Medicare in Georgia

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Georgia

Key takeaways

- Over 1.9 million residents are enrolled in Medicare in Georgia.1

- About 55% of Georgia Medicare beneficiaries are enrolled in Medicare Advantage plans.1

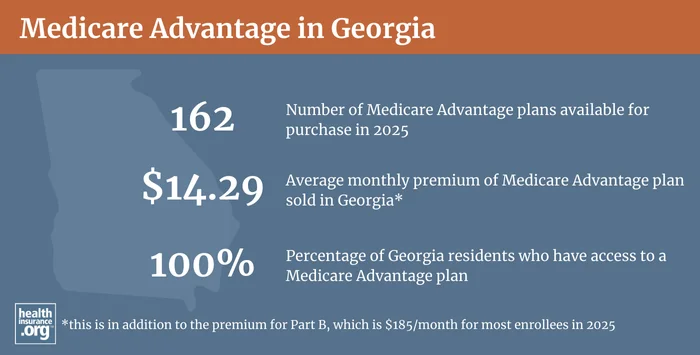

- All counties in Georgia have Medicare Advantage plans available, but plan options vary considerably from one county to another.2

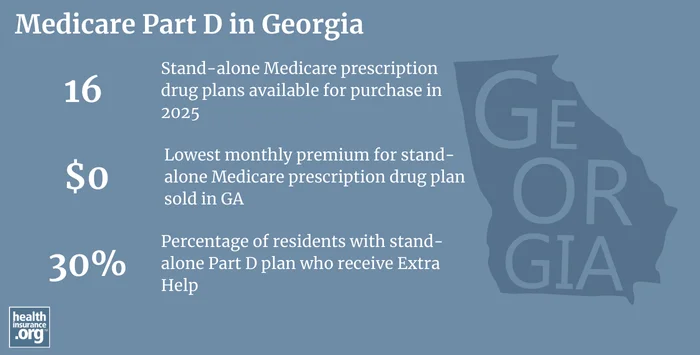

- There are 16 stand-alone Part D prescription plans available in Georgia in 2025.3

Medicare enrollment in Georgia

As of August 2024, there were 1,939,560 people enrolled in Medicare in Georgia.4 That’s about 15% of the state’s population versus about 17% of the total U.S. population enrolled in Medicare.5

For most Americans, enrolling in Medicare benefits goes along with turning 65 years old. But over 7 million Americans under the age of 65 also have Medicare coverage.6 This is because Medicare eligibility is also triggered once a person has been receiving disability benefits for 24 months, or has kidney failure or ALS.

Nationwide, almost 11% of Medicare beneficiaries are under age 65:6 for beneficiaries of Medicare in Georgia, it’s 12%.4

The Medicare Annual Election Period runs from October 15 to December 7 each year and allows Medicare beneficiaries the chance to switch between Medicare Advantage and Original Medicare (and add, drop, or switch to a different Medicare Part D prescription drug plan). People who are already enrolled in Medicare Advantage plans also have the option to switch to a different Medicare Advantage plan or to Original Medicare during the Medicare Advantage open enrollment period, which runs from January 1 to March 31.

Learn about Medicare plan options in Georgia by contacting a licensed agent.

Explore our other comprehensive guides to coverage in Georgia

The ACA Marketplace allows individuals and families to shop for and enroll in ACA-compliant health insurance plans. Subsidies may be available based on household income to help lower costs.

Hoping to improve your smile? Dental insurance may be a smart addition to your health coverage. Our guide explores dental coverage options in Georgia.

Learn about Georgia’s Medicaid expansion, the state’s Medicaid enrollment and Medicaid eligibility.

Short-term health plans provide temporary health insurance for consumers who may find themselves without comprehensive coverage. Learn more about short-term plan availability in Georgia.

Frequently asked questions about Medicare in Georgia

What is Medicare Advantage?

Medicare beneficiaries can choose to get their Part A and Part B coverage through private Medicare Advantage plans, or directly from the federal government via Original Medicare.

Medicare Advantage plans are offered by private insurers and plan availability varies from one county to another. For example, in some Georgia counties, there are only 20 Medicare Advantage plans available in 2024, whereas in other counties there are more than 50 plans.2

Medicare Advantage enrollment had increased to 55% of the state’s Medicare population by July 2024, where about 1,069,003 Georgia Medicare beneficiaries had Medicare Advantage coverage1 (not counting people with private coverage like Part D and Medigap, used to supplement Original Medicare).

