Find Florida Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Florida Health Insurance Marketplace Guide

This guide, including the FAQs below, will help you understand the Florida health insurance options available to you and your family. Many people find that an Affordable Care Act (ACA) Marketplace plan – or Obamacare – helps them save money on health insurance expenses.

Florida uses the federally-facilitated Health Insurance Marketplace: HealthCare.gov. Individual and family plans on the ACA exchange in Florida are available for:1

- Self-employed people

- People who retired early and need coverage until they become eligible for Medicare

- People who work for small businesses without health benefits

Florida’s Marketplace has by far the highest enrollment in the U.S. Almost one out of every five Marketplace enrollees is in Florida.2

Sixteen private insurance companies are offering coverage through the Florida Health Insurance Marketplace for 2026,3 with plan availability varying from one area to another.4 But as explained below, there were some changes in the list of participating insurers for 2026. And for 2027, Cigna will no longer offer Marketplace plans in Florida (or in any state). Premium changes for 2026 are also detailed below.

Florida banned surprise balance billing starting in mid-2016, for state-regulated health plans.5 Florida’s law was lauded as a model for other states that wanted to implement similar consumer protections. The federal No Surprises Act took effect in 2022, providing nationwide protection from surprise balance bills, including for people with self-insured plans (which aren’t regulated by state laws).

*Values displayed by this tool are from data generated by CMS and reflect 2026 Marketplace health plans purchased in each state. The values returned are averages based on the plans purchased by consumers of each selected state: subsidy and premium values vary based on factors such as zip code, age, household size, and income.

Florida Marketplace quick facts

Frequently asked questions about health insurance in Florida

Who can buy Marketplace health insurance in Florida?

To qualify for Florida Health Insurance Marketplace coverage, you must:1

- Live in Florida

- Be a U.S. citizen, national, or lawfully present in the U.S.

- Not be incarcerated

- Not be enrolled in Medicare

But those rules just allow a person to enroll in coverage through the exchange. Eligibility for financial assistance (premium subsidies and/or cost-sharing reductions) through the Health Insurance Marketplace depends on how your household income compares with the cost of the second-lowest-cost Silver plan in your area.

In addition, to qualify for financial assistance with your Marketplace plan you must:

- Not be eligible for Medicaid or CHIP (Florida KidCare), or premium-free Medicare Part A.8

- Not have access to affordable employer-sponsored health coverage. If your employer (or your spouse’s employer) offers coverage but you feel it’s too expensive, you can use our Employer Health Plan Affordability Calculator to learn whether you might be eligible for premium subsidies in the Florida Marketplace.

- If married, file a tax return jointly with your spouse.9

- Not be able to be claimed by someone else as a tax dependent.9

When can I enroll in an ACA-compliant plan in Florida?

The open enrollment period to sign up for 2026 ACA-compliant individual and family health insurance in Florida ended on January 15, 2026.10

Open enrollment will be shorter, however, starting in the fall of 2026. Due to a rule change that was finalized in 2025, the open enrollment period will still start on November 1, 2026, but it will end on December 15. All plans selected during open enrollment will take effect January 1, 2027.

Outside of open enrollment, you can only enroll or switch plans if you meet the special enrollment period (SEP) requirements. Most SEPs require a qualifying life event, such as losing coverage, getting married, or permanently moving, but American Indians and Alaska Natives can enroll year-round.11

How do I enroll in a Florida health insurance Marketplace plan?

To sign up for a Florida Health Insurance Marketplace plan, you have several enrollment options:

- Online through HealthCare.gov.

- By calling the Marketplace Call Center at (800) 318-2596.

- With the help of licensed agents, navigators, or certified application counselors or an approved enhanced direct enrollment entity.12

- Mailing in a paper application

Go to localhelp.HealthCare.gov to find a navigator, certified application counselor, or agent in your area.

How can I find affordable health insurance in Florida?

You can find affordable individual and family health insurance in Florida through HealthCare.gov, which is Florida’s ACA exchange/Marketplace.

