Find New Mexico Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

New Mexico health insurance Marketplace guide

This guide to health insurance in New Mexico, including the FAQs below, is designed to help you understand the coverage options and potential financial assistance available to you and your family.

Starting in the fall of 2021, New Mexico began using its own state-based health insurance exchange – beWellnm (also referred to as NMHIX, or New Mexico Health Insurance Exchange). Before that, the state used the federally facilitated HealthCare.gov Marketplace platform. New Mexico’s Health Insurance Marketplace plans are used by people who aren’t eligible for Medicare, Medicaid, or an affordable employer-sponsored health plan.

New Mexico residents can use beWellnm to shop for individual and family health plans offered by four private health insurance carriers for 2026 (plus one dental insurer).4 Full-price premiums increased substantially for 2026 (see details below), but New Mexico’s state-based subsidy program was enhanced to make coverage more affordable in 2026 (details below).

New Mexico is among the states where additional state-funded subsidies are available through the Marketplace, in addition to federal subsidies. New Mexico’s state-funded subsidies were expanded for 2024,5 and for 20256 and were expanded again for 2026 to offset the expected reductions in the federal subsidy program (more details below).78

As a result of New Mexico’s expanded state subsidies, residents were fully insulated from the reduction in federal subsidies, as New Mexico backfilled 100% of the difference using state funds.9 As a result, New Mexico’s Marketplace enrollment grew significantly for 2026, while nationwide Marketplace enrollment declined.10

NMHIX previously processed premium payments, and was one of only two state-based Marketplaces (the other is Rhode Island’s) that did this. But NMHIX shifted away from this as of 2026, and enrollees now pay their premiums directly to their insurance companies, as is the case in most other states.11

Frequently asked questions about health insurance in New Mexico

Who can buy Marketplace health insurance in New Mexico?

To be eligible to enroll in private health coverage through beWellnm, you must:12

- Be lawfully present in the United States, and live in New Mexico

- Not be incarcerated

- Not be enrolled in Medicare13

So most New Mexico residents can enroll in a health plan through the exchange.14 But a more pressing question for most people is eligibility for financial assistance in the form of state and federal subsidies through beWellnm.

To qualify for income-based federal Advance Premium Tax Credits (APTC), New Mexico Premium Assistance, federal cost-sharing reductions (CSR), or New Mexico’s State Out-of-Pocket Assistance (SOPA),15 you must:

- Not have access to an affordable plan offered by an employer. If you are eligible to sign up for an employer’s plan and aren’t sure whether it’s considered affordable, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies via beWellnm.

- Not be eligible for New Mexico Centennial Care (Medicaid).

- Not be eligible for premium-free Medicare Part A.16

- Not be able to be claimed by someone else as a tax dependent.17

- If you’re married, you must file a joint tax return with your spouse.17 (with very limited exceptions)18

In addition to those basic parameters, beWellnm subsidy eligibility will depend on your household’s income.

When can I enroll in an ACA-compliant plan in New Mexico?

In New Mexico, the open enrollment period for 2026 coverage ended on January 15, 2026.19

Open enrollment will be shorter starting in the fall of 2026, due to a federal rule that was finalized in 2025. State-run exchanges will be required to end open enrollment no later than December 31, and all plans selected during open enrollment will take effect January 1.

Outside of the annual open enrollment period, you may still be able to enroll or make a plan change if you experience a qualifying life event, such as giving birth or losing other health coverage.

New Mexico also offers an Easy Enrollment Program that enables uninsured residents to initiate the health insurance enrollment process through their state tax returns.2021

Enrollment in New Mexico Centennial Care (Medicaid) is available year-round.

For a few years, New Mexico required off-exchange open enrollment to end on December 15, a month before the open enrollment period ended for on-exchange plans.22 But in late 2025, New Mexico repealed that rule, and noted that open enrollment for off-exchange plans would continue until January 15, following the same schedule used for on-exchange plans.23 But as noted above, open enrollment will no longer continue past the end of December in any state as of the fall of 2026.

How do I enroll in a Marketplace plan in New Mexico?

To enroll in an ACA Marketplace/exchange plan in New Mexico, you can:

- Visit beWellnm – New Mexico’s health insurance exchange – to compare the health plans available in your area, determine whether you’re eligible for financial assistance (including federal and state subsidies), and enroll in coverage during open enrollment or during a special enrollment period.

