Find California Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

California Health Insurance Marketplace Guide

Our California health insurance guide, including the FAQs below, is designed to help you understand the health coverage options and possible financial assistance available to you and your family. Having health coverage is especially necessary in California, as there’s a penalty on the state tax return for non-exempt filers who don’t have health coverage.1

California runs its own state-based health insurance Marketplace, called Covered California. Eleven private health insurers offer 2026 coverage for individuals and families via Covered California, down from 12 in 20252 (details below).

And California is one of the states where the exchange still offers a platform small businesses can use to purchase health coverage for their employees; three insurers offer small group plans through Covered California for 2026.3

California is among the states where state-funded subsidies are available to Marketplace enrollees, in addition to federal subsidies. In 2024 and 2025, California used state funds to provide additional cost-sharing subsidies, helping to reduce enrollees’ out-of-pocket costs.4 For 2026, the program shifted to a state-funded premium subsidy (see details below) in an effort to offset some of the reduction in federal subsidies due to the expiration of the federal subsidy enhancements at the end of 2025.

Under California rules, all of the plans sold in the exchange are standardized.5 Standardized plans are available in most states. But although most states also have non-standardized plans available through the exchange, California does not.6 This means that for certain services, all of the Covered California plans in a given metal level will have the same out-of-pocket costs.

A Covered California plan can be a great option if you need to buy your own health insurance. This includes people who aren’t eligible for Medicare or Medicaid, or don’t have an offer of affordable health insurance from an employer.

Who can buy health insurance on California’s Marketplace?

In order to sign up for private health coverage through Covered California, you must:7

- Be a California resident

- Not be incarcerated

- Not be enrolled in Medicare

- Be lawfully present in the United States (California expanded Medi-Cal (Medicaid) eligibility to undocumented immigrants, but that program is being phased out; undocumented adults are no longer eligible to enroll, although they can keep existing coverage for now).8

By those rules, most Californians can enroll in coverage through the exchange. But a bigger question for most people is financial assistance, and there are a few additional parameters to be eligible for subsidies through Covered California. To qualify for income-based Advance Premium Tax Credits (APTC), federal cost-sharing reductions (CSR), or California’s state-funded cost-sharing subsidies, you must:

- Not have access to affordable health coverage through an employer. If you have access to an employer’s plan but it seems too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies via Covered California.

- Not be eligible for Medi-Cal (California Medicaid).

- Not be eligible for premium-free Medicare Part A.9

- File a joint tax return if you’re married.10

- Not be able to be claimed by someone else as a tax dependent.10

Beyond those basic parameters, qualifying for Covered California subsidies will depend on how much your household earns. Here’s how household income is calculated under the ACA.

California AB570, enacted in October 2021, made California the first state in the country to provide a pathway for some policyholders to add their parents to their health plan as dependents.11

The legislation, which took effect in 2023, only applies to individual/family health plans (ie, not to plans that people get from an employer). Under the state law, a California resident with individual/family health coverage can cover parents as dependents, as long as the parents rely on the policyholder for at least 50% of their living expenses.

An earlier version of the bill would have applied to employer-sponsored health plans as well, but was opposed by business groups that worried about the cost. With the modification to make the legislation apply only to individual/family plans, the state expects that only about 15,000 people will use the option to add parents to their health plan.12

When can I enroll in an Affordable Care Act (ACA)-compliant plan in California?

The open enrollment period for 2026 individual market coverage in California ended on January 31, 2026.13 (In most states, open enrollment runs from November 1 through January 15.)

Starting in the fall of 2026, for coverage effective in 2027 and future years, open enrollment will not be allowed to extend past December 31, and all plans selected during open enrollment will take effect January 1. This is due to a federal rule change that was finalized in 2025. California has confirmed that open enrollment for 2027 coverage will run until December 31.14

The open enrollment window is your opportunity to select a new plan or switch to a different plan. The enrollment window applies to plans obtained via Covered California or directly from an insurer, but note that subsidies are only available through Covered California.

After the annual open enrollment window ends, you may still be eligible to enroll or make a plan change if you qualify for a special enrollment period. This generally requires a qualifying life event such as giving birth or losing other health coverage, although Native Americans can enroll anytime without a qualifying event.