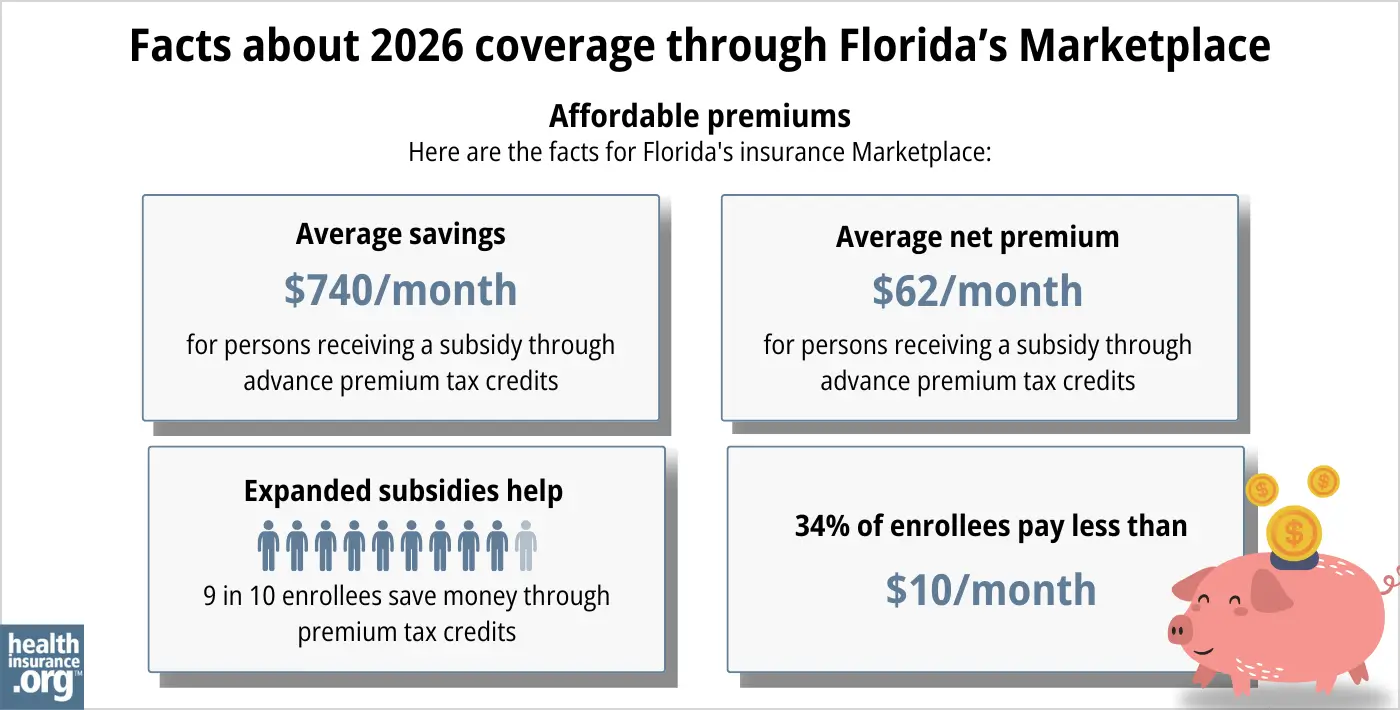

During open enrollment for 2026 coverage, more than 95% of Florida’s Health Insurance Marketplace enrollees qualified for premium subsidies.13 These subsidies, called Advance Premium Tax Credits (APTC), lower your monthly premiums.

The subsidies averaged $740/month, and the average subsidy-eligible enrollee was paying about $62/month for their coverage after the subsidies were applied.13

Most Marketplace enrollees do still qualify for subsidies, but the subsidies don’t cover as much of enrollees’ total premiums in 2026, and are no longer available to enrollees with household income above 400% of the federal poverty level. This is because Congress did not extend the federal subsidy enhancements that had been in place from 2021 through 2025, so they expired at the end of 2025.

If your household income is between 100% and 250% of the federal poverty level and you select a Silver plan through the Florida Health Insurance Marketplace, you will also receive cost-sharing reductions (CSR). While APTCs help reduce health insurance costs, CSRs reduce out-of-pocket costs like deductibles, copayments, or coinsurance.

As of early 2026, nearly half of Florida’s Marketplace enrollees were receiving CSR benefits.13 But this was down from about two-thirds of enrollees the year before,14 because many enrollees switched from Silver plans to Bronze plans (thus forfeiting their CSR), in order to keep their premiums affordable.

Source: CMS.gov 13

Medicaid and Florida KidCare (CHIP) are options for affordable health insurance in Florida if you qualify for either program.

Alternatively, short-term plans offer low-cost health coverage, for people who aren’t eligible for Medicaid or a Marketplace subsidy. These plans can also be used for temporary coverage by people who missed the annual enrollment period for ACA-compliant coverage. But short-term health insurance is much less robust than ACA-compliant coverage, generally does not cover pre-existing conditions or all of the essential health benefits, and should not be considered an adequate substitute for ACA-compliant major medical coverage.