- Enroll in a beWellnm plan with the help of an insurance agent or broker, Navigator, or certified application counselor.

- Contact beWellnm by phone at 1-833-862-3935.

How can I find affordable health insurance in New Mexico?

When you enroll in coverage through beWellnm, you may find that you’re eligible for financial assistance. And the assistance may be more robust than it is in many other states, as both federal and state subsidy programs are available in New Mexico. The state subsidies were once again expanded for 2026, for the third year in a row, making New Mexico the only state that was able to fully backfill the reduction in federal subsidies.9

As a result of the Affordable Care Act (ACA), federal premium subsidies (advance premium tax credits, or APTC) are available depending on your income. If you’re eligible for APTC, it will reduce the amount you pay for your health coverage each month, as long as you enroll in a metal-level plan through beWellnm.

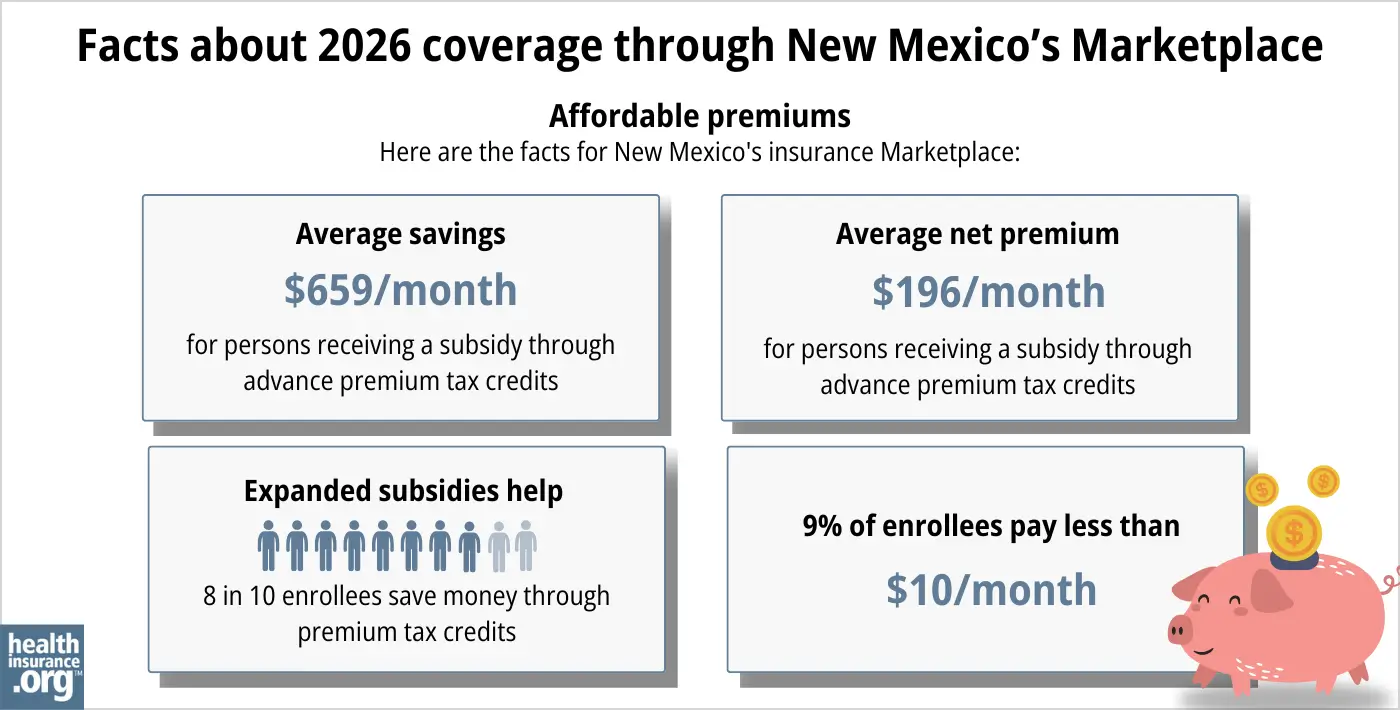

During the open enrollment period for 2026 coverage, 82% of the people who enrolled through beWellnm qualified for federal APTC that averaged $659/month, bringing the average net premium (for people who qualified for APTC) to $196/month24 (up from $86/month in 2025).25

But that’s only addressing federal subsidies. New Mexico fully backfilled the reduction in federal APTC for 2026, making coverage much more affordable than it would otherwise have been. So the number of people who qualified for financial assistance in New Mexico was higher than the federal report showed, and the average total financial assistance received by enrollees was also more substantial than indicated on the federal report.26 There’s no “subsidy cliff” in New Mexico in 2026, and New Mexico enrollees didn’t experience the sort of sticker shock that was common in other states.