In addition to the standard list of qualifying events that trigger special enrollment periods nationwide, Covered California will also grant a special enrollment period to a person whose medical provider leaves their health plan’s network while the person is undergoing treatment for one of the following:15

- Pregnancy

- A terminal illness

- An acute condition or serious chronic condition

- The care of a child during its first 36 months.

- A surgery or other procedure scheduled in the next 180 days

There is also a special enrollment period available if you have to pay the California penalty for not having health coverage the prior year.15

In 2022, California enacted SB967, which created an easy enrollment program in California.16

Unlike most other states that have created or considered similar programs, the California legislation did not specifically create a special enrollment period for people deemed eligible for marketplace coverage (as opposed to Medicaid/CHIP, which is available year-round). However, Covered California does offer a special enrollment period specifically for people who have to pay a penalty on their state tax return for not having health insurance. A full list of Covered California’s special enrollment opportunities is available here.

Enrollment in Medi-Cal (California Medicaid) is available year-round.

Frequently asked questions about health insurance in California

How do I enroll in a Covered California Marketplace plan?

To enroll in an ACA Marketplace/exchange plan in California, you can:

- Visit Covered California, California’s health insurance exchange (Marketplace). Using this online platform, you can compare plans, determine whether you’re eligible for financial assistance, and enroll in coverage. You can reach the Covered California call center at 1-800-300-1506, Monday to Friday between 8 a.m. and 6 p.m.

- Enroll in a plan through Covered California with the help of an insurance agent or certified enrollment counselor.19

- Covered California has a “help on demand” program that allows you to submit your contact information and then receive a call from a certified enrollment assister who will help you sort out the details.

How can I find affordable health insurance in California?

The Affordable Care Act (ACA) provides income-based premium subsidies that can reduce the amount you pay for your coverage each month. In California, these subsidies are available to applicants who meet the eligibility requirements and enroll in a health plan through Covered California.

For 2026 coverage, California is offering additional state-funded premium subsidies to applicants with household income up to 165% of the poverty level20 ($25,823 for a single person or $53,048 for a family of four).

California is one of ten states where state-funded subsidies are available in addition to federal subsidies.

