Health Insurance Marketplace by State

Each state runs its health insurance Marketplace differently – some use HealthCare.gov, while others manage their own Marketplaces, also called health insurance exchanges. Here’s what you need to know about how your state’s Marketplace works.

What is a health insurance Marketplace?

A health insurance Marketplace is a platform where consumers in the United States can purchase ACA-compliant individual/family health insurance plans and receive income-based premium subsidies to make coverage and care more affordable. During the open enrollment period for 2026 coverage, 23.1 million people selected Marketplace plans throughout the country,1 down from 24.3 million people the year before.2

Each state has just one official Marketplace, operated by the state, the federal government, or both. In the majority of the states, HealthCare.gov serves as the enrollment platform and runs the customer service call center. But some states run their own platforms, such as Covered California, New York State of Health, Connect for Health Colorado, and MNsure.

Health insurance Marketplaces vary by state

The Affordable Care Act (ACA), enacted in March 2010, called for the creation of a health insurance Marketplace in each state, but the practical implementation of those marketplaces varies from one state to another.

This overview answers questions about what the marketplaces are, what they offer, and how they work. You can select a state on the map below to see specific details about that state’s marketplace.

Frequently asked questions about health insurance Marketplaces

Who’s eligible to use the health insurance Marketplaces?

With the exception of people who are enrolled in Medicare coverage, virtually all Americans are eligible to use the health insurance Marketplace as long as they’re lawfully present in the U.S. (Note that this no longer includes DACA recipients).

But practically speaking, the Marketplaces are for people who need to buy their own health insurance because they don’t have access to employer-sponsored coverage, Medicare, or Medicaid. This includes people who are self-employed, people who are employed by a small business that doesn’t offer health benefits, and people who have retired before age 65 and are thus too young to be covered by Medicare.

The majority of Americans under age 65 get their coverage from an employer,3 which means they don’t need to use the Marketplace. They can choose to decline their employer’s coverage and select a plan in the Marketplace instead, but they won’t be eligible for financial assistance unless the employer’s coverage isn’t considered affordable and/or doesn’t provide minimum value.

Most Americans under age 65 who are eligible for Medicaid can use the Marketplace to enroll in Medicaid, or at least to determine their eligibility for Medicaid. In some states, the Medicaid enrollment process is completed via the Marketplace, while in other states, the Marketplace sends the consumer’s information to the state Medicaid agency to finalize the eligibility and/or enrollment process.

When can consumers buy health insurance through their Marketplace?

There is an open enrollment period each fall when people can enroll in coverage through the Marketplace or change their coverage for the coming year (the same open enrollment window also applies to individual market plans that are available outside the Marketplace, purchased directly from the insurance companies).

In most states, the open enrollment period in the fall of 2026 (for 2027 coverage) will run from November 1 to December 15. This is shorter than the window that was used for the past several years, due to a rule change finalized by the Trump administration.

However, some state-run exchanges will continue open enrollment until as late as December 31. The enrollment window cannot extend beyond that date in any state, and all plans selected during open enrollment must take effect January 1, as there is no longer an option for a February 1 effective date.

Outside of the annual open enrollment period, a special enrollment period is necessary to enroll in a plan through the health insurance Marketplace (or outside the Marketplace, directly through an insurer) or change to a different plan. Special enrollment periods are triggered by a variety of qualifying life events, and will give you at least 60 days to select a new medical plan.

How do health insurance Marketplaces help consumers?

In each state, the health insurance Marketplace allows consumers to select from among different qualified health plans offered by a variety of private health insurance companies. (In a few rural areas of the United States, only one insurer offers medical plans for sale in the Marketplace, but there are still a variety of plan options available).4

All qualified plans offered for sale in the Marketplace must be ACA-compliant – meeting standards established and enforced by the federal and state governments. So when a person shops in the health insurance Marketplace, they can be sure that the participating insurers will not use medical underwriting or exclude pre-existing conditions. All of the available plans will cover the ACA’s essential health benefits without annual or lifetime benefit caps.

Income-based premium subsidies and cost-sharing reductions are only available through the health insurance Marketplace, and are a key aspect of keeping health insurance premiums and out-of-pocket costs affordable for United States residents. (Note that in the majority of the states, it’s possible to enroll through the Marketplace via an enhanced direct enrollment entity, without using the Marketplace website.)

Income-based subsidies continue to be available in the Marketplace in 2026. But the expiration of federal subsidy enhancements at the end of 2025 caused a sharp increase in net premiums for Marketplace plans. As a result, some people didn’t or couldn’t continue to pay their premiums. Over the first few months of 2026, coverage was terminated due to non-payment of premiums for about 17% of the people who had selected Marketplace plans for 2026.5

What are the types of health insurance Marketplaces?