Applicants with household income up to 250% of the federal poverty level are also eligible for federal cost-sharing reductions (CSR), which will reduce the deductible and other out-of-pocket expenses for Silver-level plans. Thirty-six percent of beWellnm enrollees were receiving federal CSR benefits as of 2026.24 (Additional state-funded cost-sharing reductions are also available in New Mexico, and are explained below.)

Source: CMS.gov1

Extra state subsidies make coverage more affordable

In addition to the federal subsidies, New Mexico is among the states where extra state-funded subsidies are available. And these subsidies have expanded each year since they debuted, making coverage more affordable for more people.

New Mexico offers both state premium subsidies and state cost-sharing reductions.(Plans that include additional state cost-sharing reductions are labeled “turquoise.”) The state subsidy program is funded by the Health Care Affordability Fund (HCAF).15

For 2026, New Mexico’s state-funded premium subsidies were expanded to make up for the reduction in federal subsidies,15 including a provision to include assistance for enrollees with household income above 400% of FPL7 and for recent immigrants with income below FPL.8 Those two populations lost federal subsidies altogether in 2026 (due to the expiration of federal premium subsidy enhancements and the One Big Beautiful Bill, respectively). So New Mexico expanded the state subsidy program in an effort to ensure these populations could still obtain affordable coverage.

So at any income level, New Mexico residents are protected from the impact of the reduction in federal subsidies. Although several other states offer state-funded subsidies, New Mexico is the only one that was able to fully backfill the loss of federal subsidies for 2026.

History of New Mexico’s state-funded subsidy program

As of 2023, New Mexico began offering state-funded premium subsidies (for applicants with income up to 400% of the federal poverty level, or FPL) and cost-sharing assistance (for applicants with income up to 300% of FPL), in addition to the federal premium subsidies and cost-sharing reductions.27

New Mexico’s cost-sharing reductions (state out-of-pocket assistance, or SOPA) were expanded for 2024, ensuring that people with household income up to 300% of FPL could get plans with 90% actuarial value (ie, platinum-level coverage).28 And that was expanded again for 2025, so that applicants with household income up to 400% of FPL could get plans with 90% actuarial value.29 The 90% actuarial value plans are called “Turquoise 3.”

As explained above, New Mexico further expanded the state-subsidy program to address the fact that federal premium subsidies are expected to shrink significantly in 2026. The federal subsidy enhancements that have been in effect since 2021 are scheduled to expire at the end of 2025 unless Congress acts to extend them. If they expire, federal subsidies will be smaller in 2026, and will end altogether for some enrollees. New Mexico is making up the difference with its state subsidy program.

Starting in 2023, New Mexico no longer allows health insurers in the individual/family market to add a tobacco surcharge to smokers’ premiums (the state joined several others that had already imposed similar rules).

Starting with the 2024 plan year, New Mexico has standardized plans available at the Silver, Gold, and Turquoise level.30

Depending on your income and circumstances, you may be able to enroll in free or low-cost health coverage through Centennial Care (New Mexico Medicaid). Learn more about whether you might be eligible for Medicaid in New Mexico.

As was the case in all states, Medicaid disenrollments resumed in New Mexico in mid-2023, after being paused for three years during the pandemic. But New Mexico took some fairly unique steps to help people transition from Medicaid to the Marketplace: For those with income up to 400% of the poverty level, the state covered their first month of after-subsidy premiums for the Marketplace plan, and beWellnm also offered retroactive effective dates (the first of the month during which the person applied) for the new Marketplace plans when a person transitioned away from Centennial Care Medicaid.31

How many insurers offer Marketplace coverage in New Mexico?

For 2026, four insurers offer exchange plans in New Mexico,32 The same four insurers offered coverage for 2025.