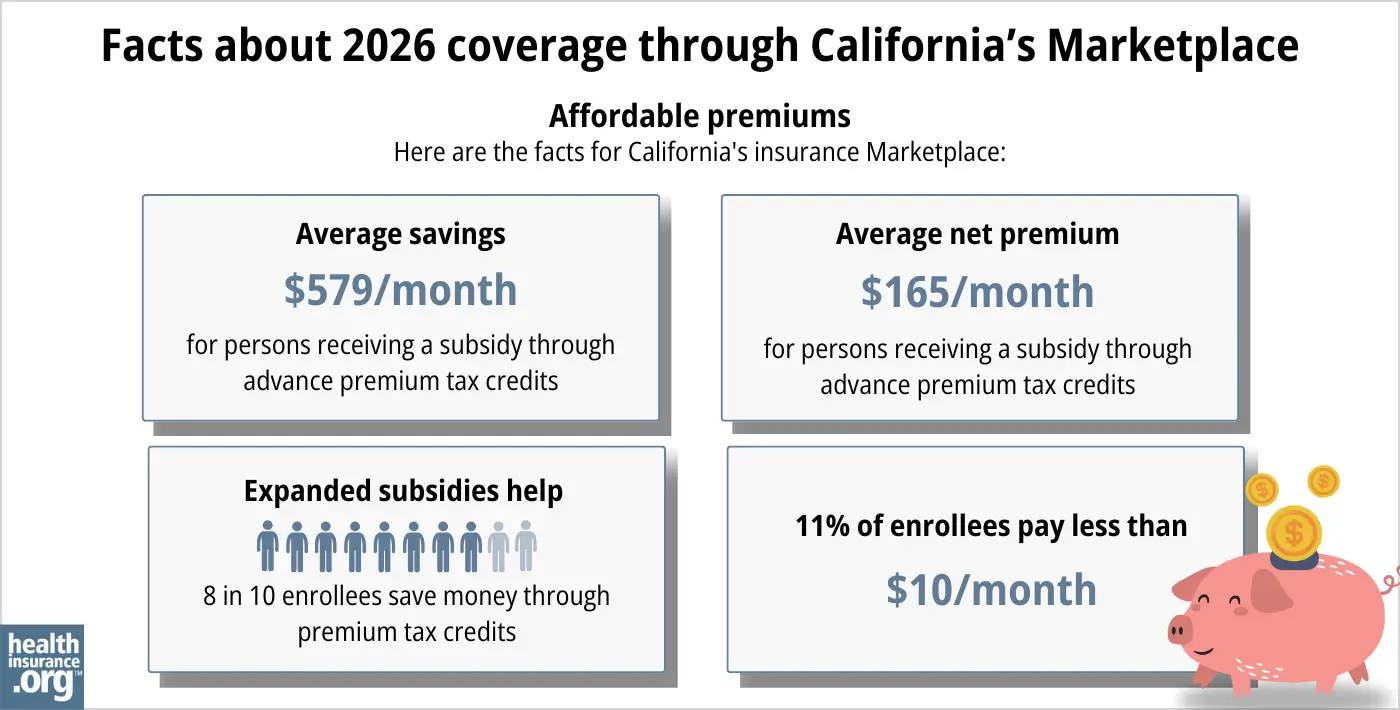

During the open enrollment period for 2026 coverage, eight out of ten people who enrolled via Covered California were eligible for premium tax credits. These subsidies averaged about $579/month, and after the subsidies were applied, the average subsidy-eligible enrollee’s premium was about $165/month.21

If your household income isn’t more than 250% of the federal poverty level, you’ll also be eligible for federal cost-sharing reductions (CSR). These benefits, which are built into Silver-level plans for eligible applicants, reduce the deductible and other out-of-pocket expenses. About 43% percent of Covered California enrollees were receiving CSR benefits as of 2026.22

In 2024 and 2025, California supplemented the federal CSR benefits with additional state-funded cost-sharing subsidies (for 2026, this program has been converted to a supplemental premium subsidy, to help offset some of the reduction in federal premium subsidies due to the expiration of federal subsidy enhancements). Eligible Silver-plan enrollees in 2024 and 2025 had $0 deductibles and lower costs for other out-of-pocket expenses.23

California allocated additional funding to the state subsidy program for 2025. So all Covered California enrollees qualified for at least the Enhanced Silver 73 plan,24 which offered reduced out-of-pocket costs and no deductibles.4

For 2026, California switched to a state-funded premium subsidy program. This was to offset some of the reduction in federal premium subsidies stemming from the expiration of federal subsidy enhancements.25

When the federal subsidy enhancements expired at the end of 2025, California’s state subsidy program switched to a supplemental premium subsidy for applicants with household income up to 165% of the federal poverty level. This helps to keep coverage affordable for those enrollees, but Covered California noted that the state funding is only a small fraction of the federal funding that was lost when the federal subsidy enhancements expired.26

Covered California and Medi-Cal (California Medicaid) use the same application, and the system will let you know whether you’re eligible for Medi-Cal or a private plan through Covered California – with subsidies if you qualify for them.

Source: CMS.gov 22

California does not allow short-term health insurance policies to be sold, under the terms of legislation that the state enacted in 2018.27

How many insurers offer coverage in California’s Marketplace?

Eleven insurers are offering individual/family plans through Covered California for 2026.26

- Anthem Blue Cross

- Blue Shield of California

- Balance by CCHP

- Health Net

- Inland Empire Health Plan

- Kaiser Permanente

- LA Care Health Plan

- Molina Healthcare

- Sharp Health Plan

- Valley Health Plan

- Western Health Advantage

This is down from 12 in 2025,4 as Aetna exited the market at the end of 2025 (as was the case in all states where Aetna offered Marketplace coverage).

Are Marketplace health insurance premiums increasing in California?