How many insurers offer Marketplace health insurance in Florida?

Sixteen insurers are offering coverage through the Florida Health Insurance Marketplace for 2026, including two separate Cigna entities,3 (coverage areas vary by carrier).15

Notable changes for 2026 include:

- Aetna exited at the end of 2025 (as is the case in all states where they offered individual market coverage).

- Community Care Network Inc. (22 Health) is new for 20263 (plans only available in Broward County).15

- Cigna added new HMO plans in 2026 that are sold under a separate entity (Cigna Healthcare of Florida, Inc.)

But Cigna will not offer plans after the end of 2026. So Florida Marketplace enrollees with Cigna plans (including Cigna HMO and Cigna Health & Life) will need to select new plans during the open enrollment period that begins November 1, 2026. In 2026, Cigna’s plans are available in 11 of Florida’s 67 counties.16

How much is health insurance in Florida and will premiums rise?

The following average rate changes were approved for 2026 for individual/family plans sold through Florida’s Health Insurance Marketplace, amounting to an overall weighted average rate increase of 31.5%, before any subsidies are applied.3 (As described below, after-subsidy premium increases were much more significant, due to the expiration of the federal subsidy enhancements that had been in effect since 2021.)

Florida’s ACA Marketplace Plan 2026 APPROVED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Aetna CVS Health / Coventry Health Plan of Florida | Exiting market |

| Community Care Network, Inc. (22 Health) | New for 2026 |

| AmeriHealth Caritas | 37.2% |

| AvMed | 24.5% |

| Blue Cross Blue Shield of Florida, Inc. | 29.6% |

| Capital Health Plan | 29.7% |

| Centene Venture Company Florida (Celtic/Ambetter) |

37.9% |

| Cigna Health & Life Ins. Co. | 29.5% |

| Cigna (HMO) | New for 2026 |

| Florida Health Care Plan, Inc. | 26.2% |

| Health First Commercial Plans | 23.2% |

| Health Options (Florida Blue HMO) | 29% |

| Molina Healthcare of Florida, Inc. | 40.8% |

| Oscar Insurance Company of Florida | 26.4% |

| Sunshine State Health Plan | 48.7% |

| UnitedHealthcare | 29.9% |

| Simply Healthcare Plans, Inc. (Wellpoint) | 27.2% |

Source: FLOIR (Florida Office of Insurance Regulation)3

Average rate changes are calculated before subsidies are applied. Most Florida exchange enrollees receive subsidies that covered the majority of the premium cost in 2025.17 But because Congress did not extend the federal subsidy enhancements that had been in place since 2021, the enhancements expired at the end of 2025. As a result, subsidies are smaller in 2026 than they would have been if the enhancements had been extended, and some people lost their subsidies altogether. This made coverage significantly less affordable, and fewer people enrolled in Marketplace plans for 2026.

Here are some examples of the sort of net premium increases that people experienced in Fort Lauderdale for 2026:18

- 40-year-old earning $40,000:

- Lowest-cost plan in 2025 was $34/month

- Lowest-cost plan in 2026 is $110/month

- 60-year-old earning $63,000:

- Lowest-cost plan in 2025 was $191/month

- Lowest-cost plan in 2026 is $1,064/month (due to the subsidy cliff)

For perspective, here’s a summary of how full price premiums in Florida’s ACA-compliant market have changed over the years:

- 2015: Average increase of 7%19

- 2016: Average increase of 9.5%20

- 2017: Average increase of 19.1%21

- 2018: Average increase of 44.7%22 (federal funding for cost-sharing reductions was eliminated)

- 2019: Average increase of 5.2%23

- 2020: Average increase of 0%24

- 2021: Average increase of 3.1%25

- 2022: Average increase of 6.6%26

- 2023: Average increase of 7.2%27

- 2024: Average increase of 5.3%28

- 2025: Average increase of 7.5%29

How many people are insured through Florida’s Marketplace?