- Blue Cross Blue Shield of New Mexico

- Molina

- Presbyterian Health Plan

- UnitedHealthcare of New Mexico

For several years, New Mexico had one of the few remaining ACA-created CO-OPs, but it closed at the end of 2020, leaving just three CO-OPs still operational (as of 2026, those three CO-OPs offer coverage in four states).

Are Marketplace health insurance premiums increasing in New Mexico?

For 2026, the following average rate changes were approved by the New Mexico Office of the Superintendent of Insurance (OSI), amounting to an overall average increase of 35.7% for full-price (pre-subsidy) premiums:33

New Mexico’s ACA Marketplace Plan 2026 APPROVED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Blue Cross Blue Shield of New Mexico (Health Care Service Corporation) | 38.7% |

| Molina | 15.3% |

| Presbyterian Health Plan | 29.3% |

| UnitedHealthcare of New Mexico | 53% |

Source: New Mexico Office of the Superintendent of Insurance33 and New Mexico SERFF34

The weighted average pre-subsidy rate increase for 2026 was 35.7% in the individual market in New Mexico. And in most states, the expiration of federal subsidy enhancements resulted in a sharp increase in average after-subsidy premiums.35 But as noted above, New Mexico’s state subsidy program was expanded to backfill the reduction in federal subsidies.9

For perspective, here’s an overview of how average full-price premiums have changed over the years in New Mexico’s individual/family market:

- 2015: Average decrease of 1.7%.36

- 2016: Average increase of 4%.37

- 2017: Average increase of 28.4%.38

- 2018: Average increase of 30%.39

- 2019: Average decrease of 1%.40

- 2020: Average increase of 0.9%.41

- 2021: Average decrease of 1.5%.42

- 2022: Average increase of 15.5%.43

- 2023: Average increase of 11.3%.44 (before Friday Health Plans, which had the largest increase, announced that they would exit the market).

- 2024: Average increase of 7%.45

- 2025: Average increase of 10.2%.46

How many people are insured through New Mexico's Marketplace?