The following average rate changes were approved for 2026 for Covered California’s individual market insurers, amounting to an overall average rate increase of 10.1%, before subsidies were applied.28

California’s ACA Marketplace Plan 2026 APPROVED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Aetna CVS Health | Exited market |

| Anthem Blue Cross | 14.7% |

| Blue Shield of California | 9.3% |

| Balance by CCHP | 9.5% |

| Health Net | 14.8% |

| Inland Empire Health Plan | 17.9% |

| Kaiser Permanente | 7% |

| LA Care Health Plan | 10.9% |

| Molina Healthcare | 14.6% |

| Sharp Health Plan | 8.8% |

| Valley Health Plan | 20.3% |

| Western Health Advantage | 14.1% |

Source: California Department of Managed Healthcare29

California’s 2026 weighted average rate increase for full-price plans was less than half the national average,30 but it was still a double-digit increase. And for people who receive subsidies through Covered California (which was about nine out of ten enrollees in 2025),31 average net premiums (if everyone kept the same policy) increased by 97% for 2026, due to the failure of Congress to extend federal subsidy enhancements.25

The subsidy amount is different for each enrollee and changes each year depending on the cost of the second-lowest-cost Silver plan relative to the enrollee’s household income. Under the American Rescue Plan and the Inflation Reduction Act, subsidies were larger and more widely available than they used to be. But those subsidy enhancements expired at the end of 2025.

As a result, subsidies do not cover as much of the cost of 2026 coverage, and some people lost their subsidies altogether. Ultimately, some people dropped their coverage and others downgraded to Bronze plans. Even with those changes, the average after-subsidy premium in 2026 (including people who pay full-price) is $264/month, up from $187/month in 2025.32

If the cost of your current plan is increasing for the coming year, you may want to consider some of the other plans that are available via Covered California. You might find some that are less expensive and offer similar benefits.

Here’s a look at how average full-price (pre-subsidy) premiums have changed over the years in California’s individual/family market:

How many people are insured through California’s Marketplace?

