Medicare in Kansas

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Kansas

Medicare enrollment in Kansas

588,163 Kansas residents were enrolled in Medicare as of August 2024,1 amounting to more than 17% of the state’s population2 — very similar to the share of the total United States population enrolled in Medicare.2

About 90% of Medicare beneficiaries in Kansas are eligible due to their age (ie, being at least 65), while more than 10% are under 65 and eligible for Medicare due to a disability that lasts at least 24 months1 (people with amyotrophic lateral sclerosis (ALS) or end-stage renal disease (ESRD) do not have to wait 24 months for Medicare eligibility).

Learn about Medicare plan options in Kansas by contacting a licensed agent.

Explore our other comprehensive guides to coverage in Kansas

The ACA Marketplace allows individuals and families to shop for and enroll in ACA-compliant health insurance plans. Subsidies may be available based on household income to help lower costs.

Hoping to improve your smile? Dental insurance may be a smart addition to your health coverage. Our guide explores dental coverage options in Kansas.

Learn about Kansas’ Medicaid expansion, the state’s Medicaid enrollment and Medicaid eligibility.

Short-term health plans provide temporary health insurance for consumers who may find themselves without comprehensive coverage. Learn more about short-term plan availability in Kansas.

Frequently asked questions about Medicare in Kansas

What is Medicare Advantage?

Original Medicare is available throughout the United States. And in most parts of the country, Medicare Advantage plans are available as an alternative, for people who prefer private health insurance. Medicare Advantage plans are available in most counties3

Seventeen percent of Kansas Medicare beneficiaries selected private Medicare Advantage plans as of 2018,4 which was much lower than the 35% of all Medicare beneficiaries nationwide who had Medicare Advantage enrollment at that point.5 The remaining 83% of the state’s Medicare beneficiaries had opted instead for coverage under Original Medicare.

Total Medicare coverage enrollment has been growing nationwide, but Medicare Advantage enrollment has been growing even faster. As of August 2024, nearly 33% of Medicare beneficiaries in Kansas (196,518 people) were enrolled in private plans obtained through Medicare Advantage insurers.1

Medicare Advantage offers all of the benefits of Original Medicare (hospital inpatient care plus outpatient services), plus additional benefits like a cap on out-of-pocket costs, and in most cases, integrated Medicare Part D prescription drug coverage (the cap on out-of-pocket costs does not apply to the Medicare Part D prescription drug coverage, however).

Many Medicare Advantage plans also provide additional benefits and programs, such as dental and vision coverage, a 24-hour nurse hotline, and fitness. And many Medicare Advantage plans have no monthly premiums other than the cost of Medicare Part B.6 But there are tradeoffs and limitations: Medicare Advantage plans have more limited networks than Original Medicare, and total out-of-pocket costs under a Medicare Advantage plan are typically higher than they would be with Original Medicare combined with Medigap and a stand-alone Medicare Part D prescription drug plan.6

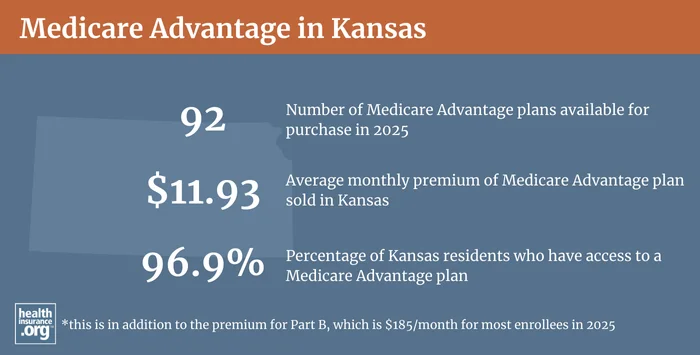

Depending on the county in which they live, residents in Kansas can select from between one and 40 Medicare Advantage plans for 2024.3

During the Medicare Annual Election Period each fall (October 15 to December 7), Medicare beneficiaries can switch between Medicare Advantage and Original Medicare, and can also make changes to their Medicare Part D prescription drug coverage (but in most cases, there is not an opportunity to make a change to Medigap coverage without medical underwriting and/or a penalty). There is also a Medicare Advantage Annual Enrollment Period (January 1 to March 31) during which people who are already enrolled in Medicare Advantage plans can switch to a different Medicare Advantage plan or drop their Medicare Advantage plan and enroll in Original Medicare instead.

What are Medigap plans?

Medigap plans are used to supplement Original Medicare, covering some or all of the out-of-pocket costs (for coinsurance and deductibles) that people would otherwise incur if they only had Original Medicare on its own. More than half of all Medicare beneficiaries have supplemental healthcare coverage from an employer’s plan or Medicaid.7 But optional private Medigap plans are available to Original Medicare beneficiaries who don’t have supplemental coverage from another source.

250,326 Kansas residents were enrolled in Medigap plans as of 2022.8

The Kansas Insurance Department publishes a Medigap buyer’s guide, available here. There are 41 insurers offering Medigap plans in Kansas for 2025.9 Almost all of them use attained-age rating for setting monthly premiums, although a few use issue-age rating (here’s how they both work).

Medigap plans are standardized under federal rules, and people are granted a six-month window, when they turn 65 and enroll in Original Medicare, during which coverage is guaranteed issue for Medigap plans. Federal rules do not, however, guarantee access to a Medigap plan if you’re under 65 and eligible for Medicare as a result of a disability.