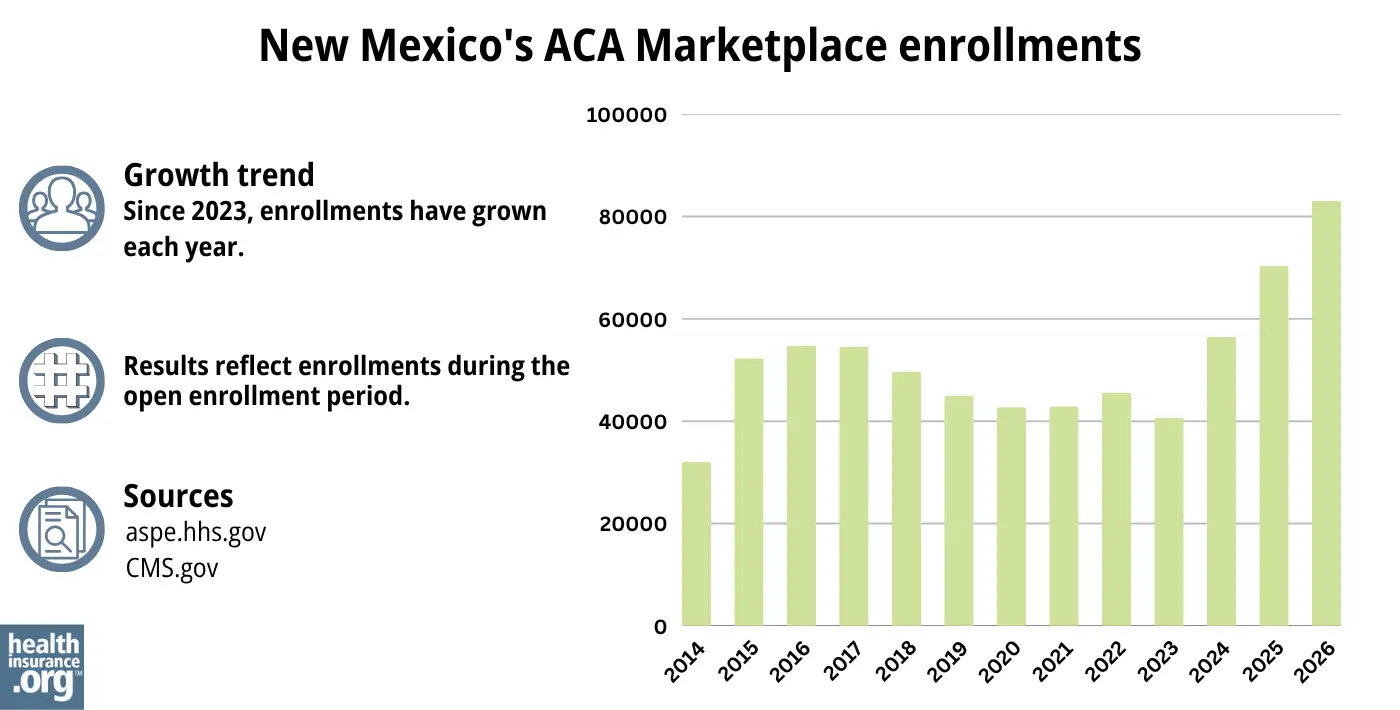

During the open enrollment period for 2026 coverage, 83,103 people enrolled in plans through New Mexico’s exchange.24 This was a new record high, and an 18% increase over the previous record high that has been set the year before.47 setting a new record high.

Source: 2014,48 2015,49 2016,50 2017,51 2018,52 2019,53 2020,54 2021,55 2022,56 2023,57 2024,58 202547 20261

New Mexico was unique in seeing such a large enrollment increase for 2026. Indeed, overall nationwide Marketplace enrollment declined by nearly 5% in 2026. But because New Mexico used state funds to fully offset the reduction in federal premium subsidies, the state was able to avoid the coverage losses that plagued much of the country for 2026.59

What health insurance resources are available to New Mexico residents?

beWellnmThe state’s exchange for small businesses, individuals, and families.

Health Action New MexicoA consumer advocacy organization working to improve healthcare access and affordability in New Mexico.

New Mexico Human Services Department

Administers Centennial Care (Medicaid) and various other social services programs in the state.

New Mexico Office of the Superintendent of Insurance

Licenses and regulates health insurance companies in New Mexico, as well as brokers and agents; can provide assistance and information to consumers who have questions or complaints about regulated entities.

New Mexico State Health Insurance Assistance Program

A resource for New Mexico Medicare beneficiaries and their caregivers.

Looking for more information about other options in your state?

Need help navigating health insurance options in New mexico?

Explore more resources for options in NM including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶

- “New Mexico SERFF Filings” and “New Mexico Rate Review Submissions” RateReview.HealthCare.gov. Accessed Sep. 14, 2025 *The above is based on the most current data available. ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” and “Marketplace 2025 Open Enrollment Period Report: National Snapshot” Centers for Medicare & Medicaid Services, April 2026 ⤶

- ”Who Are the Carriers?” BeWell. New Mexico’s Health Insurance Marketplace. Accessed Apr. 1, 2026 ⤶

- 2024 Plan Year Health Insurance Marketplace Affordability Program Policy and Procedures Manual. New Mexico Office of the Superintendent of Insurance. April 2023. ⤶

- ”2025 Plan Year Health Insurance Marketplace Affordability Program, Policy and Procedures Manual” New Mexico Office of the Superintendent of Insurance. April 26, 2024 ⤶

- ”Addendum #1 to the New Mexico Health Insurance Marketplace Affordability Program Policy and Procedures Manual for the 2026 Plan Year” New Mexico Health Care Authority. Accessed Dec. 12, 2025 ⤶ ⤶

- ”Addendum #2 to the New Mexico Health Insurance Marketplace Affordability Program Policy and Procedure Manual for the 2026 Plan Year” New Mexico Health Care Authority. Accessed Dec. 12, 2025 ⤶ ⤶

- ”New Federal Changes” BeWell New Mexico’s Health Insurance Marketplace. Accessed Dec. 12, 2025 ⤶ ⤶ ⤶

- ”EXCLUSIVE! FINAL 2026 Open Enrollment Report published: 23.1M QHP selections; 25.0M w/BHPs, down 1.2M y/y (Part 1)” ACA Signups. Mar. 27, 2026 ⤶

- ”How to Make Your Payment” New Mexico’s Health Insurance Marketplace. Accessed Apr. 1, 2026 ⤶

- ”New Mexico Health Insurance Exchange Policy Manual for Plan Year 2026” beWellnm, NMHIX. Accessed Dec. 12, 2025 ⤶

