024 ⤶

- ”2026 Qualified Health Plan and Essential Plan Line Up” NY State of Health. Oct. 29, 2025 ⤶

- Insulin Cost-Sharing Limit Q&A Guidance. New York State Department of Financial Services. Accessed Feb. 9, 2026. ⤶

- ”Notice 2019-45: Additional Preventive Care Benefits Permitted to be Provided by a High Deductible Health Plan Under § 223” Internal Revenue Service. Accessed Feb. 9, 2026 ⤶

- ”Summary of Requested 2027 Rate Actions” And “Requested Rate Actions – Additional Information” New York State Department of Financial Services. Accessed June 12, 2026 ⤶ ⤶ ⤶

- ”Press Release: Governor Hochul Urges Congress to Pass an Extension of Affordable Care Act Health Insurance Subsidies” New York State of Health. Sep. 17, 2025 ⤶

- New York health insurance rates to rise in 2015. Long Island Business News. September 2023. ⤶

- FINAL PROJECTION: 2016 Weighted Avg. Rate Increases: 12-13% Nationally* ACA Signups. October 2015. ⤶

- Department of Financial Services Announces 2017 Health Insurance Rates. New York State Department of Financial Services. August 2016. ⤶

- DFS Announces 2018 Health Insurance Rates in a Continued Robust New York Market. New York State Department of Financial Services. August 2017. ⤶

- 2019 Rate Hikes. ACA Signups. October 2018. ⤶

- 2020 Rate Changes. ACA Signups. October 2019. ⤶

- DFS Announces 2021 Health Insurance Premium Rates, Protecting Consumers During COVID-19 Pandemic. New York Department of Financial Services. August 2020. ⤶

- DFS Announces 2022 Health Insurance Premium Rates, Saving New Yorkers $607 Million. August 2021. ⤶

- “DFS Announces 2023 Health Insurance Premium Rates” NY Dept. of Financial Services, April 17, 2022 ⤶

- 2024 Individual and Small Group Requested and Approved Rate Actions. New York State Department of Financial Services. October 2023. ⤶

- ”Summary of Requested & Approved 2025 Rate Actions” New York State Department of Financial Services. Aug. 30, 2024. ⤶

- ”EP and QHP Enrollment as May 3, 2026” New York State of Health. Accessed June 12, 2026 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “2023 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2023, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶

- Medicaid Enrollment and Unwinding Tracker. KFF. Data through June 2024. ⤶

- State-based Marketplace (SBM) Medicaid Unwinding Report, data through April 2024. Centers for Medicare & Medicaid Services. Accessed Aug. 15, 2024. ⤶