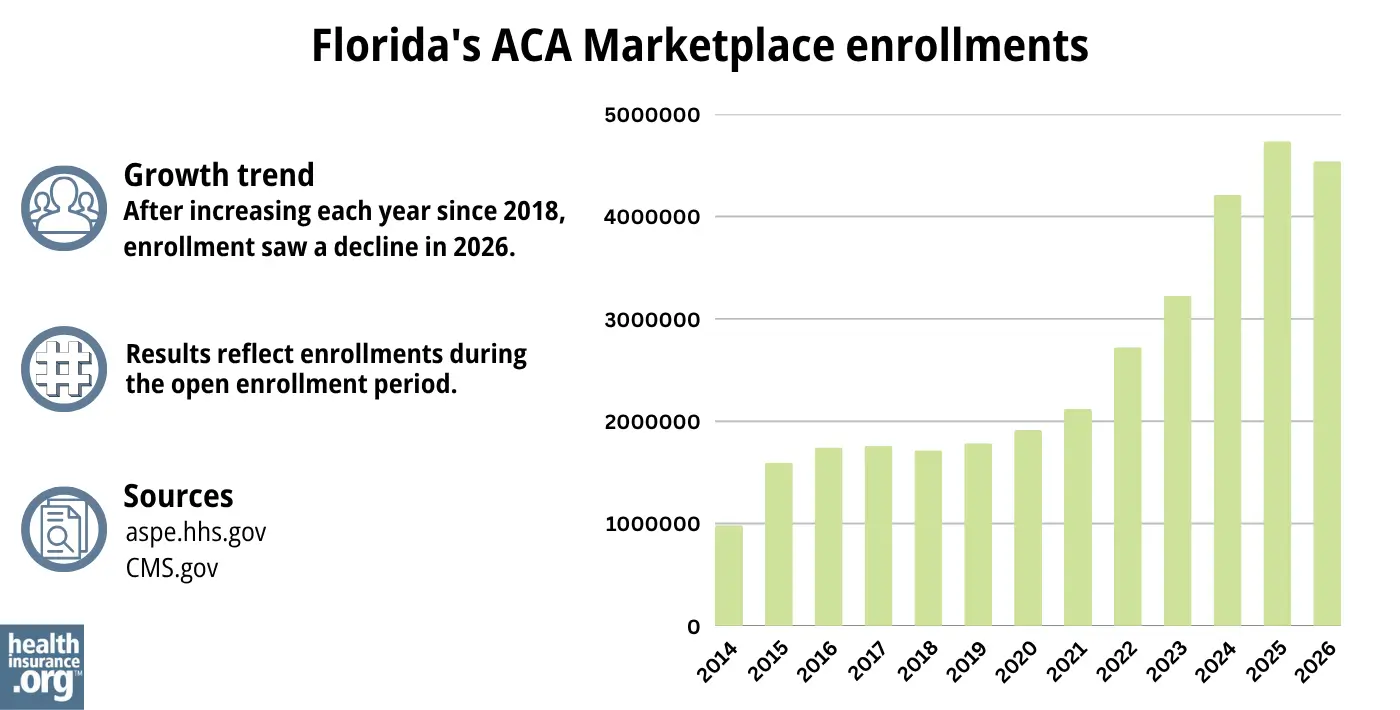

4,538,772 selected Florida Marketplace plans during the open enrollment period for 2026 coverage.13

Although Florida continues to have the nation’s highest Marketplace enrollment, 2026 enrollment was down about 4% from the year before, when a significant record high of 4,735,415 people enrolled in health insurance through Florida’s Marketplace during the open enrollment period for 2025 coverage.30

Source: 2014,31 2015,32 2016,33 2017,34 2018,35 2019,36 2020,37 2021,38 2022,39 2023,40 2024,41 202530 202613

Before the drop in enrollment for 2026, Florida Marketplace enrollment had been increasing for several years in a row (see chart above). The enrollment growth in recent years was due in part to the American Rescue Plan, which improved affordability starting in 2021. The Inflation Reduction Act then extended these improvements until 2025, ensuring coverage remains more affordable than it was before the ARP became law.42

But because the subsidy enhancements were allowed to expire at the end of 2025, coverage became less affordable for 2026 and enrollment declined for the first time since 2018.

The enrollment spike in 2024 and 2025 was also due to the “unwinding” of the pandemic-era Medicaid continuous coverage rule. Medicaid disenrollments resumed in 2023 after a three-year pause, and some people who previously had Medicaid transitioned to Marketplace coverage instead.

What health insurance resources are available to Florida residents?

Healthcare.gov

This is the ACA Marketplace, where you can enroll in a health insurance plan online. You may also get help by calling (800) 318-2596.

Florida Consumer Action Network (FCAN)

Nonprofit consumer advocacy group that helps Floridians understand their health insurance options.

Florida KidCare

Florida’s health insurance program for children.

