Medicare in Indiana

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Indiana

Medicare enrollment in Indiana

As of February 2026, Medicare enrollment in Indiana stood at 1,412,712 people.1

For most individuals, turning 65 is the path to Medicare enrollment. But younger individuals gain Medicare eligibility after they have been receiving disability benefits for 24 months, or if they have end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS). Nationwide, about 9% of all Medicare beneficiaries are under age 65.2 In Indiana, about 11% of Medicare beneficiaries were under age 65 as of early 2026.1

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Indiana’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

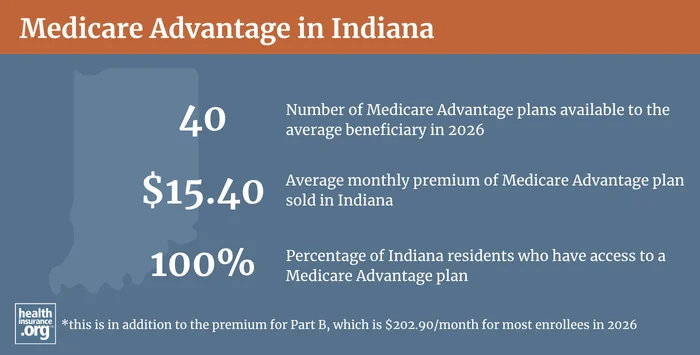

Medicare Advantage plan availability and enrollment in Indiana

As of February 2026, there were 723,196 Indiana Medicare beneficiaries enrolled in Medicare Advantage plans.1

Medicare Advantage plans are marketed in all counties in Indiana in 2026, but plan availability ranges from county to county. The average Medicare beneficiary in Indiana can choose from among 40 Medicare Advantage plans in 2026.3

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Indiana by contacting a licensed agent.

Medicare supplement (Medigap) plan availability in Indiana

According to AHIP, 370,851 Indiana Medicare beneficiaries were enrolled in Medigap plans (also known as Medicare Supplement insurance) in 20234 to supplement their Original Medicare coverage.

You can compare Medigap plans on Medicare.gov’s plan finder tool, or by using Indiana’s plan comparison tool. As of 2025, 39 insurers offered Medigap plans in Indiana.5

Unlike other private Medicare coverage (Medicare Advantage and Medicare Part D plans), federal rules do not provide an annual open enrollment window for Medigap plans. Instead, federal rules provide a one-time six-month window when Medigap coverage is guaranteed issue. This window starts when a person is at least 65 and enrolled in Medicare Part B. (You must be enrolled in both Part A and Part B to buy a Medigap plan.)

Federal rules do not guarantee access to Medigap plans for people who are under 65. However, the majority of the states have rules to ensure that disabled Medicare beneficiaries have at least some access to Medigap plans. Indiana requires Medigap insurers to make all policies guaranteed-issue for Medicare beneficiaries under the age of 65, during a six-month window when they’re first enrolled in Medicare.6,7

- For Medigap plans A, B, and D, the under-65 premiums must be the same as age-65 premiums.

- For other plans, such as Plan G or Plan N, the premium can be up to 200% of the age-65 premium.

Indiana also enacted legislation in 2025 to add a “birthday rule” starting in 2026. This allows Medigap enrollees (who are at least 65) to switch to another Medigap policy within 60 days of their birthday, without medical underwriting. The new policy must have the same benefits as their existing policy (so someone with Plan N can only switch to another Plan N, for example).8

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

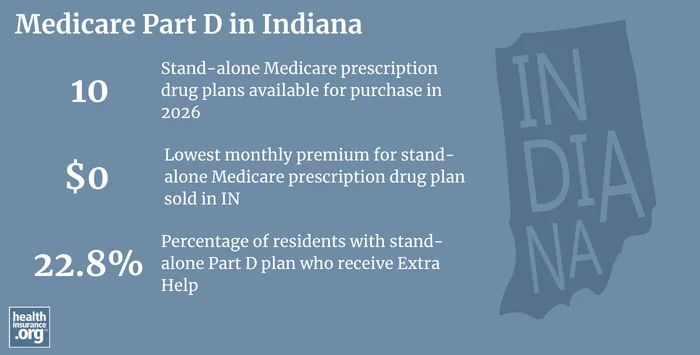

Medicare Part D plan availability and enrollment in Indiana

In Indiana, there are 10 stand-alone Part D plans for sale for 2026, with premiums as low as $0/month.9

As of February 2026, there were 1,192,401 Indiana Medicare beneficiaries who had Part D prescription coverage.1 About 47% had coverage under stand-alone Part D plans, while about 53% had Part D prescription coverage as part of their Medicare Advantage plans.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Indiana

Do you have questions about Medicare eligibility or need help enrolling in Medicare in Indiana?

- The Indiana Department of Insurance (IDOI) website provides information about Medicare eligibility, enrollment, and other general Medicare information, and also maintains a page about Medigap in Indiana.

- The Indiana State Health Insurance Assistance Program offers free assistance for Medicare beneficiaries. Call their central office at 1-800-452-4800 or find a local office.

- The Medicare Rights Center has a comprehensive national website and a helpful call center that can provide a variety of assistance with Medicare-related questions.

- Programs of All-Inclusive Care for the Elderly (PACE): A Medicare and Medicaid program that helps seniors receive the care they need in their homes and local communities, without having to move into a nursing home.

Looking for more information about other options in your state?

Need help navigating health insurance options in Indiana?

Explore more resources for options in IN including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Indiana” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data, May 2026. ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org. Dec. 9, 2025 ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025. Accessed Oct. 3, 2025 ⤶

- “Medicare Supplements Indiana” Indiana Department of Insurance, SHIP. Updated Sep. 23, 2025 ⤶

- “Indiana SB215” BillTrack50. Enacted Mar. 11, 2024 ⤶

- “Medicare Supplement Plans” Indiana Department of Insurance. Accessed Oct. 3, 2025 ⤶

- “Indiana HB1226” BillTrack50. Enacted Apr. 10, 2025 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” (44) Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