- Medicare and the Health Insurance Marketplace. Medicare.gov. Accessed Dec. 12, 2025 ⤶

- “Frequently Asked Questions; New Mexico State-Based Exchange” beWellnm, Accessed Dec. 12, 2025 ⤶

- ”The Health Care Affordability Fund” New Mexico Legislative Finance Committee. June 25, 2025 ⤶ ⤶ ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Dec. 12, 2025 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Dec. 12, 2025 ⤶ ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- “Enrollment” beWellnm, Accessed Dec. 12, 2025 ⤶

- NM Easy Enrollment Program. Health Action New Mexico. Accessed Apr. 1, 2026 ⤶

- ”Use Your State Tax Form for Easy Enrollment” beWellnm. Accessed Apr. 1, 2026 ⤶

- Application of Open Enrollment and Special Enrollment Periods to Individual Off-Exchange Plans. New Mexico Office of the Superintendent of Insurance. December 2023. ⤶

- ”Application of Open Enrollment and Special Enrollment Periods to Individual Off-Exchange Plans” New Mexico Office of the Superintendent of Insurance. Nov. 13, 2025 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov, Mar. 27, 2026 ⤶ ⤶ ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶

- ”Federal and State Policy Changes” beWellnm. Accessed Apr. 1, 2026 ⤶

- “Health Insurance Marketplace Affordability Program” NM Office of the Superintendent of Insurance, October 2022 ⤶

- “2024 Plan Year Health Insurance Marketplace Affordability Program Policy and Procedures Manual” New Mexico Office of the Superintendent of Insurance, April 13, 2023 ⤶

- “2025 Plan Year Health Insurance Marketplace Affordability Program, Policy and Procedures Manual”New Mexico Office of the Superintendent of Insurance. April 26, 2024 ⤶

- “Standardized Health Plan Requirements for the 2024 Plan Year” beWellnm. January 2023 ⤶

- Minimizing Coverage Disruptions After the Federal Medicaid Continuous Coverage Requirement Expires During the 2023 Plan year. New Mexico Office of the Insurance Commissioner. February 2023. ⤶

- “New Mexico SERFF Filings” and “New Mexico Rate Review Submissions” RateReview.HealthCare.gov. Accessed Dec. 12, 2025 ⤶

- ”New Mexico Announces Significant Rate Increases for 2026 ACA Plans, State Premium Support Will Continue to Help Enrollees with Costs” New Mexico Office of the Superintendent of Insurance. Aug. 19, 2025 ⤶ ⤶

- ”New Mexico SERFF” (to obtain approved average increases for each carrier). Accessed Sep. 14, 2025 ⤶

- ”ACA Marketplace Premium Payments Would More than Double on Average Next Year if Enhanced Premium Tax Credits Expire” KFF.org. Sep. 30, 2025 ⤶

- New Mexico: 2015 QHP Premiums To DROP 1.65% (Weighted Average). ACA Signups. September 2014. ⤶

- FINAL PROJECTION: 2016 Weighted Avg. Rate Increases: 12-13% Nationally* ACA Signups. October 2015. ⤶

- Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC). ACA Signups. October 2016. ⤶

- 2018 Rate Hikes. ACA Signups. October 2017. ⤶

- 2019 Rate Hikes. ACA Signups. October 2018. ⤶

- 2020 Rate Changes. ACA Signups. October 2019. ⤶

- 2021 Rate Changes. ACA Signups. October 2020. ⤶

- 2022 Rate Changes. ACA Signups. October 2021. ⤶

- UPDATED: FINAL Unsubsidized 2023 Premiums: +6.2% Across All 50 States +DC. ACA Signups. Accessed November 2023. ⤶

- Calculated by healthinsurance.org, based on premium and enrollment data in New Mexico SERFF filings. NM SERFF. Accessed December 2023. ⤶

- ”State OSI Announces 2025 Qualified Health Plan Rates … A Dozen Healthcare Plans For Less Than $10 A Month” Los Alamos Daily Post. Oct. 3, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶ ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “2023 Marketplace Open Enrollment Period Public Use Files” CMS.gov, March 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “EXCLUSIVE! FINAL 2026 Open Enrollment Report published: 23.1M QHP selections; 25.0M w/BHPs, down 1.2M y/y (Part 1)” ACA Signups. Mar. 27, 2026 ⤶