About 865,913 Georgia Medicare beneficiaries had coverage under Original Medicare instead at that point.1

What are Medigap plans?

Original Medicare does not limit out-of-pocket costs (like monthly premiums and coinsurance or copayments), so most enrollees maintain some form of supplemental coverage.7

Nationwide, over 80% of Original Medicare beneficiaries have supplemental coverage. But for those who don’t, Medigap plans (also known as Medicare Supplement Insurance plans, or MedSupp) will pay some or all of the out-of-pocket costs (e.g., deductibles and coinsurance) they would otherwise have to pay if they only had Original Medicare coverage.8

Medigap plans are sold by private insurers, but they’re standardized under federal rules and regulated by state laws and insurance commissioners. There are 39 insurers that offer individual Medigap plans in Georgia in 2025.9 Details about the insurers that offer Medigap plans in Georgia are available through the Plan Finder tool on the Medicare.gov website.

There are three ways Medigap insurers can set their premiums: Issue-age rating means that premiums are based on the age the person was when they enrolled in the plan, so a person who enrolls at age 65 will always pay a lower premium than a person who enrolls at age 80 (rates can still increase overall, but not based on a particular enrollee’s increasing age). Attained-age rating is the approach that most insurers use nationwide (except where prohibited), and it allows the insurer to increase premiums based on the enrollee’s current age, so rates go up as a person ages. Community rating means that premiums don’t vary with age, but there are only eight states that require this approach, and insurers usually do not use it if not required to do so.10

In Georgia, Medigap insurers have been prohibited from using attained-age rating for plans issued since 2009 (see Section 7). So most Medigap plans in the state use issue-age rating, 11although some opt for community rating.

Federal rules require Medigap insurers to offer plans on a guaranteed-issue basis during an enrollee’s open enrollment period, which begins when the person is at least 65 years old and enrolled in Medicare Part B (and Part A; you have to be enrolled in both to obtain Medigap, but some people delay enrollment in Part B if they continue to receive employer-sponsored coverage to supplement Medicare Part A). Despite the fact that over 7 million Medicare beneficiaries nationwide are not yet 65,12 there is no federal requirement that Medigap insurers offer plans to people who are under age 65.13 However, the state of Georgia does require insurers to offer Medigap to those under 65.11

But the majority of the states have addressed this with legislation that ensures at least some access to Medigap plans for people under age 65, and Georgia is among them. In Georgia, Medigap insurers must offer their plans on a guaranteed-issue basis to anyone who enrolls in Medicare Part B, regardless of age.11 This rule took effect in 2011, and Georgia granted a one-time six-month open enrollment period to people who already had Part B; since then, people who enroll in Medicare in Georgia all have the same six-month open enrollment period for Medigap, regardless of their age.

Georgia’s statute clarifies that people under age 65 can be charged higher premiums, but that the premium variation “shall not be excessive, inadequate, or unfairly discriminatory and shall be based on sound actuarial principles and reasonable in relation to the benefits provided.”11 Even with that parameter, Medigap rates are substantially higher for Georgia residents under the age of 65; rate filings are available in SERF and on Medicare’s plan finder tool. Most Georgia Medigap insurers are charging under-65 enrollees between three and ten times as much as they charge enrollees who are 65.14

Disabled Medicare beneficiaries have access to another Medigap open enrollment period when they turn 65. At that point, they can obtain a plan with the standard age-65 rates.

Disabled Medicare beneficiaries have the option to enroll in a Medicare Advantage plan instead of Original Medicare, and rates are not higher for enrollees under age 65. Medicare Advantage plans have more limited provider networks than Original Medicare, and total out-of-pocket costs can be as high as $8,300 per year for in-network care, plus the out-of-pocket cost of prescription drugs (Part D does not have a cap on out-of-pocket costs, regardless of whether it’s purchased as a stand-alone plan or integrated with Medicare Advantage) can be higher.15

Although the Affordable Care Act eliminated pre-existing condition exclusions in most of the private health insurance market, those rules don’t apply to Medigap plans. Medigap insurers can impose a pre-existing condition waiting period of up to six months if an individual didn’t have at least six months of continuous coverage prior to your enrollment (although many of them choose not to do so). And if you apply for a Medigap plan after your initial enrollment window closes (assuming you aren’t eligible for one of the limited guaranteed-issue rights), the Medigap insurer can consider your medical history in determining whether to accept your application, and at what premium.

What is Medicare Part D?