FloridaHealthFinder.gov

State-run site to compare and enroll in health plans.

Federally funded Navigator organization: University of South Florida, (813) 396-2898

Florida Office of Insurance Regulation

Licenses and oversees health insurers, brokers, and agents. Helps consumers with complaints. Reviews annual health insurance rate changes.

Medicare Rights Center

National service with a call center providing advice and information for people with Medicare.

Looking for more information about other options in your state?

Need help navigating health insurance options in Florida?

Explore more resources for options in FL including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”A quick guide to the Health Insurance Marketplace” HealthCare.gov ⤶ ⤶

- ”Marketplace 2026 Open Enrollment Period Report: National Snapshot” CMS Newsroom. Jan. 28, 2026 ⤶

- “Individual PPACA Market Monthly Premiums for Plan Year 2026” Florida Office of Insurance Regulation. Oct. 16, 2025 ⤶ ⤶ ⤶ ⤶ ⤶

- ”Individual Market Availability by Company” Florida Office of Insurance Regulation. Accessed Nov. 2, 2025 ⤶

- ”Florida House Bill 221” BillTrack50. Enacted 2015. ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Individual PPACA Market Monthly Premiums for Plan Year 2026” Florida Office of Insurance Regulation. Aug. 14, 2025 *The above is based on the most current data available. ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Mar. 14, 2026 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Mar. 14, 2026 ⤶ ⤶

- “A quick guide to the Health Insurance Marketplace®” HealthCare.gov, Accessed Mar. 14, 2026 ⤶

- “Important facts about The Marketplace; The Health Insurance Marketplace for American Indians and Alaska Natives” CMS.gov, Accessed Mar. 14, 2026 ⤶

- “Entities Approved to Use Enhanced Direct Enrollment” CMS.gov, Dec. 8, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- ”Effectuated Enrollment: Early 2025 Snapshot and Full Year 2024 Average” CMS.gov, July 24, 2025 ⤶

- ”Individual Market Availability by Company” Florida Office of Insurance Regulation. Accessed Nov. 6, 2025 ⤶ ⤶

- ”Cigna Healthcare’s 2026 Footprint” Cigna. Accessed June 1, 2026 ⤶

- ”Effectuated Enrollment: Early 2025 Snapshot and Full Year 2024 Average” CMS.gov, July 24, 2025 ⤶

- ”See Plans & Prices” (zip 33301) HealthCare.gov. Accessed Oct. 31, 2025 ⤶

- Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums. The Commonwealth Fund. December 2014. ⤶

- Individual PPACA Market Monthly Premiums for Plan Year 2016. Florida Office of Insurance Regulation, August 2015. ⤶

- Individual PPACA Market Monthly Premiums for Plan Year 2017. Florida Office of Insurance Regulation, September 2016. ⤶

- 2018 Rate Hikes. ACA Signups. October 2017. ⤶

- 2019 Rate Hikes. ACA Signups. October 2018. ⤶

- 2020 Rate Changes. ACA Signups. October 2019. ⤶

- Individual PPACA Market Monthly Premiums for Plan Year 2021 Florida Office of Insurance Regulation, September 2020. ⤶

- Florida Office of Insurance Regulation Announces 2022 PPACA Individual Market Health Insurance Plan Rates. Florida Office of Insurance Regulation, September 2021. ⤶

- Individual PPACA Market Monthly Premiums for Plan Year 2023 Florida Office of Insurance Regulation, September 2022 ⤶

- Individual PPACA Market Monthly Premiums for Plan Year 2024 Florida Office of Insurance Regulation, August 2023. ⤶

- ”Individual PPACA Market Monthly Premiums for Plan Year 2025” Florida Office of Insurance Regulation, Aug. 28, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶ ⤶

- “ASPE Issue Brief (2014) ” ASPE, 2015 ⤶

- “ Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report ”, HHS.gov, 2015 ⤶

- “ HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files ” CMS.gov, 2017 ⤶

- “ 2018 Marketplace Open Enrollment Period Public Use Files ” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files ” CMS.gov, 2019 ⤶

- “ 2020 Marketplace Open Enrollment Period Public Use Files ” CMS.gov, 2020 ⤶

- “ 2021 Marketplace Open Enrollment Period Public Use Files ” CMS.gov, 2021 ⤶

- “ 2022 Marketplace Open Enrollment Period Public Use Files ” CMS.gov, 2022 ⤶

- “ Health Insurance Marketplaces 2023 Open Enrollment Report ” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, Accessed August 2023 ⤶