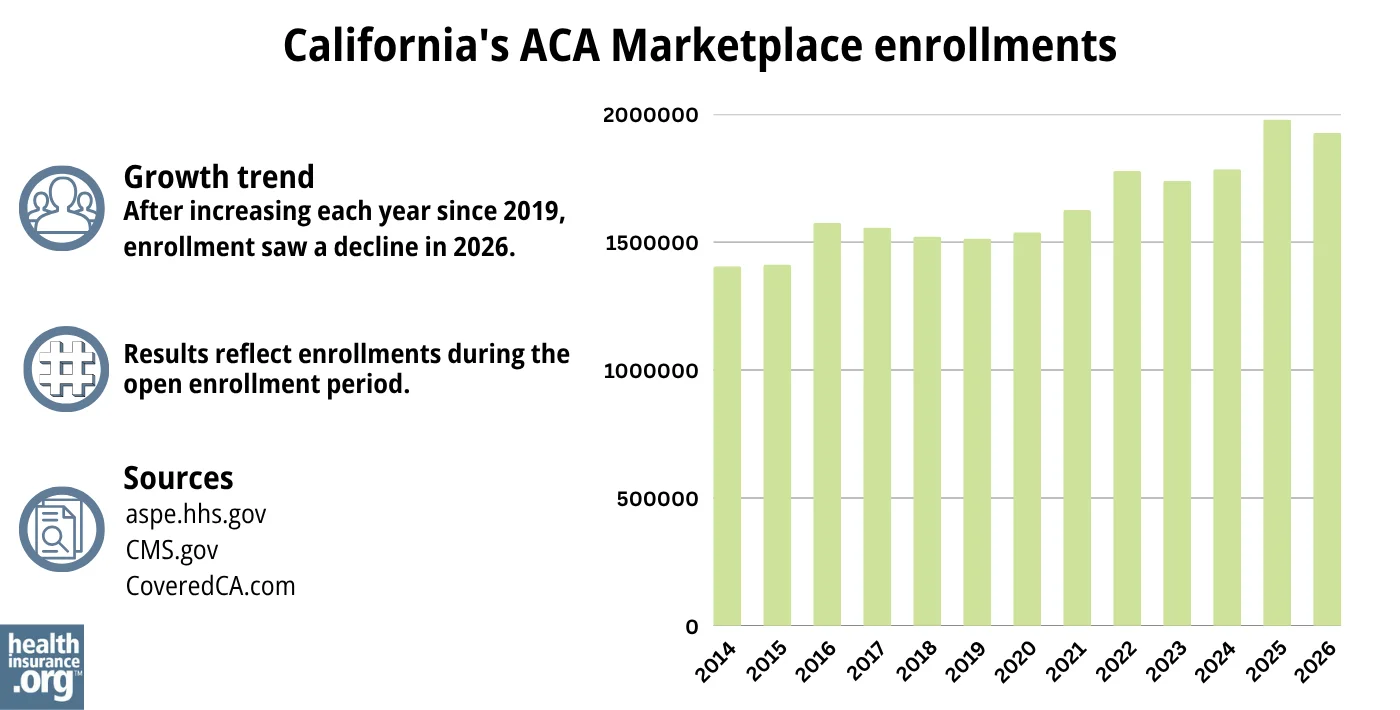

CMS reported that 1,927,371 people enrolled in 2026 plans through Covered California during open enrollment.21

This was down about 52,000 from the year before, when Covered California’s enrollment had reached a record high. The decline in 2026 was due to the expiration of the federal subsidy enhancements at the end of 2025, which drove net premiums higher.

Here’s a summary of historical enrollment numbers for Covered California:

Source: 2014,44 2015,45 2016,46 2017,47 2018,48 2019,49 2020,50 2021,51 2022,52 2023,53 2024,54 202555 202622

What health insurance resources are available to California residents?

Covered California: This is California’s Marketplace/exchange. Residents can use Covered California to enroll in individual/family health plans and receive income-based subsidies, and also to enroll in Medi-Cal. You can contact Covered California at 800-300-1506.

California Department of Health Care Services: The agency that administers Medi-Cal and various other health care programs.

California Department of Managed Health Care (DMHC): Regulates the vast majority of California’s commercial (non-self-insured) health plans, and assists consumers and businesses with insurance-related questions and concerns.

California Department of Insurance: Regulates California’s insurance plans that aren’t regulated by the DMHC. If a complaint or concern is filed with the DMHC and it’s for a product that’s regulated by the Department of Insurance, it will be forwarded to the Department of Insurance.

California Health Insurance Counseling and Advocacy Program (HICAP): A service for California Medicare beneficiaries and their caregivers. HICAP provides information and assistance with questions related to Medicare eligibility, enrollment, and claims.

Looking for more information about other options in your state?

Need help navigating health insurance options in California?

Explore more resources for options in CA including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Penalty” CoveredCA.com, Accessed Dec. 9, 2025 ⤶

- ”Information About Qualified Health and Dental Plan Issuers” Covered California. Accessed Aug. 26, 2025 ⤶

- ”Covered California 2026 CCSB Health Plan Offerings” Covered California. Accessed Jan. 22, 2025 ⤶

- ”Covered California’s Rates and Plans for 2025: The Most Financial Support Ever to Help More Californians Pay for Health Insurance” Covered California. July 24, 2024 ⤶ ⤶ ⤶

- “Covered California 2026 Patient-Centered Benefit Plan Designs” CoveredCA.com, Jul. 28, 2025 ⤶

- “Standardized Plans in the Health Care Marketplace: Changing Requirements” KFF.org, May 8, 2023 ⤶

- “Who can get a health plan through Covered California?” CoveredCA.com, Accessed Dec. 9, 2025 ⤶

- ”Medi-Cal Immigrant Eligibility FAQs” California DHCS. Accessed Apr. 23, 2026 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Dec. 9, 2025 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Dec. 9, 2025 ⤶ ⤶

- California Assembly Bill 570. BillTrack50. Enacted October 2021. ⤶

- California Now 1st State To Let Parents Be Added To Their Children’s Insurance Plans. CBS News Sacramento. October 2021. ⤶

- “Dates and Deadlines” CoveredCA.com Accessed Apr. 23, 2026 ⤶

- “Federal Changes to Your Health Insurance” Covered California. Accessed Apr. 15, 2026 ⤶

- Qualifying Life Events. Covered California. Accessed Dec. 9, 2025 ⤶ ⤶

- California Senate Bill 967. BillTrack50. Enacted August 2022. ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Covered California Rates and Plans for 2026: Consumer Affordability on the Line with Uncertainty Surrounding Federal Premium Tax Credit Extension” Covered California. Aug. 14, 2025 *The above is based on the most current data available. ⤶