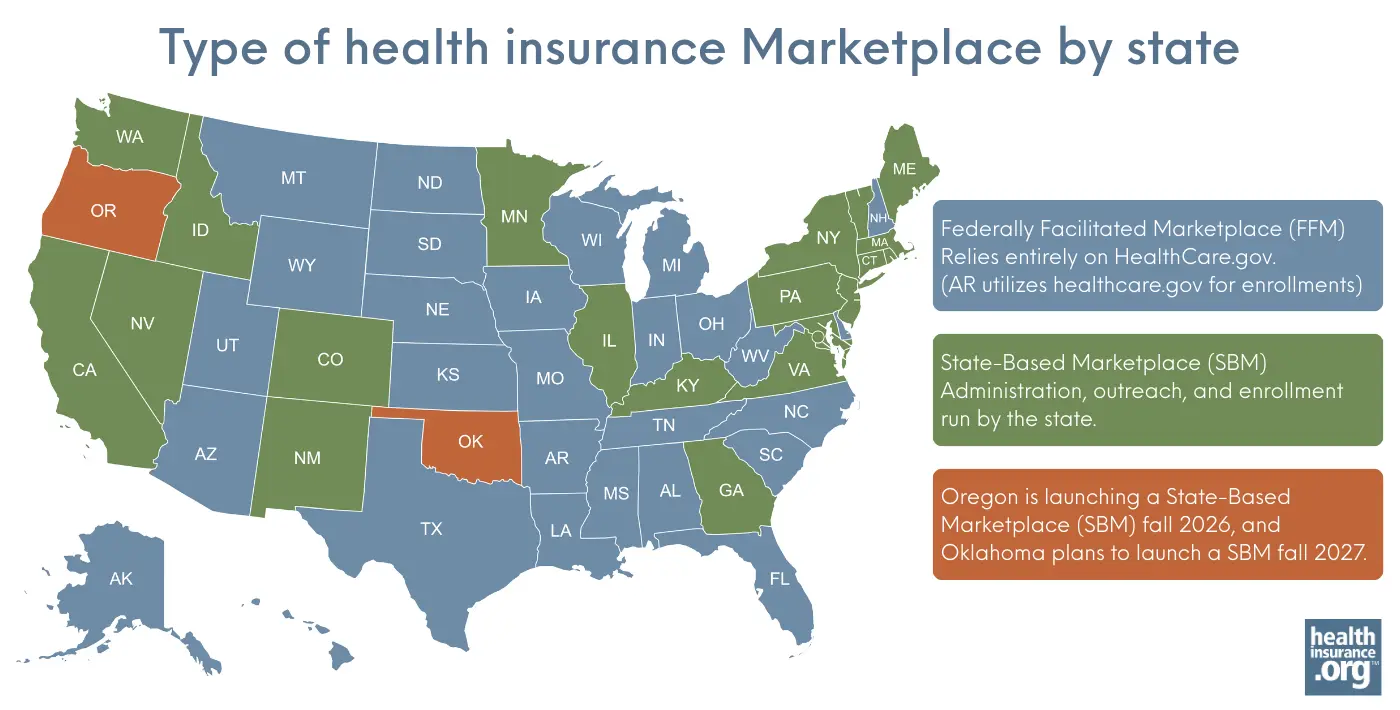

A state’s health insurance Marketplace can be run by the state, by the federal government, or both. As of the 2026 plan year:

- DC and 20 states have fully state-run Marketplaces, which means they oversee the Marketplace and operate their own website and call center, and fund their own Navigator programs (examples are GetCoveredNJ, Pennie, Vermont Health Connect, Washington Healthplanfinder, etc.). For 2026, this list includes Illinois, which previously did not have a fully state-run Marketplace.6

- Twenty-eight states rely fully on the federal government for their Marketplaces. They use the HealthCare.gov website and customer service call center, and receive federal Navigator funding.

- Two states (Arkansas and Oregon) have state-based Marketplaces that use the federal platform (SBM-FP), which means they oversee their own Marketplace and fund their own Navigator programs, but rely on HealthCare.gov for enrollment. Oregon plans to transition to a fully state-run Marketplace in the fall of 2026, for coverage effective in 2027.7

You can find more information here about the types of health insurance Marketplaces, how they work, which model each state uses, and how states’ approaches to this have changed over time.

Do I have to buy my health insurance through a Marketplace?

You are not required to buy coverage through the Marketplace. There is no longer a federal penalty for not having health coverage (although DC and four states have state-based penalties for people who choose to remain uninsured). And even when there was a federal penalty, people could choose to purchase their coverage off-exchange instead of buying a plan through the Marketplace (with the exception of DC, where individual and small-group coverage is only available through the Marketplace).

But if you don’t buy your coverage through the exchange, you cannot obtain premium tax credits8 or cost-sharing reductions,9 even if you’d otherwise be eligible for them (and most exchange enrollees are eligible for subsidies, even after the federal subsidy enhancements expired at the end of 2025).1 This is one of the primary reasons people shop in the Marketplace, as full-price individual health insurance premiums would simply be too costly for most people.

How much could you save on 2026 Marketplace coverage?

Compare health insurance Marketplace plans and check subsidy savings from a third-party insurance agency.

Footnotes

- “2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. Accessed May 13, 2026 ⤶ ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov. Accessed July 30, 2025 ⤶

- “Employer-Sponsored Health Insurance 101” KFF.org. October 8, 2025 ⤶

- “Plan Year 2025 Qualified Health Plan Choice and Premiums in HealthCare.gov Marketplaces” Centers for Medicare & Medicaid Services. Oct. 25, 2024 ⤶

- “One in Five HealthCare.gov Enrollees Dropped Insurance Coverage This Year” NOTUS. May 12, 2026 ⤶

- “Get Covered Illinois Transitions to a State-Based Marketplace this November” Get Covered Illinois. Aug. 11, 2025 ⤶

- “State-based Marketplace Project” Oregon.gov. Accessed Sep. 22, 2025 ⤶

- “Premium tax credit” heatlhcare.gov. Accessed October 6, 2025 ⤶

- “Cost sharing reduction (CSR)” heatlhcare.gov. Accessed October 6, 2025 ⤶