But Kansas is among the majority of the states with rules to ensure at least some access to Medigap plans for enrollees under the age of 65. And the consumer protections in Kanas are among the nation’s strongest. In Kansas, all Medicare beneficiaries — including those who gain eligibility due to a disability and those who become eligible when they turn 65 — have the same guaranteed issue access to Medigap coverage (see page 4 of the Kansas Medigap buyer’s guide).

Starting when a person is enrolled in Medicare Part B (regardless of their age), they have a six-month window during which coverage is guaranteed issue for all available Medigap plans. As long as the person enrolls during their six-month open enrollment window, insurers are required to charge younger, disabled beneficiaries the same premiums that apply to a 65-year-old. This is a stronger consumer protection than most states have; in the majority of the states where Medigap plans are guaranteed-issue for people under age 65, the insurers are allowed to charge higher prices for that population.

As is the case in every state, Kansas residents who are enrolled in Medicare prior to age 65 still have a guaranteed-issue Medigap open enrollment period when they turn 65, regardless of whether they already had Medigap coverage prior to turning 65. But since Kansas does not allow Medigap insurers to charge higher rates for younger enrollees, this is not as important as it is in other states where disabled beneficiaries pay much higher premiums and can then switch to a lower-cost plan when they turn 65.

What is Medicare Part D?

Original Medicare does not cover outpatient prescription drugs. But Medicare beneficiaries can get prescription drug coverage through Medicaid or an employer-sponsored plan (offered by a current or former employer). For people who don’t have access to either of those, a Medicare Part D prescription drug plan is available to provide prescription drug coverage to Medicare beneficiaries. Medicare Part D prescription drug coverage can be obtained as a stand-alone prescription drug plan or integrated with a Medicare Advantage plan.

As of August 2024, there were 282,599 Kansas Medicare beneficiaries with coverage under stand-alone Medicare Part D prescription drug plans.1 Another 182,944 Kansas Medicare beneficiaries had Medicare Part D prescription drug coverage integrated with a Medicare Advantage plan.1

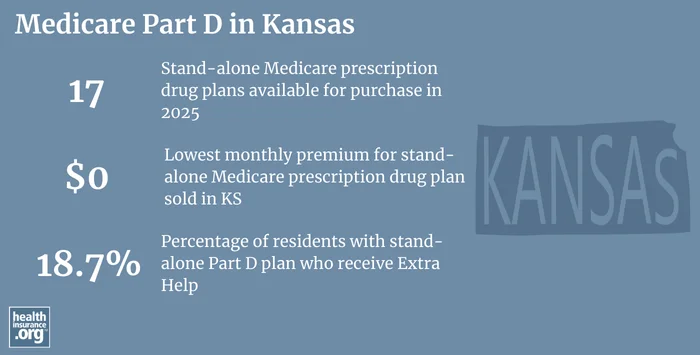

For 2025 coverage, there are 17 stand-alone Medicare Part D prescription drug plans available in Kansas, with monthly premiums starting at $0 per month.10

Medicare Part D prescription drug enrollment is available during the Medicare Annual Enrollment Period each fall, from October 15 to December 7. You can change your plan multiple times during that period; the last plan change you make will take effect January 1 of the coming year.

What additional resources are available for Medicare beneficiaries and their caregivers in Kansas?

Need help with your Medicare application in Kansas? Got questions about Medicare eligibility in Kansas? You can contact SHICK — Senior Health Insurance Counseling for Kansas — with questions related to Medicare in Kansas.

The Kansas Insurance Department’s website provides a comprehensive Medigap resource for people filing for Medicare benefits in Kansas and wishing to supplement the coverage with a Medigap plan. The page includes a general information guide to Medigap plans as well as a rate comparison tool.

Medicare.gov, maintained by CMS (the Centers for Medicare & Medicaid Services) provides information about every aspect of Medicare, and includes a healthcare provider finder tool as well as a plan finder tool that can help you determine which insurers for Medigap, Medicare Part D, and Medicare Advantage are offered by private insurance companies approved by Medicare.

The Medicare Rights Center provides Medicare-related assistance throughout the United States. They maintain a website and a call center where consumers can get answers to a wide range of questions about Medicare.

Looking for more information about other options in your state?

Need help navigating health insurance options in Kansas?

Explore more resources for options in KS including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Kansas.” Centers for Medicare & Medicaid Services Data. Accessed December, 2024. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- “U.S. Census Bureau Quick Facts: U.S. & Kansas.” U.S. Census Bureau, July 1, 2023. ⤶ ⤶

- ”Medicare Advantage 2024 Spotlight: First Look” KFF.org Nov. 15, 2023 ⤶ ⤶

- Medicare Monthly Enrollment – Kansas (2018).” Centers for Medicare & Medicaid Services Data, May 2023. ⤶

- Monthly Medicare Enrollment – US (2018).” Centers for Medicare & Medicaid Services Data, May 2018. ⤶

- “Understanding Medicare Advantage Plans.” Medicare.gov. Page 6. Accessed September 22, 2023. ⤶ ⤶

- Ochieng, Nancy, Gabrielle Clerveau, and Tricia Neuman. “A Snapshot of Sources of Coverage among Medicare Beneficiaries.” Kaiser Family Foundation, August 14, 2023. ⤶

- ”The State of Medicare Supplement Coverage” AHIP. May 2024 ⤶

- “Explore your Medicare coverage options.” Medicare.gov. Accessed October, 2024. ⤶

- ”Fact Sheet: Medicare Open Enrollment for 2025” (50) Centers for Medicare & Medicaid Services. Sep. 27, 2024 ⤶