- “Help With Your Application” CoveredCA.com, Accessed Dec. 9, 2025 ⤶

- ”Program Eligibility by Federal Poverty Level for 2026” Covered California. Accessed Dec. 9, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. Accessed March 2026 ⤶ ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. Accessed March 2026 ⤶ ⤶ ⤶

- “Covered California to Launch State-Enhanced Cost-Sharing Reduction Program in 2024 to Improve Health Care Affordability for Enrollees” CoveredCA.com, July 20, 2023 ⤶

- ”Covered California Policy and Action Items” Covered California Board Meeting.May 16, 2024 ⤶

- ”Covered California’s Open Enrollment 2026: Here to Help Connect Californians to Care Despite Uncertainty Around Federal Tax Credits” Covered California. Oct. 30, 2025 ⤶ ⤶

- ”Covered California Rates and Plans for 2026: Consumer Affordability on the Line with Uncertainty Surrounding Federal Premium Tax Credit Extension” Covered California. Aug. 14, 2025 ⤶ ⤶

- California Senate Bill 910. BillTrack50. Enacted September 2018. ⤶

- ”2026 Final Gross Rate Changes – California: +10.1% (updated)” ACA Signups. Oct. 5, 2025 ⤶

- ”Search Rate Review Filings” California Department of Managed Healthcare. Accessed Dec. 9, 2025 ⤶

- ”2026 Rate Change Project” ACA Signups. Nov. 2, 2025 ⤶

- “Effectuated Enrollment: Early 2025 Snapshot and Full Year 2024 Average” CMS.gov. July 24, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” And ”2025 Marketplace Open Enrollment Period Public Use Files”CMS.gov. Accessed Apr. 23, 2026 ⤶

- Covered California Announces Rates for 2015; Rigorous Negotiations with Health Insurance Companies Keep Rate Increases Low and Choices Robust. Covered California. July 2014. ⤶

- Covered California Holds Rate Increases Down For Second Consecutive Year. Covered California. July 2015. ⤶

- Covered California Health Plan Rates To Jump 13.2 Percent In 2017. KFF Health News. July 2016. ⤶

- 2018 Rate Hikes. ACA Signups. October 2017. ⤶

- Covered California Releases 2019 Individual Market Rates: Average Rate Change Will Be 8.7 Percent, With Federal Policies Raising Costs. Covered California. July 2018. ⤶

- 2020 Rate Changes. ACA Signups. October 2019. ⤶

- California’s Efforts to Build on the Affordable Care Act Lead to a Record-Low Rate Change for the Second Consecutive Year. Covered California. August 2020. ⤶

- Covered California Announces 2022 Plans: Full Year of American Rescue Plan Benefits, More Consumer Choice and Low Rate Change. Covered California. July 2021. ⤶

- UPDATED: FINAL Unsubsidized 2023 Premiums: +6.2% Across All 50 States +DC. ACA Signups. Accessed November 2023. ⤶

- Covered California’s Health Plans and Rates for 2024: More Affordability Support and Consumer Choices Will Shield Many From Rate Increase. CoveredCA.com, July 25, 2023 ⤶

- ”California: *Final* avg. unsubsidized 2025 ACA rate changes: +7.7% individual market, +7.3% small group market” ACA Signups. Oct. 10, 2024 ⤶

- “Health Insurance Marketplace: Summary Enrollment Report for the Initial Annual Open Enrollment Period” HHS; ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report ”, HHS; ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2016 Open Enrollment Period: Final Enrollment Report” HHS; ASPE, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files ” CMS.gov, 2017 ⤶

- “ 2018 Marketplace Open Enrollment Period Public Use Files ” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files ” CMS.gov, 2019 ⤶

- “ 2020 Marketplace Open Enrollment Period Public Use Files ” CMS.gov, 2020 ⤶

- “ 2021 Marketplace Open Enrollment Period Public Use Files ” CMS.gov, 2021 ⤶

- “ 2022 Marketplace Open Enrollment Period Public Use Files ” CMS.gov, 2022 ⤶

- “ Health Insurance Marketplaces 2023 Open Enrollment Report ” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- ”Covered California Reaches Landmark Achievement with Nearly 2 Million Enrolled as Open Enrollment Concludes” CoveredCA.com, February 20, 2025 ⤶