Original Medicare does not provide coverage for outpatient prescription drugs. Over 80% of Original Medicare beneficiaries have some type of supplemental coverage, and these plans can include prescription drug coverage.716

Medicare Part D, created under the Medicare Modernization Act of 2003, provides drug coverage for Medicare beneficiaries who do not have another source of coverage for prescription drugs expenses. Medicare Part D coverage can be purchased as a stand-alone plan (called a prescription drug plan, or PDP) or obtained as part of a Medicare Advantage plan. (Medicare Advantage plans with built-in prescription drug coverage are called Medicare Advantage-Prescription Drug, or MAPD, plans).

You can sign up for a PDP or MAPD (or change to a different one) during the annual enrollment period that runs from October 15 to December 7 each year, with the new coverage effective January 1 of the coming year.

There are 16 stand-alone Medicare Part D plans for sale in Georgia in 2025, with premiums that start at $0 per month.3

Overall Medicare Part D enrollment — including stand-alone prescription drug plans and Medicare Advantage plans with integrated Medicare Part D prescription drug coverage — has been steadily increasing in Georgia1718 as overall Medicare coverage enrollment has grown. But enrollment in stand-alone Medicare Part D plans has been decreasing in Georgia, because Medicare Advantage enrollment growth has outpaced Original Medicare enrollment growth.

As of July 2024, there were 524,870 Georgia residents with stand-alone Medicare Part D plans.1 That was down from more than 627,566 in March 2018.17 But during the same period, enrollment in Medicare Advantage plans with integrated Part D coverage had grown from about 620,828 people17 to more than 1,022,907 people.1

What additional resources are available for Medicare beneficiaries and their caregivers in Georgia?

Need help with your Medicare coverage enrollment, or understanding your Medicare eligibility in Georgia? You can contact the State Health Insurance Assistance Program with questions related to Medicare enrollment in Georgia.

Regardless of whether you’re about to submit your Medicare application in Georgia or have been a Medicare beneficiary for many years, you’re likely to have questions from time to time. The Medicare Rights Center website is a nationwide resource for information, with helpful content geared to Medicare beneficiaries, caregivers, and professionals.

Looking for more information about other options in your state?

Need help navigating health insurance options in Georgia?

Explore more resources for options in GA including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Georgia.” Centers for Medicare & Medicaid Services Data. Accessed November, 2024. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- ”Medicare Advantage 2024 Spotlight: First Look” KFF.org Nov. 15, 2023 ⤶ ⤶

- ”Fact Sheet: Medicare Open Enrollment for 2025” (32) Centers for Medicare & Medicaid Services. Sep. 27, 2024 ⤶ ⤶

- “Medicare Monthly Enrollment – Georgia.” Centers for Medicare & Medicaid Services Data. Accessed December, 2024. ⤶ ⤶

- “U.S. Census Bureau Quick Facts: Georgia; United States.” U.S. Census Bureau, July, 2023. ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data, November 2024. ⤶ ⤶

- Ochieng, Nancy, and Jeannie Fuglesten Biniek. “Cost-Related Problems Are Less Common among Beneficiaries in Traditional Medicare than in Medicare Advantage, Mainly Due to Supplemental Coverage.” Kaiser Family Foundation, July 7, 2021. ⤶ ⤶

- “Get Medigap Basics.” Medicare.gov. Accessed July 22, 2023. ⤶

- “Explore your Medicare coverage options.” Medicare.gov. Accessed October, 2024. ⤶

- “Community Rating – Glossary.” Glossary | HealthCare.gov. Accessed July 27, 2023. ⤶

- “Subject 120-2-8 Medicare Supplement Insurance.” State of Georgia. Accessed July 27, 2023. ⤶ ⤶ ⤶ ⤶

- ”Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data, November 2024. ⤶

- “Get Ready to Buy.” Medicare.gov. Accessed July 21, 2023. ⤶

- “Supplement Insurance (Medigap) Plans in Georgia.” Medicare.gov. Accessed July 23, 2023. ⤶

- “What You’ll Pay in Out-of-Pocket Medicare Costs in 2023.” The National Council on Aging, November 18, 2022. ⤶

- “HP-2022-08 Medicare Beneficiary Enrollment Trends.” Office of Health Policy, March 2, 2022. ⤶

- “Medicare Monthly Enrollment – Georgia (2018).” Centers for Medicare & Medicaid Services Data, March 2018. ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – Georgia.” Centers for Medicare & Medicaid Services Data, March 2023 ⤶